which will give a big boost to digital economy. It is proposed to introduce Digital Rupee based on blockchain and other technologies, and will be issue by the Reserve Bank of India starting this year. (Image: Shutterstock)")

In a little more than a year, discussions on central bank digital currencies (CBDCs) have moved from the fringe to the mainstream. In India, legal enablers for a digital currency have been put in place via the Finance Bill, 2022. All eyes are now on the Reserve Bank of India.

What will the RBI's CBDC look like?

The Finance Bill lays down the likely framework. It proposes that the CBDC "should also be regarded as bank notes". As such, the CBDC ought to be what the name suggests: a currency in all aspects except form.

The proposed change should put to bed certain other questions. Currency notes don't offer interest, so there is no reason for the RBI's CBDC to do so. There are counterviews, most visibly from Sweden's central bank, Sveriges Riksbank, which argued that a non-interest paying CBDC would effectively place a zero lower bound on all interest rates in the economy and thereby limit monetary policy.

For India, positive rates may be a more pertinent territory but if the RBI's views are anything to go by, its CBDC will not carry any interest.

"Basically, digital currency is like a physical rupee only. There is no difference between these two," RBI deputy governor T Rabi Sankar said at the post-monetary policy media briefing on February 10.

The absence of an interest rate should ease fears of CBDCs competing with bank deposits, a balance that central banks don't wish to upend.

| KEY DESIGN FEATURES | |||

| COUNTRY | INTEREST ON CBDC | QUANTITATIVE CURBS | ANONYMITY |

| The Bahamas | No | Yes | For lower tier |

| Canada | Undecided | Undecided | Undecided |

| China | No | Yes | For lower tier |

| Eastern Caribbean Currency Union | No | Yes | For lower tier |

| Sweden | Undecided | Exploring | Undecided |

| Uruguay | No | Yes | Yes, but traceable |

Measures to ensure stability include the CBDC not offering any rate of interest and a cap on the quantity of digital currency that can be held, especially by those who opt for a lower-threshold CBDC wallet that offers the most anonymity.

Also Read: Budget 2022 | Explained: What is Digital Rupee, when will it come and how’s it different from private cryptocurrencies? 10 critical questions answered

Which rupee is which?

There has been confusion about the operational aspects of a CBDC. How would one differentiate between a normal rupee in a bank account that can be used to complete a transaction via internet banking or Unified Payments Interface and a digital rupee or CBDC?

One can turn to The Bahamas for some clarity.

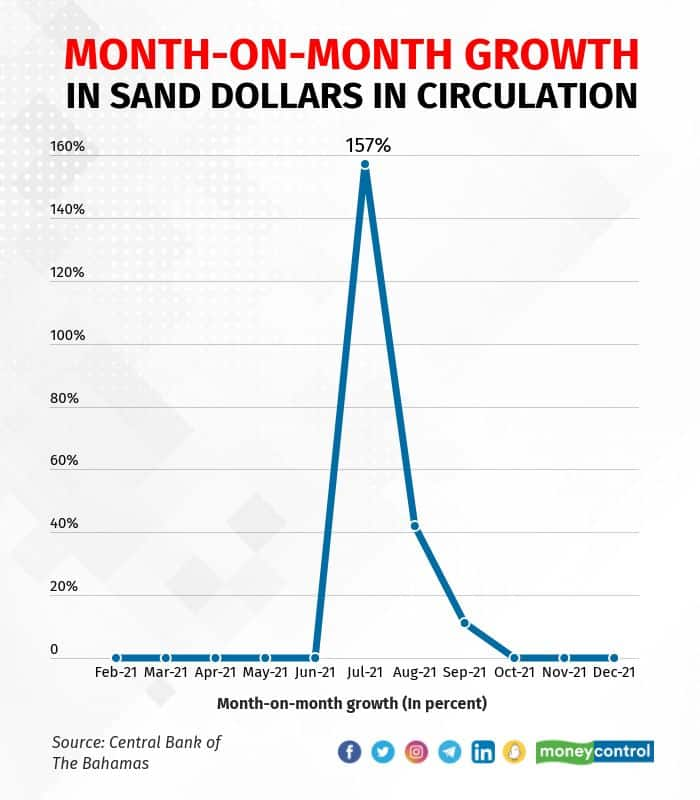

The Central Bank of The Bahamas launched its CBDC, the Sand Dollar, in October 2020. Sand Dollars are held in secured digital wallets, or e-wallets, and can be accessed through a mobile app or physical payment card. Authorised agents enroll users via their proprietary applications.

