The International Monetary Fund (IMF), on December 19 (India time), in its Article IV consultations staff report praised Indian authorities for the way the economy is progressing. The multilateral agency expects India's GDP to grow by 6.3 percent in the current year as well as the next.

While the IMF may upgrade its growth forecast and bring it more in line with that of the government and the Reserve Bank of India (RBI) in its update to the World Economic Outlook in January, there are differences in its assessment of India and that of the authorities. Moneycontrol takes a quick look at four such key items.

Fiscal consolidationTo be fair to the IMF, it has praised the Indian government's "near-term fiscal policy which focuses on accelerating capital spending while tightening the fiscal stance". It also pointed out that the government is committed to reducing the fiscal deficit to 4.5 percent of GDP by 2025-26 from 5.9 percent this year, with the reduction to be "implemented approximately evenly" over the next two years.

However, the IMF thinks India needs to do more and needs an "ambitious fiscal consolidation path" to re-build its buffers and reduce debt in a sustainable manner.

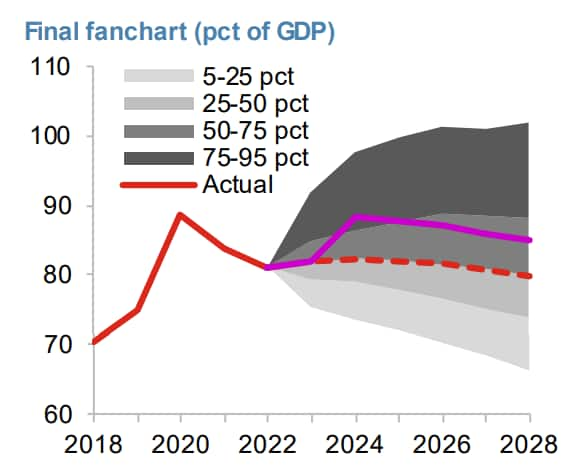

Also read: Moving the goalposts — fiscal deficit target and a 20-year delay"Based on currently announced policies, the primary deficit gradually narrows to around 2 percent of GDP by 2028-29. Maintaining this deficit and assuming nominal economic growth of 10.5 percent and interest rate at 6.25 percent implies that debt would eventually stabilise at around 57 percent of GDP. However, starting from current debt levels, this would take decades to reach; in 10 years debt is still above 76 percent of GDP," the IMF noted. It added that given the shocks India has had to face, the debt-to-GDP ratio could exceed 100 percent in the medium term.

Source: International Monetary Fund

Source: International Monetary FundIndian officials disagree. According to KV Subramanian, IMF's Executive Director for India and a former Chief Economic Adviser to the government, it "sounds extreme" that India's debt-to-GDP ratio could exceed 100 percent.

"Despite the multitude of shocks, the global economy has faced in the past two decades, India's public debt to GDP ratio at the general government level has barely increased from 81 percent in 2005-06 to 84 percent in 2021-22 and back to 81 percent in 2022-23," Subramanian said in a statement as part of the IMF report.

Foreign exchange interventionOver the years, Indian authorities’ intervention in the foreign exchange market has invited criticism, with the US even placing India on its currency manipulation watch-list in the past. This view is seemingly shared by the IMF, which said in its report that India's interventions in the forex market "likely exceeded levels necessary to address disorderly market conditions and has contributed to the rupee-USD moving within a narrow range since December 2022".

However, RBI officials were having none of it. The report noted the RBI "strongly disagreed" with the IMF's assessment and said the agency was picking data "selectively". "In their (RBI) view, (IMF) staff's assessment is short-term and restricted to the last six to eight months without any rationale for the same, and if a longer-term view of two to five years is taken, the IMF's assessment would fail. In the authorities' view, therefore, IMF's reclassification of the de facto exchange rate regime to 'stabilised arrangement' is unjustified," the report said, adding that RBI officials, in their meetings with the IMF, said the interventions were in line with the "best principles of transparency" and that the rupee's exchange rate continues to be market determined.

Trade barriersThe IMF also took issue with India's trade practices on two counts. One, it said inflation in India did not rise sharply in 2022 due to "extensive government interventions (e.g., restrictions on wheat, sugar, and rice exports, removal of tax on import of lentils, reversal of earlier increases in excise duties on petrol and diesel)". In this, it said India should unwind its "recent restrictive trade policies…expeditiously" and called on it to focus on agricultural reforms, which would provide "a more durable solution to fostering domestic food security".

Also Read: Trade measures can ease food inflation only in short run, says MPC's Shashanka BhideRejecting this criticism, Subramanian said inflation did not rise as much in India as in other countries in 2022 because of "India's sui generis economic policy during the Covid-19 pandemic that anticipated that the pandemic also presented a significant supply-side shock, which led to India implementing a judicious mix of demand-side and supply-side measures".

The second suggestion on trade from the IMF staff was to reduce India's "long-standing high tariff and non-tariff import barriers" and phase out the recently introduced restrictions on the import of laptops and personal computers. But according to Subramanian, the IMF is painting an incorrect picture of India here.

Citing the World Bank's World Integrated Trade Solution database, the former Chief Economic Adviser said India's non-tariff measures are "significantly lower than leading economies". If anything, the higher non-tariff measures imposed by leading economies are hurting India's service sector, Subramanian argued.

Financial sector risksFinally, the IMF has classified India's financial sector vulnerabilities as 'medium', warning that a "sudden increase in sovereign risk premia" could exert pressure on balance sheets and banks' appetite to lend.

Again, Subramanian dismissed this as "far-fetched" on account of India's strong fundamentals. He also disagreed with the 'medium' risk vulnerability tag given to the Indian financial sector, arguing that the sector is strong and resilient.

"The banking system is in its best shape in more than a decade. There are no major vulnerabilities, and they are well capitalised… even if an external or domestic shock occur, both banks and non-banks are well positioned not to amplify those shocks and continue to provide financial services to the real economy," he added.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.