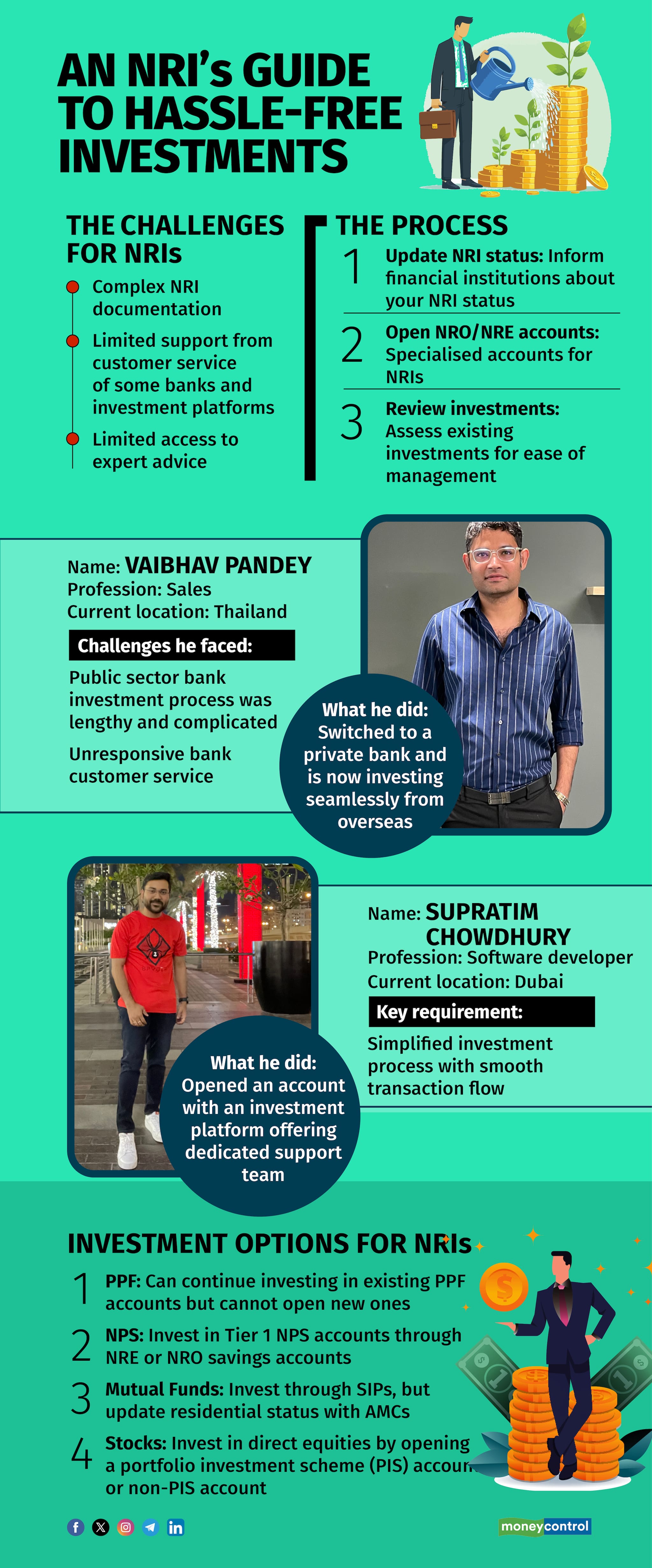

When Gurugram-based sales professional Vaibhav Pandey moved to Thailand in 2023, he wanted to continue his investments in India, thanks to the lucrative returns on offer compared to other developing countries. He wanted to ensure that his portfolio was well-diversified across geographies. Pandey initially decided to continue with investments through a public sector bank where he was holding an account, expecting a hassle-free experience. However, his experience was far from smooth.

“The investment process through public sector bank was lengthy and complicated,” says Pandey. He also experienced customer service that was not adequately responsive, making it difficult for him to get his investment related queries addressed or resolve issues.

Frustrated with his experience, Pandey decided to route his investments through a private bank account. “Now, investing has become quite seamless,” says Pandey.

Kolkata-based software developer Supratim Chowdhury, settled in Dubai since September 2023, was clear while moving abroad that he wanted to invest through a tech-efficient platform that offers a simplified process. “As a Non-Resident Indian (NRI), I require investment solutions that cater to my unique needs. So I opened an account with an investment platform that provided a dedicated support team adept at handling complexities of NRI documentation for tasks like KYC registration, bank detail updates or nominee updates in investment folios,” says Chowdhury.

