Net interest margin (NIM) at most Indian banks improved on a year-on-year basis in the April-June quarter as the Reserve Bank of India (RBI) kick-started its rate hiking cycle, according to banking analysts Moneycontrol spoke to on Wednesday, August 10.

Bankers and analysts expect the banking sector’s NIM to improve further in this financial year but the pace could slow as banks begin to mobilise deposits at a faster pace.

NIM is the difference between the interest income earned and the interest paid by a bank relative to its interest-earning assets like cash. Typically, in a rate-hike cycle, banks are quick to pass on the impact of a repo rate hike to its customers by increasing the lending rate. However, the rate transmission on deposits is not as prompt. The difference is reflected in the margins.

Also read: Q1 marks growth phase for India’s banks but warts are visible too

In the April-June quarter, the RBI hiked the repo rate—the rate at which it lends funds to banks—by 90 basis points (bps) in its bid to combat inflationary pressures in the economy. One basis point is one-hundredth of a percentage point. Following the rate hike, banks were quick enough to pass the rate hike on to its customers, faster than the increase in deposits. In the same quarter of the previous financial year, the repo rate was at a record low of 4 percent due to uncertainties posed by the COVID-19 pandemic.

“Banks raise lending rates in anticipation of interest rates rise and deposit rates hike follow with a lag. This has been happening since the interest rate cycle started turning and has helped the banks improve NIMs in Q1FY23,” said Aditya Acharekar, associate director at CARE Ratings.

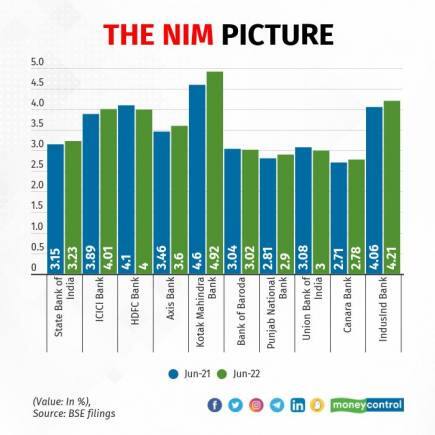

As a result of the RBI’s rate increase, ICICI Bank reported a 12 bps year-on-year increase in NIMs to 4.01 percent in the April-June quarter, while State Bank of India (SBI), the country’s largest lender, reported an 8 bps jump to 3.23 percent. Private lenders such as Kotak Mahindra Bank, Axis Bank and IndusInd Bank reported a rise in NIMs on a year-on-year basis in the fiscal first quarter, while state-run peers like Punjab National Bank, Bank of Baroda and Union Bank of India also reported an annual increase.

However, some banks did report a sequential decline in NIMs. For example, SBI’s NIM dropped on a quarter-on-quarter basis in the reporting quarter mainly due to growth in the low-margin overseas book, analysts at Emkay Global Financial Services said in a note. HDFC Bank also reported a sequential decline in NIMs as its business mix changed substantially, the lender’s managing director and chief executive Sashidhar Jagdishan said in an analysts’ post-earnings call. Jagdishan had guided that NIMs will remain muted for the next 12-18 months.

What lies ahead?

Often, monetary transmission happens based on the prevailing liquidity situation. Transmission works better in a relatively tight liquidity scenario.

The RBI, in its bid to withdraw pandemic-era surplus, is expected to continue liquidity absorption in the coming quarters. Already, the net liquidity absorbed by the RBI as on August 9 was Rs 1.36 lakh crore, down from Rs 5.49 lakh crore as on May 9, indicating that liquidity is not as much in surplus as before. The monetary policy committee is also expected to hike rates further. Economists expect the repo rate to be hiked at least to 5.75 percent by December from 5.40 percent currently.

Till now, a large part of banks’ advances were already linked to the marginal cost of fund-based lending rate (MCLR) or external benchmark-based lending rate and were getting re-priced at a relatively faster pace even as the term deposit base was re-priced gradually. MCLR is an internal reference rate for banks set by the RBI to help determine a minimum interest rate on various types of loans. Under the MCLR regime, banks typically adjust their interest rates as soon as the repo rate changes.

However, with an expectation that credit offtake will continue over the coming quarters and a fall in liquidity surplus, there is also a probability that banks will start mobilising deposits at a faster pace by offering higher rates. This could put pressure on their margins.

“By Q4 (January-March), we expect the rate hikes to have reached a level beyond which the RBI will not use rate hikes as a tool and would use liquidity management tools to moderate inflation,” said Vivek Iyer, partner and leader, financial services risk, at Grant Thornton Bharat. “It is during this time period that we can see some deposit mobilisation increases and a corresponding increase in the deposit rates.”

During the first quarter, most banks had guided that the improvement in NIMs was likely to continue, but the pace may slow. For instance, Punjab & Sind Bank MD and CEO Swarup Kumar Saha had told Moneycontrol that the lender’s NIMs should be above 2.90 percent, with an upward bias of up to 2.95 percent in the coming quarters. The bank’s NIM stood at 2.92 percent in April-June.

Large versus small

Lenders that have a large share of low-cost current and savings account deposits have more heft on margins as savings deposit rates are seldom changed. In contrast, those that depend more on wholesale deposits or even retail term deposits may need to hike deposit rates quicker to attract deposits.

NIMs are largely dependent on the liability mix and pricing mix of the assets. Depending on each bank’s growth ambitions, certain banks may choose to mobilise deposits by adopting a relatively more aggressive pricing strategy, which could limit the upside on NIMs, analysts said.

“We expect banks to increase their deposit rates to maintain their current account-savings account ratio or mobilise funds through term deposits,” said Punit Patni, a research analyst at Swastika Investmart. “The drive to mobilise deposits might lead to a rate war sort of situation and this competition will impact the NIMs negatively, especially in the case of mid- and small-sized banks.”

According to Hemali Dhame, associate vice-president, research, Kotak Securities, large banks are better placed at cost-efficient deposit mobilisation. However, mid-sized banks' deposits remain expensive versus large banks, she said.

“The costs are sticky when liquidity is unfavourable, generally. Hence we understand NIMs would be dependent on bank-specific strategies,” added Dhame.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.