Ruchi Agrawal

Moneycontrol Research

Oil marketing companies (OMCs) reported a mixed set of Q4 numbers last fiscal. While Bharat Petroleum Corporation (BPCL) managed a healthy showing, Indian Oil Corporation (IOC) and Hindustan Petroleum Corporation (HPCL) saw some sequential impact due to subdued performance in the refining segment. Performance of the marketing segment was strong with an uptick in margins after the December17 Gujarat assembly elections.

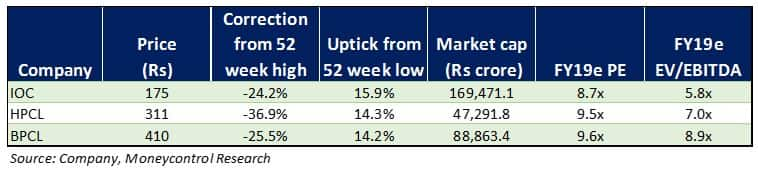

Although there has been substantial correction in stock prices, we approach the current year with caution given the upcoming state elections and past trends of tweaking margins around election time, rising crude oil prices and the government’s unwillingness to reduce excise duty or value added tax.

Indian Oil Corporation

The company reported a 157 percent year-on-year (YoY) uptick in earnings before interest, tax, depreciation and amortisation (EBITDA) in Q4 FY18 on the back of resilient performance in the marketing segment. However, EBITDA declined 17 percent sequentially due to lower gross refining margins (GRMs) at $9.1 per billion barrels (bbl) and lower refining inventory gains.

Net profit declined 34 percent quarter-on-quarter (QoQ) due to lower other income and higher finance costs.

Strong performance in the marketing segment was driven by improved margins and 7 percent YoY growth in volumes as domestic sales and exports increased 6 percent and 21 percent YoY, respectively. Shut down at the Paradip unit led to 6 percent QoQ contraction in refining volumes. Shut down of the Panipat complex led to an 8 percent QoQ fall in petchem volumes. The management said Paradip refinery is expected to reach 30 percent high sulphur crude processing target by Q2 FY19, which would drive GRMs. The latter was impacted by shutdowns and impacted its overall performance.

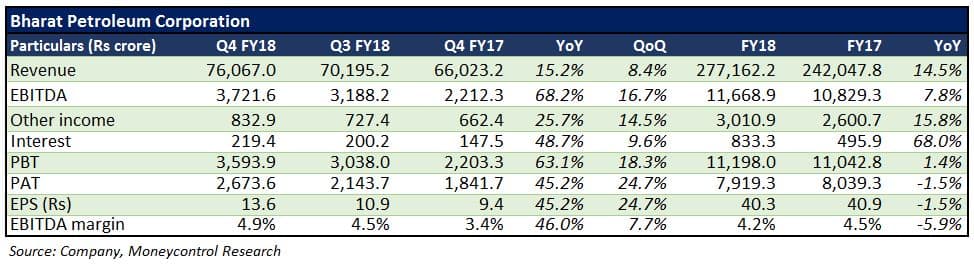

Bharat Petroleum Corporation

The company reported GRMs at $6.5/bbl, up 8 percent YoY but down 18 percent sequentially. EBITDA improved 68 percent YoY on the back of inventory gains and lower employee costs. Despite higher finance costs and other expenses PAT increased 40 percent YoY on rising other income.

Refining margins came in lower than peers after capacity expansion at the Kochi refinery. The same is likely to improve going forward. Marketing volume grew 9.9 percent YoY to 11.1 million tonne (MT), with domestic sales up 16 percent and exports down 58 percent. The company was able to gain back market share, This, coupled with improved margins, could drive growth.

With improved utilisation at the Kochi refinery, the management aims to work on improving the product and sourcing mix to enhance margins. To improve diesel volumes, BPCL is working on further enhancing its highway presence.

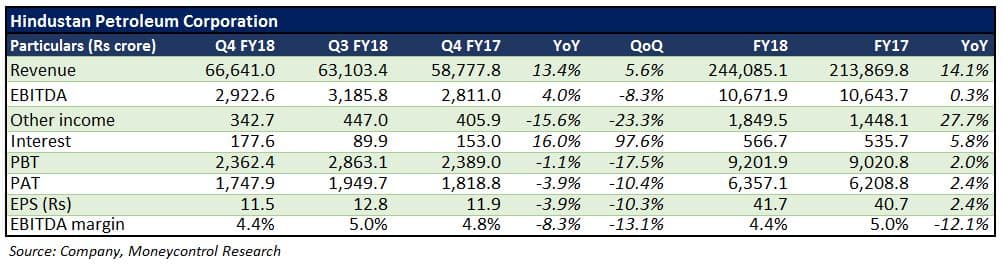

Hindustan Petroleum Corporation

Despite a healthy 13.4 percent YoY uptick in Q4 revenue, EBITDA grew 4 percent due to higher other expenses. Profit after tax declined around 4 percent YoY on the back of a 12 percent decline in GRMs at $7.1/bbl and weak performance in the refining segment.

The marketing segment reported healthy performance on margin expansion due to price hikes undertaken post the Karnataka assembly elections. Marketing volumes grew 7 percent YoY (up 2 percent QoQ) to 9.4 MT. Refinery throughput remained flat YoY at 4.6 million tonne per annum (MTPA) but rose 3 percent QoQ.

The management expects its operational efficiency in power consumption and capacity utilisation to continue, which would protect margins. It also expects better performance from the refining and petchem projects

Outlook

Net marketing margins for petrol and diesel have been negative or weak around Gujarat, Bihar, Uttar Pradesh and Karnataka assembly elections. Given this trend and manipulation of marketing margins of OMCs, we remain cautious on the sector. With upcoming state and general elections, performance of the marketing segment might get impacted. OMCs have been left untouched from the subsidy burden for now but upstream oil companies may be asked to absorb the same. The situation might change if global crude price harden further closer to the elections.

The current subsidy provision on cooking fuel is inadequate at current crude prices. If crude prices sustain at current levels then there might be delays in subsidy payments from the government, which could lead to higher interest costs.

Although there has been a steady uptick in the domestic prices of diesel and petrol post the Karnataka assembly elections, there is still immense skepticism in the market towards policy changes on capping of fuel prices. This has led to a steep correction in stocks prices, with OMC valuations looking optically attractive. Notwithstanding the valuation comfort, policy uncertainty in light of high crude prices, inflationary environment and populism in an election year make us cautious on this space.

Follow @RuchiagrawalFor more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.