Navigating the complex procedure challengeLike Pandey, NRIs encounter several hurdles when investing in India. “This includes limited access to expert investment advice and personalised support through virtual meetings is a significant concern,” says Harsh Gahlaut, Co-founder & CEO, FinEdge, an investment platform. Additionally, most digital platforms fail to provide dedicated service managers to help with intricate NRI documentation. Furthermore, NRIs need a reliable, convenient, and process-oriented tech platform for effortless transactions.

“If you prefer robo advisors or DIY investment platforms, then remember they are primarily transactional, lacking the personalised support and customised investment solutions that NRI investors require, especially when dealing with complex documentation," notes Gahlaut. Additionally, traditional wealth management firms have limited reach and often impose investment thresholds, restricting options for NRI investors.

Also read | Banking for NRIs: Tips for Indians moving overseasEvaluate existing investments before moving abroadWhen assessing your existing investments, prioritise ease of access and management. “Consider the feasibility of maintaining assets like mutual funds, stocks, fixed-income products, or real estate from abroad. If they demand frequent attention, it may be wise to divest unless you have a reliable support system in place," advises Amit Suri, Founder of AUM Wealth.

Real estate, while valuable for rental income or appreciation, can be a hassle to manage remotely. “Selling before relocating abroad can simplify your finances and eliminate concerns about bills, taxes, and maintenance,” says Suri. However, take a call on the basis of your long-term plans and your outlook for your property, among other factors.

Updating your financial institutions about your NRI status is crucial for efficient asset management. Chowdhury's case highlights the importance of this step. He notified his bank about his NRI status, opened specialised accounts (NRO and NRE), and completed necessary documentation, including FATCA and KYC forms, to ensure a smooth transition.

“Updating your residency status is not limited to your bank. It's essential to notify your stockbroker, asset management companies (AMCs), and insurance providers about your change in status," says Suri. Additionally, ensure your KYC documents are updated to reflect this change, facilitating smooth transactions and regulatory compliance.

Be aware that your non-resident status can also impact your tax responsibilities, so stay informed about applicable tax regulations to avoid any unexpected liabilities.

Also read | Careful, NRIs: This is how to ensure your power of attorney is a tool, not a trapHow to invest in Indian stocks and mutual fundsNRIs can invest in direct equities through their NRO savings account and trading account opened in NRI status. “Investments in the secondary markets in India from the NRE savings account requires the NRI to open a Portfolio Investment Scheme (PIS) account, as mandated by the Reserve Bank of India (RBI),” says Pranav Mishra, Head – Distribution, Consumer Bank, Kotak Mahindra Bank. All investments done from the NRE account will be subject to the entity level/sectoral threshold restrictions, he adds. Further, an NRI can hold only one PIS account with banks across India.

"As an NRI, you can continue investing in mutual funds through SIPs by opening an NRO or NRE account. However, it's crucial to update your residential status with all AMCs," notes Arnika Dixit, President and Head -Branch Banking of Axis Bank.

Before investing verify whether or not the fund house accepts NRI investments, Suri cautions. Also, review each mutual fund's terms to ensure they meet your post-relocation objectives, considering factors like redemption ease and alignment with your long-term goals.

Also read | What NRIs need to know about investing via mutual funds in IndiaA guide to NRI investments in India: PPF, NSC and NPSBoth Pandey and Chowdhury continue to maintain Public Provident Fund (PPF) accounts in India. “It’s important to note that NRIs are not allowed to open a new PPF account. However, they can continue to invest funds in an existing PPF account, opened as a Resident Indian, until the maturity period of 15 years,” says Mishra. During these 15 years the account is active, NRIs earn the same interest rate as resident Indians. The maturity amount will be transferred to the NRO savings account of the NRI. As per a recent guideline effective from October 1, NRIs are not permitted to extend their PPF investments in India beyond the initial 15-year period.

Also, NRIs are not permitted to invest in National Savings Certificates (NSCs). However, NSC investments done as a Resident Indian can be held till maturity, Mishra adds.

“NRIs are permitted to invest in Tier 1 National Pension System (NPS) accounts, from NRE or NRO savings accounts,” says Mishra. The investor needs to be between 18 and 60 years of age and should hold a valid PAN card.

“NPS offers a structured retirement solution that can grow over time, creating a reliable financial buffer while you’re overseas,” says Ajay Lakhotia, Founder and CEO, StockGro, a stock market learning platform. Taking advantage of these investment avenues can help you maintain a strong, India-based financial corpus for retirement, even while relocating abroad.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.