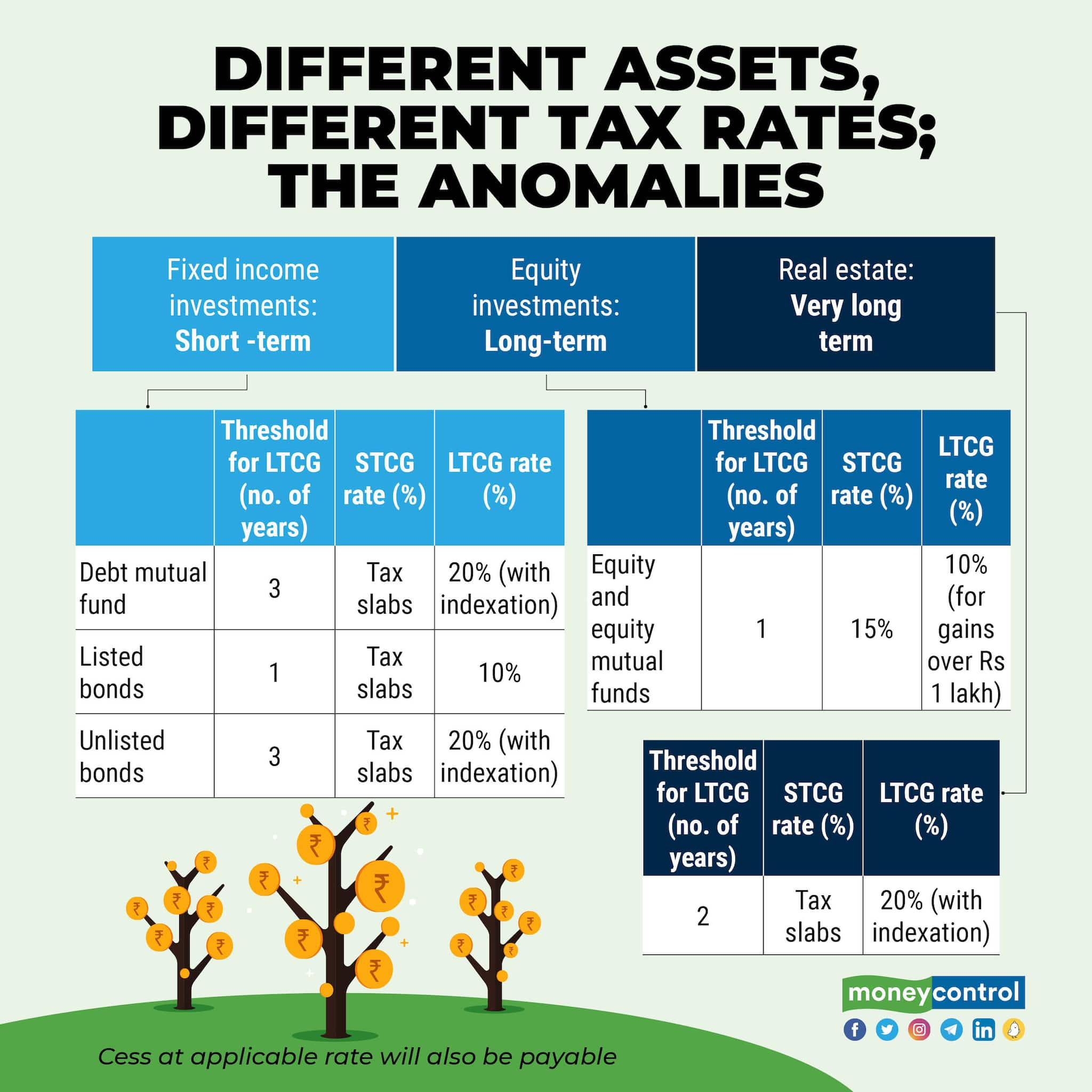

If you buy a listed bond, then you pay long-term capital gains (LTCG) tax of 10 percent, if you hold it for more than 12 months. But if you sell a debt mutual fund, the threshold for paying capital gains tax goes up to three years. Sell your debt fund after three years, and you pay LTCG tax of 20 percent (with indexation). Short-term capital gains (STCG) are taxed at your slab rate.

