The market once again gained momentum and hit a fresh all-time high this week ahead of Diwali 2020.

Consistent liquidity flow, hope of strong earnings and economic growth in FY22, better-than-expected September quarter earnings and progress in the COVID-19 vaccine are the key drivers of the rally.

Experts say the momentum may continue in Samvat 2077 as well given the expected growth across segments.

"Nifty had traded sideways since January 2018. Barring the sharp dip made by Nifty briefly this year, for the last three years, it has traded in the range of 10,000-12,000. A three year sideways consolidation has made a right base from where a sharp up move will happen once earnings and economy start showing positive trends. And coming calendar year looks set to provide the right impetus for this breakout to happen," Shailendra Kumar, Chief Investment Officer at Narnolia Financial Advisors told Moneycontrol.

Larger part of the economic pain and lacklustre corporate earnings are behind us. We should expect firm price trends ahead with a higher high and higher low kind of price behaviour, he said.

At the same time, we should always avoid investing in bad quality businesses because as is said a rising tide lifts all the boats but the end outcome is always bad in investing if one ignores the quality aspect, he advised.

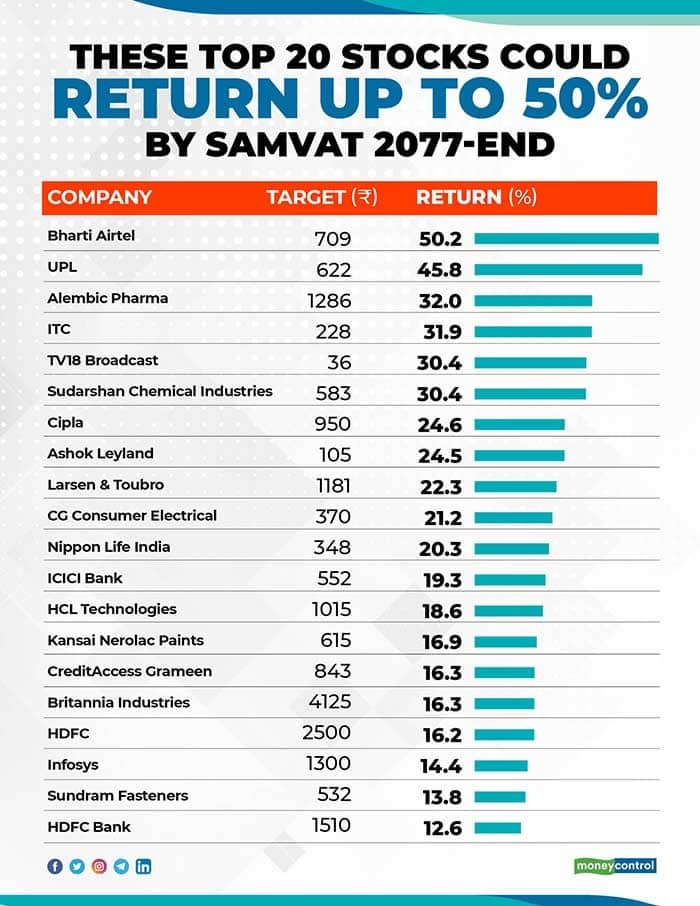

Here is a list of 20 stocks that could return 13-50 percent by Samvat 2077-end:

Brokerage: Religare Broking

The domestic commercial vehicle (CV) industry is poised for healthy growth led by increased government spending on infrastructure, mining and pick-up in economic activity. We believe ALL stands to benefit from the upcycle in the CV industry given its strong position in the M&HCV and LCV segment. Further, the proposed implementation of CV scrappage policy is likely to create an additional demand of around 1 lakh vehicles. To reduce the earnings volatility, the company has sharpened its focus on increasing its revenue share from LCVs, spares, exports and defence. We believe that ALL’s strong brand presence in the CV segment and its focus on diversifying to less cyclical businesses makes it one of our preferred picks in the sector.

Bharti Airtel is well placed to benefit from increased traction received in digital services which we believe is likely to continue going forward. After a steady addition of customers, Bharti can continue to gain market share in the mobile services business. The uncertainty over AGR dues is also behind us as Supreme Court has allowed 10 years payment window for telecom operators. In our view, the tariff hike would continue from here on, to reduce the financial stress on telecom companies which would benefit Bharti Airtel due to its strong customer base and a healthy addition of 4G customers. Further, strong cash flow generation would also help in deleveraging the balance sheet.

