Jitendra Kumar GuptaMoneycontrol Research

Companies linked to the capex cycle with high quality balance sheet is a rare find in India. Savvy investor Porinju Veliyath’s recent pick is one such construction company - Raunaq EPC International. The investor has recently bought 35000 shares recently at Rs 143.26 a share.

Raunaq EPC International Limited, engaged in turnkey execution of Engineering Projects, is a group company of the Surinder P Kanwar Group. It has a similar pedigree as some of the established names like Bharat Gears Limited. Raunaq caters to power, chemicals, hydrocarbon, metal and automobile sectors and has a clientele which is made up of NTPC, BHEL, Adani Group, Jindal Group, L&T, Reliance Energy, Indian Oil, HUL etc.

Typically, a large engineering company will not have all the engineering capabilities and abilities to execute an order. It will mostly divide the scope of work like civil work, electric work, security, communication and will outsource to smaller players who have certain domain expertise and execution capabilities. This is where one could see smaller players or companies making their mark.

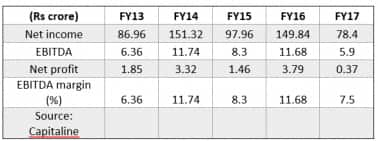

While industrial slowdown had impacted revenues in the past, Raunaq's balance sheet didn't take a hit. It has been selectively bidding for projects which are margin-accretive.

Even in 2013, its worst year, when revenue declined by 26 percent, it was able to maintain an operating margin of 8 percent as against an average of 9.5 percent seen in the last five years.

Typically, companies compromise on margins to bid aggressively. Many of them offer extended credit period to get more work, which leads to higher working capital and debt. But Raunaq kept its focus on good projects and clients. Its debtor turnover ratio at an average four times or around 90 days in last five years is among the best in the industry. This is precisely a reason that its debt in the last five years remained in the region of about Rs 8-10 crore as against an average net worth of Rs 35 crore. In fact, on a net basis (after accounting for Rs 13 crore cash or 25 percent of market capitalisation in the books in FY17) it is a zero-debt company.

While there is no great visibility on industrial capex picking up immediately, the only silver lining is that the company is well managed. If the cycle reverses it will be one of the early beneficiaries and possibly deserve higher valuations, which the market may not give today in the backdrop of falling return ratios and profitability. Over the last five years, its return on equity has fallen (about 4 percent in FY17 as against 22 percent in FY12) because of the dilution as well as drop in profits from Rs 6.5 crore in FY12 to Rs 2 crore in FY17.

Auto Component: A Drag on Business

Part of its worry also stems from auto component business which manufactures clutches for commercial vehicles in the replacement market. Auto component business, which is operated by a 100 percent subsidiary and accounts for 30 percent of the total revenue, incurred losses to the tune of Rs 1.04 crore in FY17 as against a loss of Rs 59 lakh in FY16.

The company is now extending its product range and is likely to cater to heavy commercial vehicles and at the same time engage with the domestic and foreign OEMs. However, progress needs to be monitored closely as this could have a huge impact on the future profitability of the company.

Importantly, in its core engineering business, the competitive intensity is waning with many engineering companies struggling to service their debt. Should the investment cycle turn, which is expected over the next 12-18 months, the company will hopefully generate better returns and it deserves a higher valuation.

Today, after the stock hit a 10 percent upper price circuit at Rs 169, the company is commanding a market capitalisation of about Rs 52 crore (promoters hold 67 percent), which gives a valuation of about 26 times its FY17 earnings.

While prima facie this appears to be on the higher side, the same is on account of falling earnings, which may not give a true picture of the future potential/opportunities.

The company is sitting on a net worth of close to Rs 48 crore as against a market capitalisation of Rs 52 crore, which is reasonable. Even at 15 percent return on equity, it has the potential to generate Rs 7-8 crore of annual profit, which can take the current price to earnings ratio to 6.5 times to 7 times. However, all that is contingent on revival in the capex cycle.

What investors got to keep in mind is that it is a scalable business and given the balance sheet strength, it can bid for bigger projects. While private capex cycle is going through a prolonged pause, government initiatives like Make In India, power to all, building 100 Smart Cities, industrial corridors and Sagar Mala project do give us hope that all is not over.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.