Senior citizens who have a comfortable house to live in, but are finding it hard to sustain themselves on their limited finances, have the option of boosting their monthly income. They can look at the reverse mortgage scheme, which the government of India had launched in 2007. Although the scheme has been around for many years, it has not been a popular one; banks seldom talk about it or even advertise it. But with home loan rates (though they’ve got nothing to do with reverse mortgage loan rates) now at a low, this is a good time to consider reverse mortgage if you are over 60, have a house in your name and could do with extra money.

How does reverse mortgage work?In simple words, the reverse mortgage scheme is a loan.

At the outset, the senior citizen must own a house. If you live in a rented accommodation, then you are not eligible for reverse mortgage. Based on the value of your house and its location, the bank will decide how much loan to give you. Typically, the loan-to-value (LTV) ratio is 60-80 percent. And the maximum loan amount most banks offer is Rs 1 crore, even if your property is worth much more. “The banks don’t want to over-leverage and take excess risk with this capital,” says Gajendra Kothari, MD and CEO of Etica Wealth Management. The maximum period of the loan offered is 10-20 years by most banks. But there is a sweetener and here’s where it differs majorly from all other types of loans.

The borrower does not have to pay back the amount. The legal heir has to. “If the borrower outlives the tenure of the loan, the lender will just stop making periodic payments. However, the borrower can continue to occupy the property,” says Raj Khosla, founder and managing director of MyMoneyMantra.com. Either the bank sells the property after the senior citizen’s demise or the senior citizen’s legal heir or nominee pays back the entire loan amount and gets to keep the house.

There are two payout options offered: one is a regular mortgage loan directly from the bank and other is an annuity based loan.

In an annuity based loan, the bank sanctions you a lump-sum amount, but gives it to an insurance company. The insurer calculates the annuity and then pays you either monthly, quarterly, half-yearly or yearly. “The annuity payout option is not recommended as the rates are not attractive, so payment will be quite low. Also, the annuity from insurance will be taxable,” says Kothari. However, the loan amount received by the borrower from the bank in the form of monthly instalment or lump-sum is not treated as the income earned by the senior citizen and is exempted from taxation.

There are no pre-payment charges on the reverse mortgage loan, if the borrower decides to repay. “If the prepayment of the reverse mortgage loan is done by transferring the loan to another lender, then the lender may charge a penalty of 0.5-2 percent on the balance amount,” says Gaurav Gupta, Co-founder and CEO of MyLoanCare.in.

Lack of awareness and an emotional bonding to our homes have been the main reasons why reverse mortgage has remained unpopular. In India, a house is considered a family asset, which is typically passed on to our children or legal heirs.

The scheme is also perceived to be complicated to understand. Besides, banks don’t really advertise it. And that is not surprising. Consider this: a senior citizen takes a reverse mortgage loan for 10 years and ends up living for another 40 years. There’s nothing that the bank can do to recover its amount. It has to wait till the borrower dies. Both private and state-owned banks offer reverse mortgage schemes. At times, the product may not be advertised on the bank’s website, if you walk into their branches, you can get the details.

Also remember, despite mortgaging the property with the bank, the responsibility of maintenance still lies with the home owner. You will be liable to pay the property taxes, carry out periodic maintenance activities, and even buy a property insurance if the lending bank insists, from your own pocket. You also cannot sell the property during your lifetime, or till you repay the loan.

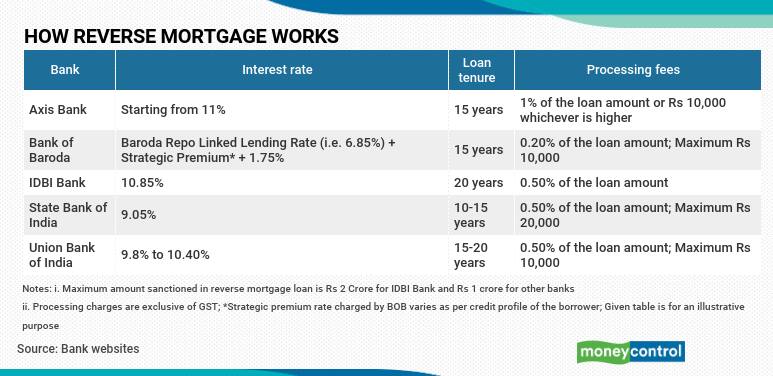

Is this a good time to go for reverse mortgage?Yes, because interest rates are low. And now they are also linked to external benchmarks, so rates are transparently fixed. When any there is a downward movement of interest rates, it helps the borrower. For instance, State Bank of India (SBI) has linked the interest rate on reverse mortgage loan with repo rate and the existing interest rates are 8.05 percent for SBI pensioners and 9.05 percent for other borrowers. With change in external benchmark rates, this rate will also change.

Khosla says, “I strongly recommend the reverse mortgage scheme at current rates to elderly people because it gives supplementary retirement income and allows them to live a life of their choice.” He adds that this scheme is best suited for retired house owners who do not have a residual monthly income or if their annual income is under stress due to low returns from fixed deposits and other debt schemes.

Also read: Life stage financial planning: For a fulfilling retired life in your 60s

Just remember that your bank typically revalues your property once in about five years, to ensure the property’s value is around the same as what it was at the time of loan disbursal. That’s because in most cases the house becomes the bank’s property after the demise of the senior citizen, which it needs to sell to realise the loan value. “The property must have a re-sale value after many years,” adds Kothari.

If you are finding it difficult to make your ends meet month-on-month, you can opt for a reverse mortgage loan. Just stay away from unregulated lenders. “Always deal with RBI registered banks and housing finance companies (HFCs); be careful from whom you are availing the reverse mortgage loan,” says Khosla.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.