Even unlisted bonds are taxed (capital gains) at the same rate as debt MFs, and the same cut-off of three years applies.

Will Budget 2022 address the anomalies in capital gains taxation?

Longer time horizon for long-term investments

Some tax experts, for long, have demanded a more rational way of deciding the tenure for which the investments must be held on, to decide when they qualify for short-term and long-term capital gains taxation.

The problem doesn’t end with just the tenure. The capital gains tax rates differ even within the same asset class. For example, STCG tax on stocks and equity mutual funds is 15 percent. For bond funds and bonds (listed and unlisted), investors pay, presently, taxes as per their income-tax slab rates; these can go up to 30 percent in cases of many tax-payers.

Also read: How gains from mutual funds are taxed

Rajesh Gandhi, Partner, Deloitte India says, “There is a need to further encourage direct investments in bonds and government securities especially from domestic investors. Though many investors buy listed bonds with an idea to hold for long term, when they sell it in less than one year, they end up paying short term capital gain tax as per slab rates. That could be brought down to 15 percent or so in line with tax rate for equities.” Also for unlisted bonds and debt mutual funds the investment should be construed long term if held for more than 12 months, as is the case with equities. This will also result in rationalization and simplification of the tax rules for different asset classes, he adds.

The Association of Mutual Funds in India (AMFI) in its proposals for Union Budget 2022 has requested for treating investments in non-equity oriented mutual fund schemes which invest 65 percent or more in listed debt securities as long term, if they are held for more than 12 months or increasing the minimum holding period for direct investment in listed debt securities or and zero-coupon bonds (listed or unlisted) to 36 months to qualify as long-term capital asset.

Gandhi is not alone asking for reduction in holding period for bonds to become long term capital gains. Gains booked on real estate such as land and building held for 24 months or more are treated as long term capital gains. “Investments in real estate is generally done with a long term view whereas debt is preferred to make short term investments. The gains booked on real estate should be considered as long term capital gains if it is held for 60 months. The investments in debt should be considered as long term asset if held for 12 months,” says Balwant Jain, a Mumbai based Chartered Accountant.

Will a longer threshold make equities unattractive?

However, not many agree with such statements.

For starters, policymakers are usually keen to channelize savings. “Government has rarely managed to achieve the disinvestment targets in budget since they were introduced. This year too government have a long pipeline of disinvestments. Government cannot afford to tinker with the equity taxation,” says a tax expert on the condition of anonymity. Increasing the holding period to qualify for long term capital gain will make equity investing unattractive. Investors won’t jump into equities for high returns alone. They will also ask for better tax treatment for the risks they take, he adds.

Bonds issued by companies in the infrastructure or priority sectors are another focus areas of governments, typically, for attracting retail money. Here, experts say that incentives work. Also, most Indians still do not own equities. As per data presented in Parliament, there were only 7.3 crore demat accounts as on October 31, 2021, although the current Covid-19 pandemic and work-from-home scene pushed many first-time investors in the stock markets.

Still, Vinayak Savanur, Founder and CIO at Sukhanidhi Investment Advisors says that equities should be taxed in such a way as to ensure that investors do not speculate. “The holding period of stocks and equity mutual funds needs to be increased to 60 months to be eligible for concessional rate of tax charged on long-term capital gains. Also the long-term capital gains tax in such case should be brought down to 5 percent from extant 10 percent,” he says.

Connecting risk-reward and tax rates

Akhil Chandna, Partner at Grant Thornton Bharat LLP is of the opinion that risk-reward relationship need not have an impact on taxability in the hands of taxpayers based on the type of asset and categorization of gains as long term and short term. However, he hopes that tax rates are rationalized, especially to remove hardship for individuals in lower tax brackets. “The rates of taxes are supposed to be concessional for individuals in higher tax slabs, however for the taxpayers at lower slab rates wherein the effective rate of tax is lower due to eligible deductions or exemptions, the current rate of tax on capital gains (10 percent, 15 percent or 20 percent or at applicable tax slab rates) can be considered as very steep,” he adds.

For a person in the 5 percent slab, short-term capital gains on equities should be 5 percent and not 15 percent.

For all news and updates related to the Budget 2020 follow our Budget page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.