Shares of Tata Motors’ commercial vehicle arm made their market debut on the NSE on November 12, listing at Rs 335 per share, a 28.5 premium premium over the discovered price. The listing marks the completion of Tata Motors’ demerger, separating its passenger and commercial vehicle businesses into two distinct entities.

Since Tata Motors has announced a major restructuring splitting its business into two listed entities, one focused on Passenger Vehicles (PV) and the other on Commercial Vehicles (CV), investors have been curious not only about business strategy but also about their tax position. After all when you hold shares in the original company and it gets divided, what cost basis do you apply when the new company’s shares arrive in your demat account for taxation purposes?

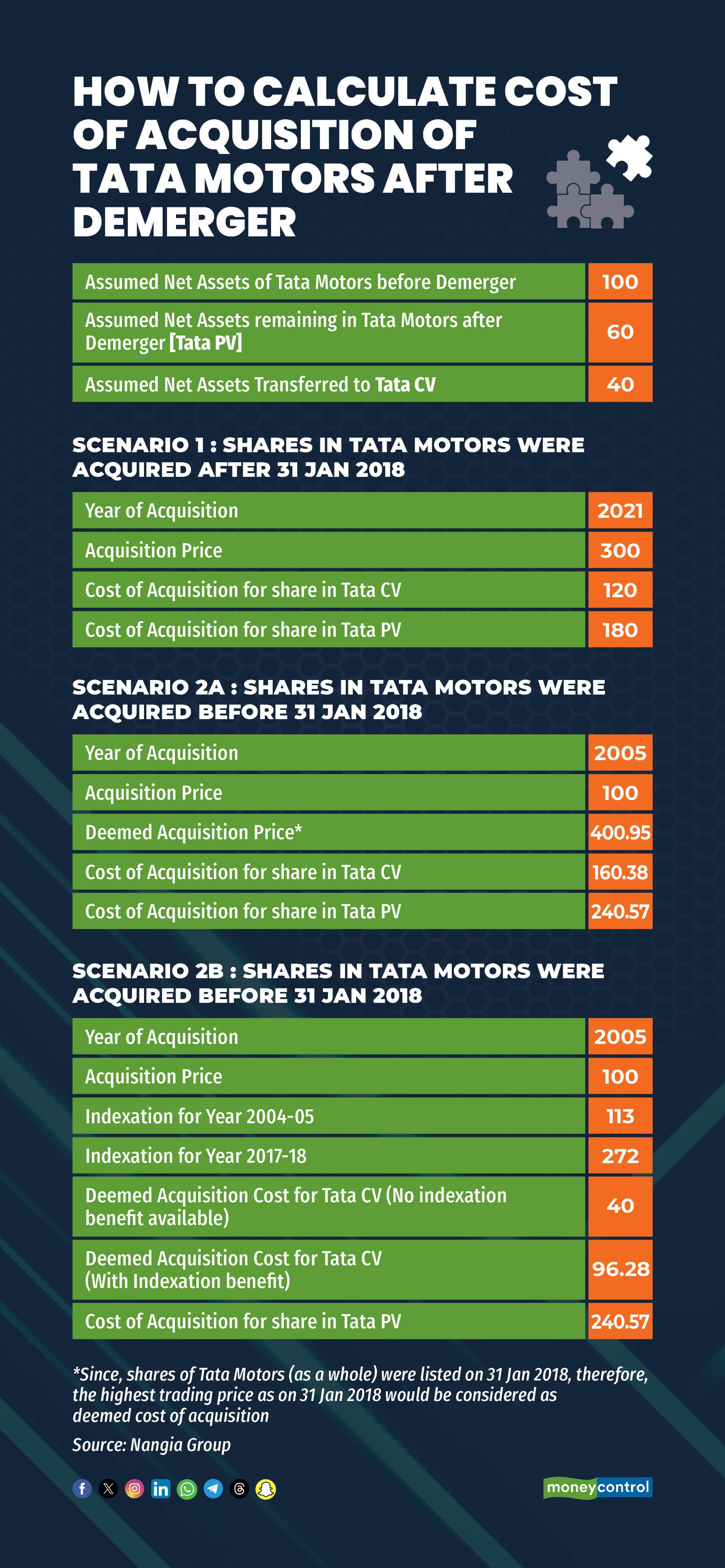

Abheet Sachdeva, Partner, Nangia Group explains that under the Income-Tax Act, when a company undergoes a demerger, the original cost of acquisition of your shares in the parent company must be apportioned between the demerged (old) company and the resulting (new) company. The formula is based on the ratio of: Net book value of assets transferred : Net worth of the demerged company as a whole before demerger.

In plain terms: if the parent company had, say, a net worth of 100 units and you know the portion of assets that moved into the new company is 40 units, then the ratio is 40:100 = 40% to the new company, and 60 percent remains with the old company.

For Tata Motors, the demerger was structured such that each shareholder of the parent company received one share in the CV entity for every one share in the parent.

In the tax framework, you would apply the cost split ratio once the company announces how much of its net assets were transferred to the CV business. Suppose that after accounting for all assets and liabilities, 40 percent of the parent company’s net assets were carved out into the CV business and 60 percent remained in the PV business.

Then 60 percent of your original cost of Tata Motors shares becomes the cost of acquisition for your shares in the PV entity and 40 percent becomes the cost of acquisition for your shares in the CV entity.

Another key piece is grandfathering. In 2018 the tax law introduced a “grandfathering” rule for listed shares held as on 31 January 2018. If shares were listed on that date, you could use the fair market value (FMV) on that date instead of your actual purchase price for computing the cost of acquisition. But if you acquired shares before 31 January 2018 and the company got listed later, you could use indexation.

In the case of the new CV entity, since the shares did not exist on 31 January 2018, you may not directly apply the FMV benefit for the CV shares. Therefore, for the resulting company you may use the proportionate cost on the basis of cost indexation. "Income tax law also provides for cost-reset in case of companies (i) where shares are listed as on 31 Jan 2018 or (ii) where shares were acquired on or prior to 31 Jan 2018 and the company was listed thereafter. In such scenarios for case (i), FMV of shares shall be the highest price quoted on a recognised stock exchange as of 31 Jan 2018, shall be available as cost of acquisition, where as in case (ii), cost indexation up to FY2017-18 shall be available," says Sachdeva.

Interestingly, in the present demerger, since the shares of the Resulting Company / New Company may not be said to have been acquired before 31 Jan 2018, the benefit of FMV as discussed may be said to be not available. Thus, proportionate original cost of shares would be available as cost of acquisition of shares. However, alternatively, with the application of grandfathering provisions under Income tax laws, the FMV testing has to be done on the existing shares of the Demerged Company/ Old Company and proportionate cost of those shares shall be considered as cost of acquisition of shares in Resulting Company/ New Company, explains Sachdeva.

Why this matters to investorsWhen you eventually sell either the PV or CV shares, your capital gains will be calculated using the cost of acquisition for each entity. Because the demerger itself is tax-neutral under section 47 of the I-T Act, you don’t pay tax when the shares are allotted to you.

Also, your holding period for the new shares continues from your original purchase of the parent shares.

The demerger of Tata Motors into PV and CV entities doesn’t change what you paid for the original shares, it just splits that cost between the two new stocks in a defined ratio based on your date of acquisition.

For the CV side you’ll use your apportioned original cost; for the PV side you may have eligibility for FMV under the grandfathering rules if you held shares before the cut-off.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.