Madhuchanda DeyMoneycontrol Research

The last salvo has been fired, even if it is a few days too late for Diwali. After working with a piecemeal approach, the government has finally announced a mega recapitalisation package for banks. While the contours are being worked out, the Street is in a mood to party, lifting all PSU bank stocks irrespective of quality. Will the celebrations go on, or is it still necessary to winnow out the weak ones as part of your investment strategy?

The recapitalisation

The government has announced Rs 2.1 lakh crore capital infusion for state-owned banks – Rs 1.35 lakh crore from bonds, Rs 18,000 crore from budgetary support and the remaining Rs 58,000 crore through share sales.

A fiscally neutral solution (except for the coupon payment on the bonds) with minimal impact on debt-to-GDP ratio and system’s liquidity (hence largely non-inflationary) was the need of the hour.

On the face of it, the move will ease PSU banks’ capital deficiency (especially following asset quality pressure and the impending transition to Basel III norms) and marginally encourage lending. However, to start with, it will largely address asset quality stress and act as precursor to consolidation.

While RBI has stepped on the accelerator on NPA resolution by taking errant companies to the Insolvency and Bankruptcy Code (IBC), the resolution in a time-bound manner would entail a huge haircut. Globally, it has been upwards of 50 percent to 60 percent. But to offer such haircuts, the banks will require capital which they currently do not have. This really puts the Indian banks in a catch-22 situation.

Indian banks are sitting on gross NPA of approximately Rs 8.5 lakh crore and net NPA of Rs 4.8 lakh crore and quite a few state-run banks are actually sitting on negative net worth. Hence, recapitalisation is a first step in the resolution process.

Why a recapitalisation bond now?

Most Indian banks are sitting on a mountain of liquidity thanks to the demonetization exercise and lack of appetite for credit in the system. This has resulted in banks ending up investing most of this liquidity in government securities, driving the Statutory Liquidity Ratio (SLR) bond holdings of banks above the minimum requirement by up to 700 basis points. This combination of a surfeit of liquidity and weak credit demand has created a perfect backdrop to design a recapitalisation bond to address the capital problem.

How will it work?

Since the banks are sitting on surplus liquidity, recapitalisation bonds can convert the bank liquidity to actually recapitalise the banks. Firstly, the government of India, through the RBI, might issue the bonds. Banks that are sitting on surplus liquidity, will use their resources to invest in these recapitalization bonds.

With the funds raised by the government through the issue of recapitalization bonds, the government could infuse capital into the stressed banks. This way, the surplus liquidity of the banks will be used more effectively and in the process the banks will also be better capitalised and now become capable of expanding their asset books as well as negotiating with stressed clients for haircuts.

Déjà vu – Recapping recap bonds

In India in the early 1990s, the government issued several tranches of special non-marketable securities called recap bonds to PSU banks and banks subscribed to it in the normal course of their business. The cash thus raised was used by the government to infuse fresh equity into beleaguered banks.

In China, the government started the process of restructuring of its banks with the issue of RMB 270 billion in Special Government Bonds in August 1998. The banks could buy the bonds after the Chinese government reduced statutory reserve requirement from 13 to 8 percent. The government then injected all the bond proceeds in their four major banks thereby virtually doubling their capital base.

What is the likely path now?

From hereon in, the government is likely to incentivise the efficient, punish the inefficient and create larger size banking entities to avoid a repeat of the current problems. So pick your bets wisely.

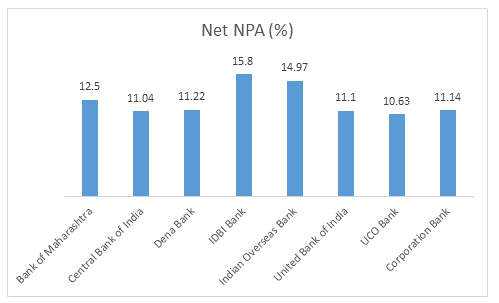

As the exhibit suggests, several PSU banks have net NPA in excess of 10 percent and Allahabad Bank and Oriental Bank of Commerce have reported NPAs that are close to this level. So identify the sick.

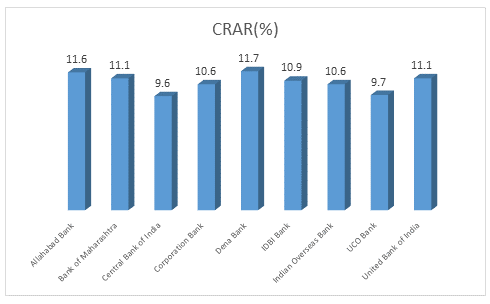

In terms of capital buffer, while none have reportedly breached the level of 9 percent thanks to the small doses of life-saving capital injected by the government, they have just about enough capital to stay afloat.

In fact, if we look at the profitability parameters, (ROA in excess of 0.25 percent), for FY17, only three entities - Indian Bank, State Bank of India (standalone) and Vijaya Bank were above the threshold limit.

Our analysis of slightly longer term data suggests that Central Bank of India, Indian Overseas Bank and United Bank of India have breached the profitability threshold for the past four years i.e. from FY14 to FY17. Banks like Dena Bank and Oriental Bank of Commerce have breached the threshold for the past three years from FY15 onwards.

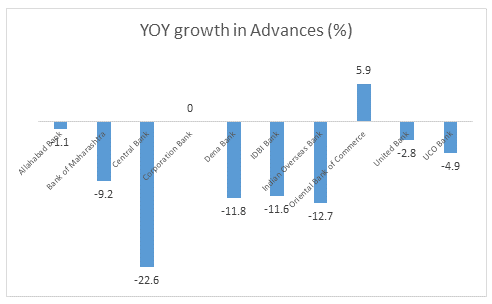

If we look at these ten public sector banks and analyse their impact on the systemic credit growth, the result speaks volumes.

The aggregate assets of these ten entities at Rs 23,80,218 crore is much less than the standalone asset book of State Bank of India. The aggregate advances of these entities is close to Rs 12,75,620 crore – 16 percent of the total bank credit. However, their share in the system’s gross NPA and net NPA is disproportionately higher at 31 percent and 33 percent, respectively.

These entities weighed down by asset quality woes are increasingly losing their relevance in incremental business. If we look at the share of these ten banks in the incremental share of system credit, the figure is negative, suggesting that they are vacating the market to the more savvy competitors.

In the market share game, the list is clearly dominated by SBI, who has, in fact, improved its market share in FY17 over FY16. Other entities who appears to have seen a slight improvement in market share includes Andhra Bank, Bank of Baroda, Bank of India, Canara Bank, Union Bank and Vijaya Bank. These entities, along with Indian Bank (on account of a better performance) and Punjab National Bank (because of the size of the balance sheet) are likely to be the long-term survivors. For the rest, a merger with stronger entities appear to be the logical next step.

In the medium-term while resolution of NPL will gather momentum, banks will likely adhere to greater provision requirements of the RBI (hence profitability may not look up) and compete a little more aggressively in the credit market (hence, expect pressure on margin to get aggravated). In the short to medium term yields might firm up, but in the absence of credit demand from private players, it’s unlikely to impact overall investment.

Finally, with government taking several other initiatives to revive investment, get ready to invest in larger consolidated PSU banking entities that will receive the larger share of capital from the exercise and are likely to play a more meaningful role in the next upcycle. Investors have got to stick to the big boys in the Street.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.