Highlights:

- CPC volumes impacted by import restriction; sharp sequential improvement in profitability

- High-cost inventory continues to be a drag; margin expected to normalise by end of H1 CY19

- Better realisation in advance materials and surge in cement volume key positives

- Capex projects on track; new SEZ facility to be optimally utilised

-------------------------------------------------

Rain Industries’ Q1 CY19 earnings was impacted by weak performance in carbon and advanced materials segments, but was partially offset by higher volume growth in the cement segment. Both carbon and advanced materials segments witnessed lower volumes, realisations and increased raw material costs.

Also read: Goa Carbon: Unfavourable supply-demand balance weighs on Q4 margin

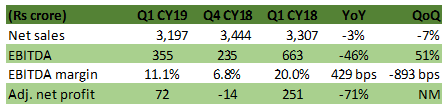

Financials at a glance

Source: Company

Product sales volume trend Source: Company

Source: Company

Key negatives

Value chain of carbon products (67 percent of Q1 CY19 Sales) -- CPC (calcined petroleum coke) and CTP (coal tar pitch) -- continues to witness several challenges. First, given the import ban on CPC, the company is not able to undertake blending in India. This doesn’t augur well for the capacity utilisation of the company’s CPC plant in the USA from where it imports, blends in India and then sell it to customers in a cost-effective manner.

Second, due to new CPC capacity commissioning in China there is an adverse impact on the supply-demand balance, leading to lower pricing trend for CPC.

Third, dynamics for the aluminium end-market are not encouraging, which puts further pressure on the carbon product prices. Smelter restart in North America has been delayed and demand from China and Europe had slumped, particularly from the automobile industry.

Fourth, the company continues to hold high-cost inventory, which impacts profitability. On account of these factors there has been a de-growth in carbon product volume sold and a sharp decline in EBITDA per tonne.

Sequentially, however, profitability per tonne is improving as the impact of high-cost inventory has started moderating.

Also read: Adverse SC action has material impact on business model

Key positives

Advance materials segment (24 percent of sales) witnessed lower volumes due to sluggish growth in the European automotive industry and in demand for resins. However, this segment continued to witness better product price realisation trends.

Performance of the cement business (nine percent of sales) improved due to increase in sales volumes in all major markets

OutlookSequentially, there was a dip in sales volume for carbon products, which can largely be attributed to timing of export shipments. Directionally, the company is quickly moving past the regulatory headwind of GPC import quota.

The management is looking at ways and means to operate its Indian CPC plant at 100 percent utilisation by buying low grade petcoke from Indian market and processing it for calcination purposes.

High-cost inventory for both carbon and advance material segments are expected to get exhaust by the end of Q2 CY19. An improvement can already by seen in the sequential jump in EBITDA margin, which should get closer to normal levels (about 18 percent) in H2 CY19

The management said its Visakhapatnam expansion plan for CPC is on track. The company said it should be able to operate even that plant at optimum levels despite the current GPC import quota. The Visakhapatnam facility, being under SEZ, also offers some flexibility to the company in terms of sourcing banned materials.

Unresolved factors include lower capacity utilisation in the USA CPC facility as the company is not able to import it to India for blending. Part of the idle US capacity could be deployed as and when US smelters restart and aluminium-end market prospects improve.

Improving realisation trend for the advance materials indicates strengthening of another growth lever for the company. Additional, tailwinds in the cement sector is comforting.

While we expect the next quarterly result to be subdued, we estimate that it is largely in the price as the stock trades at an inexpensive valuation (5.3 times CY19 estimated earnings). We are encouraged by the fact that business is under mend and carbon product prices are expected to stabilise by middle of CY19. The management expects pricing stabilisation in the end-market (aluminium) as the current cost of production doesn’t justify aluminium prices.

On account of such factors, we feel that the stock can be accumulated on every decline during the next 3-6 months.

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.