We expect CGCE to continue to strengthen its market share in the ECD segment both from unorganized as well as other players. Its strong product portfolio, new innovative product launches, strong brand presence would enable the company to achieve a higher market share in the ECD segment. Further, strong focus on cost optimization measures, increased revenue from the premium portfolio, and signs of margins bottoming out in the lighting segment augur well for margin improvement. Hence, CGCE’s strong product portfolio, market leadership in key segments coupled with healthy dividend payout ratio (33-36 percent), lean working capital cycle, strong cash flow generation and robust return ratios make it one of our preferred picks in the sector.

The COVID-19 pandemic has impacted the banking sector as a whole however measures lend by RBI and government help it to pass through this difficult time. At present in Q2FY21, we witnessed many banking players (both private and public banks) posted better numbers on the back of improving asset quality, better collections and lower provision. In the coming quarters, with improving demand and the economy getting back on track, the banking sector would see good growth recovery. We would prefer investing in large private banking space with ICICI bank as our preferred pick. The bank has a strong brand name, healthy capital and liquidity position, stable asset quality, a large customer base and improved corporate governance under new management.

Kansai Nerolac Paints

Indian paint sector is expected to grow in double-digit driven by government initiatives for housing, rising disposable income, increase in rural spending, and reduction in repainting cycle and pickup in auto demand. Further with a reduction in GST to 18 percent from 28 percent has helped organised players to gain market share. In the near term, due to COVID as well as the slowdown in Auto, KNPL performance is expected to be muted in FY21. Nonetheless, going forward, the company has plans to grow in both decorative as well as industrial space and gain market share driven by innovative products, focus on non-auto segments, increase distribution network and expand in newer areas that are technology-intensive.

L&T intends to use a major portion of the net cash inflows (around Rs 11,000 crore) from the sale of its electrical and automation business to service part of its debt and to grow technology and financial services businesses. Further, improvement in cash collections as the economy rebounds and monetization of non-core assets is likely to strengthen its cash reserves in the coming years. L&T’s strong execution capabilities enable the engineering conglomerate to command a premium over its peers. Thus, L&T by virtue of its market leadership is likely to be the key beneficiaries of the infrastructure spend by the government. We believe L&T’s diversified business portfolio and sound balance sheet make it one of the best long-term bets in the infrastructure space.

We continue to remain constructive on the Indian mutual fund industry given its low penetration level as compared to major economies (11 percent AUM to GDP ratio versus world average of 62 percent), increase in the financialization of savings and continuous strengthening of SIP flows. Further, NAM’s consistent increase in equity assets, industry-leading retail assets and strong presence in B-30 cities augur well for the growth prospects of the company. The consistent increase in monthly SIP book (Rs 620 crore) would ensure longevity and regular inflows providing stable growth.

SCI is well place to capitalize on opportunities in the global as well as Indian pigment sector driven by positive industry growth trend, a wide range of products, cost competitiveness and strong technical capabilities. In H1FY21 the growth was impacted due to the Covid-19 pandemic, however the demand has started picking up but the pace is gradual and would normalize by FY21. Further from a long-term perspective, we remain positive on the company’s growth given its strong products, focus on pigments segment, expansion opportunity and strong financial track record. Besides, it would see improvement in margins driven by a change in product mix (focus towards high margin products) and stable raw material prices.

Brokerage: KR Choksey

The pandemic has led to structural change in perceptions for home. The cost on the liabilities have come off aided by lower interest rates, TLRTRO and higher debt flows to well-rated companies. HDFC has been a key beneficiary with one of lowest lending costs in the industry. This places it favourably amidst competition. We expect it to be able to maintain NIMs at above 3 percent even as incremental individual loans may be higher. We expect strong operating performance on the back of managed costs and strong NIIs.

With the traction in advances, lower incremental credit costs, strong operating profits, improved risk adjusted NIMs, we expect NII growth of 16 percent/20 percent; PPoP at around 18 percent; PAT at 23 percent/20 percent and ability to maintain RoAs at 1.9 percent in FY21/22 respectively. We raise our target to Rs 1,510 (from Rs 1,427), implying a P/ABV of 3.7x FY22E P/ABV (higher from 3.5x on improving growth momentum and low adverse risk to credit costs).

Britannia is as a buy with target price of Rs 4,125, after applying P/E multiple of 50.0x to the FY22 EPS of Rs 82.5 per share. The company commands a well-deserved valuation premium on account of strong brand image, consistent improvement in margins and the essential nature of its products like biscuits.

