Stashfin, a neobank, has recently launched a new credit line card. Called #LiveBoundless, this card is targeted at the woman shopper. It is aimed to work a little differently from the typical credit cards that target all shoppers. The #LiveBoundless card has tie-ups with clothing, cosmetics, electronics, and kitchen appliances brands that are specific to women, besides offering cashback and discount benefits.

What does #LiveBoundless card offer?

To differentiate itself from scores of credit cards out there that pander to the shopaholic, Shruti Aggarwal, Co-Founder, Stashfin, says that this card is aimed at the salaried millennial woman and one who is new to credit (NTC). The card is open to all women, irrespective of whichever bank account she holds. All she needs is an internet banking facility and a smartphone.

After your application gets approved, you get a virtual card in your Stashfin app and also a physical card.

Just like any other credit card, the #LiveBoundless card offers reward points; 1 ‘Stashcash’ point for every Re 1 spent. A welcome gift of 2,000 Stashcash points awaits you at the time of enrolling. On purchases, the card users get 1 percent cashback on every online/retail spend. The card offers a credit limit of up to Rs 10 lakh. “The applicant needs to share a bank statement while applying for the card to evaluate eligibility and credit limit,” says Aggarwal.

What works

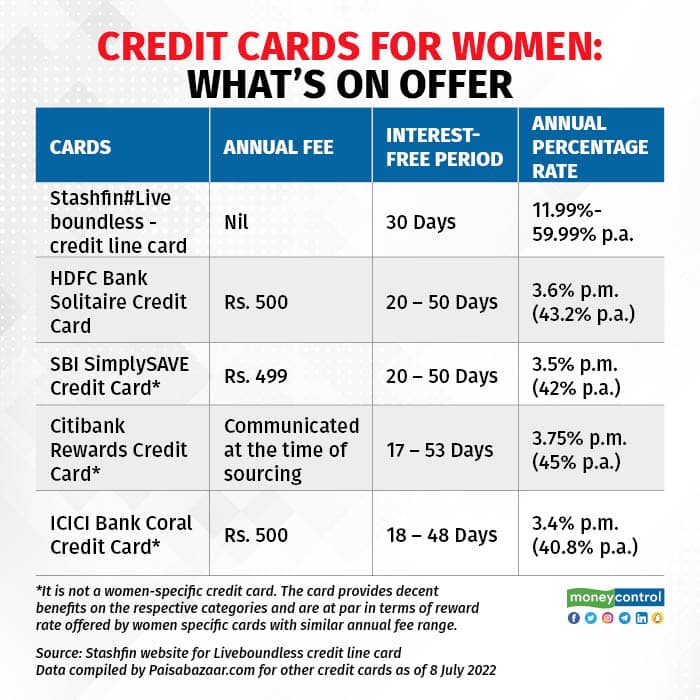

There is no joining fee and annual fees. The card is lifetime free.

Unlike typical credit cards, cash withdrawals are free. Compared to this, for instance, SBI credit cards charge a transaction fee of 2.5 percent or Rs 500 whichever is higher for withdrawal using the ATM.

Every six months, Stashfin will review the user’s credit profile. Based on this review, it could change the interest rate, tenure and credit limit. This can work in your favour if you are a disciplined user. But if your spending goes awry or you consistently default or revolve your credit, the review can work against you.

Annual interest rates on outstanding dues are between 11.99 percent per annum to 59.99 percent per annum. Aggarwal says that charges are higher for those without a credit history. Here again, this could work for or against you, depending on your credit history. A processing fee (3 percent to 5 per cent) applies if you do not pay within the credit period.

“The interest rates seem lower than regular credit cards for customers with a good credit profile,” says Parijat Garg, a personal finance expert, who analyses credit cards closely. For instance, HDFC Bank Solitaire Credit Card charges 43.2 percent per annum flat interest rate on outstanding dues (refer to graphic).

“It is like a zero-cost product for users if you repay the outstanding dues on the card within 30 days of credit period,” says Garg.

What doesn’t work

For those with a good credit history, the interest rates are low. But for NTC customers, interest rates can go up to as much as 59.99 percent per annum. Garg says the card may not have much to offer to mature users who usually get high credit limits as they would already have a bunch of credit cards. Aggarwal disagrees: “Our tie-ups with brands across segments that specifically target women offer value to our customers.”

However, regulatory uncertainty has cast a cloud over cards issued by fintech firms/neo banks like Stashfin. Recently, the Reserve Bank of India (RBI) said that fintech firms cannot offer credit to customers (either through loans and credit cards) if they do not have a tie-up with a bank. At present, this guideline has affected non-bank prepaid payment instruments (PPIs) issuing cards. To be sure, Stashfin has partnered with State Bank of Mauritius (SBM) and NSDL Payments Bank. Aggarwal declined to comment on any impact of the RBI’s guidelines.

Should you apply?

This card can be a good start for women who are looking for their first credit line card. But if you are eligible for bank-based credit cards, it pays to check them out first.

Women-centric cards may offer some additional benefits to women, but credit card is a highly competitive market. Even gender-neutral credit cards can offer you a host of benefits like airport lounge usage, lifestyle benefits, and so on.

Garg warns: “The consumer should apply for such a card only if it is available at no or minimal onboarding cost, as the clarity on any impact of RBI guidelines to bank PPI-backed cards is still to emerge.”

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.