Madhuchanda DeyMoneycontrol Research

After days of speculation, the Internal Advisory Committee (IAC) of the RBI (comprising mainly of its independent Board Members) has, after scanning through the top close to 500 exposures of the banking system, finally arrived at an objective, non-discretionary criterion for referring accounts for resolution under the IBC (Insolvency and Bankruptcy Code).

Who qualifies for IBC?

The criteria for IBC reference are accounts with fund and non-fund based outstanding amount greater than Rs 5,000 crore, with 60 percent or more classified as non-performing by banks as of March 31, 2016.

Accordingly, 12 accounts totalling about 25 percent of the current gross NPAs of the banking system would qualify for immediate reference under IBC.

For other accounts that do not qualify under the above criteria, banks should finalise a resolution plan within six months. In cases where a viable resolution plan is not agreed upon within six months, banks would be required to file for insolvency proceedings under the IBC.

These accounts will be accorded priority by the National Company Law Tribunal (NCLT). Banks might be offered some relaxation on provisioning norms for cases accepted for resolution under the IBC.

Read More: PSU banks on brink of ticking off RBI. Find out which one needs corrective action.

Who could be probably a part of the first dozen?

While it is premature to comment on the cases to be taken up and the kind of haircut banks have to take in the resolution exercise, the RBI circular definitely puts a timeline to the entire exercise. Notwithstanding the short-term pain and the haircut, the NPA disease is likely to be largely out of the system in the next couple of years.

This should enable banks to resume lending on a cleaner basis, facilitate consolidation amongst banks (especially the PSU banks) leading to creation of larger/stronger entities, and probably kickstart the long buried capex cycle.

While we do not wish to hazard guesses on the names that are likely to find place in the “priority dozen”, we focus on the top 12 cases that are likely getting addressed on a war footing.

How will taking cases to IBC help?

Under the IBC, if a company has defaulted on a loan payment, either the creditor or the debtor can approach the National Company Law Tribunal (NCLT), the adjudicating authority to be adjudged as bankrupt.

India historically had myriad regulations to deal with insolvency. The IBC consolidates all existing laws. The other merit of IBC is that it specifies a timeframe — 180 days after the process is initiated, plus a 90-day extension for resolving insolvency.

The process is done by creating a host of new institutions like Insolvency Professionals, Insolvency Professional Agencies, Information Utilities and Insolvency and Bankruptcy Board of India, a regulator that will oversee these new entities.

There is no history to IBC so it is difficult to comment on its efficacy. However, post the NPA Ordinance, RBI will be in a position to monitor specific cases, especially the difficult cases, even when the resolution process through the IBC is underway.

There are in fact five stages in the resolution process through IBC. Once a loan default occurs, the lender will approach NCLT for initiating the resolution process. Then the creditors will appoint an interim Insolvency Professional (IP) to take control of the debtor’s assets and company’s operations. Then the creditors will collect financial information of the debtor from information utilities, and constitute the creditors’ committee.

Post that, the committee has to take decisions regarding insolvency resolution by a 75 percent majority. Once a resolution is passed, the committee has to decide on the restructuring process that could either be a revised repayment plan for the company, or liquidation of the assets of the company. If no decision is made during the resolution process, the debtor’s assets will be liquidated to repay the debt. Finally, the resolution plan will be sent to the tribunal for final approval, and implemented once approved.

Resolution or liquidation?

Referring troubled assets to IBC does not necessarily mean liquidation. There will be serious options of resolution, finding buyers and selling the assets. The valuation of assets will assume importance and RBI may resort to third-party valuers so as to make it acceptable to all concerned stakeholders.

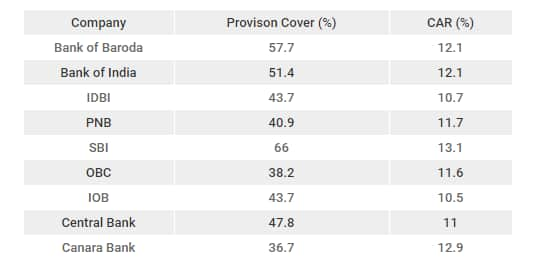

From the financial snapshot of the most troubled dozen or so companies that could be candidates for NCLT referral, one thing is clear. Banks have to be prepared to take deep haircut as resolution kicks into high gear. They can, however, look forward to some forbearance in the form of staggering the provision.

As the tentative mapping seems to suggest, large corporate lenders will be in the thick of the action in the coming one year as resolution gathers steam. From the public sector banks, Bank of Baroda, Bank of India, IDBI, Punjab National Bank, State Bank of India, Oriental Bank of Commerce, Indian Overseas Bank, Central Bank and Canara Bank are banks to watch out for. From the private sector space, it will be ICICI Bank and Axis.

Well-capitalised banks with healthy provision coverage will witness relatively lesser earnings impact of the haircut. Hence investors should place their bets wisely.

Given the attractive valuation, level of capitalisation and the upside from NPA resolution, State Bank of India and ICICI Bank prima facie look like the bigger beneficiaries, along with Axis Bank.

Investors should remember that while most banks will be sellers, some well-capitalised banks will be buyers of troubled assets at attractive long-term value. Hence, not only the troubled lenders but smart buyers like Kotak Bank should also be on the radar.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.