We have a buy recommendation on UPL, with a target price of Rs 622 per share. The company’s pipeline is valued currently at $2.0 billion to $2.5 billion of peak sales, reaching maturity in the next five to eight years. Moreover, the company has highlighted that they expect $5.0 billion of additional market value from products becoming off-patent in the next five years, and the company’s backward integration and scale will facilitate it to grab a large share of this market.

We expect Alembic Pharma's topline to grow at a CAGR of 16.8 percent over FY20-22E period and net profit to grow by CAGR of 13.9 percent over FY20-22E period. We are optimistic of company’s growth prospects on the back of new product introductions in the US, new products filed from recently commercialized Aleor JV, and improvement in the revenue mix with contribution from general and oncology injectables. Growth in the US market to remain intact with 15-20 expected new launches a year for next three years. Company to see continued traction in the Azithromycin for at least two more quarters, which will drive the API business. Recovery in the RoW & domestic market will also continue.

We believe the IT major is well-positioned to ride the increase in IT spend led by cloud movement, with its wide portfolio of offerings and large deal aggression, with margins likely to be resilient, and cash return to shareholders in the form of buy backs and dividends, a recurring theme.

We have a buy recommendation on HCL Technologies, with a target of Rs 1,015. We believe the IT major’s wellestablished position in cloud infrastructure services, integrated service portfolio in traditional IT services, digital and ER&D services, and P&P differentiator will drive double-digit revenue and earnings growth from FY21-FY23E. Cash return through consistent dividend payouts, and M&A activity should also ensure better cash usage.

We expect, Ad-revenue to increase led by the festive season later in the quarter and few big ticket events and programmes but the growth on the same will be moderate. Subscription revenue continues to drive growth over ad-revenue on account of new tariff order implementation which normalized and gaining good amount of traction. Stock currently trades at EV/EBITDA of 9.5x on FY22 EBITDA of INR 7430 Mn and EV/EBITDA of 10x on trailing EBITDA. We have valued it at EV/EBITDA multiple of 11x on FY22 EBITDA to arrive at a target price of 36 per share.

It has a strong parentage of CreditAccess India N.V. as a promoter Rs 800 crore worth of funds raised through QIP issue (allotment at Rs 707 per share) on October 8, 2020 which reduced promoter holding up to 74 percent. Additionally, allotment of NCDs worth Rs 100 crore to strengthened its liquidity. It is a good quality stock with strong asset quality (NNPA of 0 percent), healthy capital & high promoter holding. Accordingly, we assign P/ABV multiple of around 3.26x to FY22E consolidated adjusted book value of Rs 258.2 per share to arrive at a target price of Rs 843 per share and maintain buy rating on the stock.

ITC with diversified operations across non-cyclical sectors, a resilient business model, strong brand leadership position in cigarette business, product innovation track record & premiumization drive is establishing itself as a FMCG major. Despite the ongoing COVID-19 related slowdown, we see recovery signs in recent months and the current valuation attractive. Besides, we expect the cigarette business to revive in the future with strict regulation from government on curbing the sale of illegal cigarettes.

Cipla is de-facto leader in respiratory therapies in India with a market share of 25.7 percent (rank 1). In inhalation category, Cipla’s market share stands at 68.9 percent (rank 1). It also has a significant market share in therapies like Urology with a market share of 16.3 percent (rank 1) and Cardiology with a share of 5.5 percent (rank 4). Cipla’s comprehensive COVID-19 portfolio consists of Cipremi (Remdesivir), Actemra (Tocilizumab), and Ciplenza (Favipiravir) which helped company in posting strong growth in Q2FY21 in the domestic market.

After a steller H1FY21 performance, we have revised estimates for Cipla upwards for FY21E/FY22E. Key factors to watch out for Cipla in near term are approval of Advair Diskus, ramp-up in albuterol and contribution of COVID-19 drugs. Company has 250 ANDAs as of 30th Sep, 2020, with 66 ANDAs pending for USFDA approval.

We maintain our positive stance, on back of diversified set of product portfolio, and strong domestic presence in all segments of automobile. We expect EBITDA margin to remain at around 16 percent for FY21 and further to improve in FY22E to around 18 percent, led by favourable commodity price, better revenue mix (higher contribution value added products and specialized fasteners) and gradually increased in its factories operation to three shifts to meet the improved demand. Further, SFL is having sufficient capacity available to capitalize on the demand front in the domestic and export markets, return ratio are expected to improve in FY22 on better operating performance and lower capex spend.

Disclaimer: The views and investment tips expressed by investment expert on Moneycontrol.com are his own and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

TV18 Broadcast is owned by Network 18 Media & Investments which publishes Moneycontrol.com.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.