Brokerages have mixed views on the Asian Paints stock after India's largest paints player's December revenue came marginally below expectations, while the net profit jumped more than 30 percent on-year.

On January 17, Asian Paints reported a consolidated net profit of Rs 1,475.16 crore for the December quarter of the financial year 2023-24, up 34.4 percent from the year-ago period. It reported a 5.4 percent on-year gain in consolidated revenue at Rs 9,104 crore.

As of 10.45 am, the stock was trading 2.8 percent down at Rs 3,152 apiece.

Despite a healthy demand growth, brokerages have a mixed outlook. On the positive, the net profit surged over 30 percent, as volumes clocked double-digit gains on-year, and the rural segment saw signs of recovery.

On the other hand, some experts say with the rising competition and the luxury segment seeing low interest, growth prospects are muted.

The delayed festival season, which spilled on to November, and erratic monsoon, which would have forced people to put off painting after the rains were over, were expected to buoy the report card.

While the PAT came ahead of estimates, brokerages, including Jefferies and Nuvama Institutional Equities, said Asian Paints missed its forecast due to lower-than-expected revenue. The price cuts of around 1.3 percent affected the company’s top-line.

Also Read | Asian Paints Q3: Net profit up 34% to Rs 1,475 crore, revenue up 5%; meets estimates

A delayed festival demand helped Asian Paints clock high volume growth and the outlook also remains firm.

The volume growth in the December quarter was 12 percent, led by a double-digit expansion in both rural and urban markets.

The company expects a three-four percent gap between volume and value growth because of an 80 percent contribution from the economy and premium segments compared to luxury segments.

Eye on margins

Lower raw material prices drove gross margin growth. In the December quarter, Asian Paints recorded a GM of 43.6 percent, the best in the past 11 quarters.

EBITDA surged 28 percent, led by the higher than expected GMs. The EBITDA margin came in at 22.7 percent, up 40 basis points on-year. However, the management reiterated its EBITDA margin guidance of 18-20 percent in the medium term, while Motilal Oswal has predicted a 21.5 percent margin for FY25/FY26.

According to HSBC, the margin expansion led to a strong earnings growth of around 35 percent. The outlook, based on the margins, reassures investors and “should dispel fear of price wars”.

Motilal Oswal, however, said, “The gross margin in FY25/FY26 will be the key monitorable, considering the changing competitive landscape and dwindling raw material price benefits.”

Green shoots in rural demand

The Asian Paints management was positive on rural recovery. The monsoon coupled with an uptick in government spending and moderating inflation are likely to bring in positivity for the rural economy, it said.

The decorative business saw a volume growth of double-digits in rural markets as well.

The management added that over four years, both rural and urban centres grew equally well with similar double-digit CAGR. Even tier-3 and 4 cities were seeing demand recover and showing early signs of overall recovery.

Also Read | Asian Paints Q3: Positive demand trends support growth outlook

Signs of pain?

Premium products in the decorative business grew at a slower pace, while the bath-fitting business’ revenue fell 5 percent on-year, declining for the fifth straight quarter on lower demand and EBITDA-level loss.

In rupee terms, the sales in the international arm were flat as a result of macroeconomic headwinds and inflation in key markets of South Asia and Egypt, Nuvama Institutional Equities said.

Should you buy, sell or hold Asian Paints?

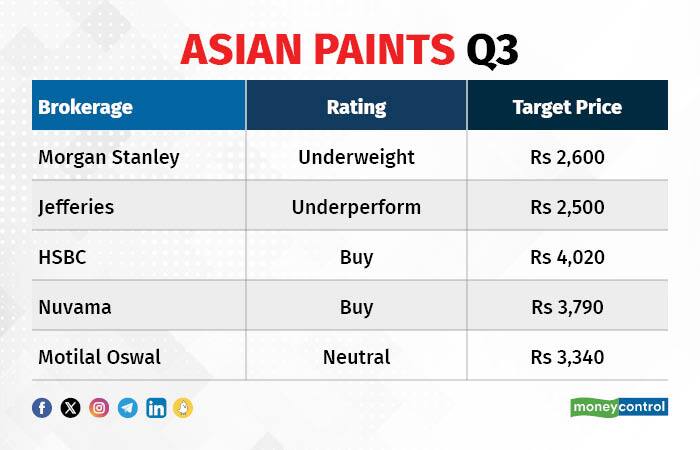

Motilal Oswal said valuations are expensive, especially given the uncertainty around the competitive pressure, with the entry of Birla Opus likely in Q4. The brokerage retained its “neutral” rating with a target price of Rs 3,340 per share.

Jefferies said the “oligopoly” of the paints sector would be challenged in 2024, as maintains its "underperform" call with an unchanged target price of Rs 2,500.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.