Users must decide their level of CBDC engagement. The basic e-wallet tier has a holding limit of $500, with a monthly transaction limit of $1,500. Operating under this tier doesn't require the user to furnish any government identity proof. However, it means tier-I e-wallets can't be linked to bank accounts.

Tier-II e-wallets can be linked to bank accounts. They have a far higher holding limit of $8,000 and a monthly transaction limit of $10,000. These facilities require a government issued identity proof for enrolment.

There is a distinction between Bahamian dollars held in a bank account and Sand Dollars in the e-wallet. But they can be moved from one to the other, provided users are willing to give up anonymity and enrol under the higher tier.

If digital and physical currencies are fungible, they should be treated equally on the RBI's balance sheet, with the former also likely to fall under the 'notes issued' head on the liabilities side and backed in full by one financial asset or the other, be it foreign securities or gold.

Retail failure?

The retail frenzy around private cryptocurrencies has been one reason for the speed with which central banks have worked on their CBDCs. However, a CBDC can't be a direct replacement for a private cryptocurrency because of the different purposes they would serve. With no fluctuations in the value of CBDCs, there would be no demand for them as an investment for people to make a quick buck.

More importantly, CBDCs would compete with other modes of payment that have proliferated in the past few years: mobile wallets, UPI, and Immediate Payment Service (IMPS), among others.

Throw in the preference for cash when it comes to small-value transactions and there seems to be no real reason for a non-interest bearing CBDC to gain widespread public acceptance.

The experience in Nigeria, which got its own CBDC, the eNaira, in late 2021, seemingly confirms this view.

"The eNaira has basically been a flop," Alexander Onukwue, Quartz's West Africa correspondent, told Moneycontrol. "Nobody talks about it, nobody talks about using it because it doesn't seem clear what it is supposed to do differently than the normal naira."

The Bahamas' Sand Dollar has perhaps fared better, with the IMF saying there were about 20,000 active e-wallets. With The Bahamas population of just under 400,000, a 5 percent adoption rate is not too shabby.

In value terms, however, the numbers are microscopic. There were $303,785 worth of Sand Dollars in circulation as of December 31, amounting to 0.06 percent of the value of notes in circulation.

Cross-border transactions

Where CBDCs can make a real splash is in cross-border transactions.

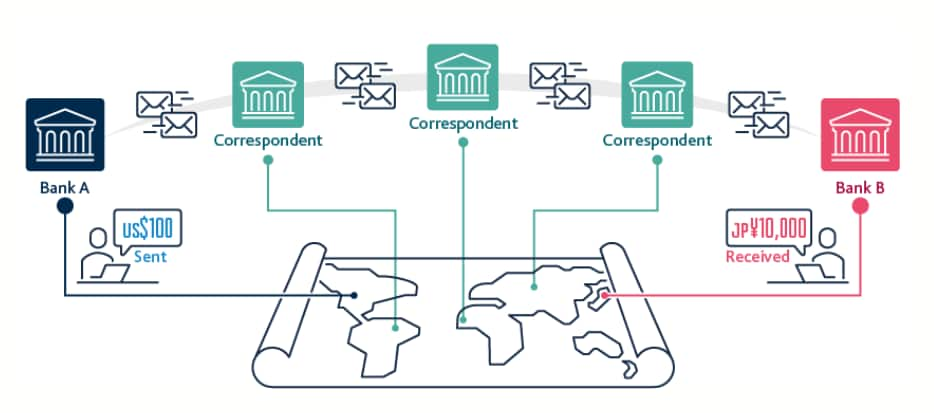

According to EY, cross-border payments are expected to hit $156 trillion in 2022, with business-to-business payments accounting for almost 97 percent of them. These payments are expensive and can take several days to settle.

According to this Bank of England chart, which depicts an international payment involving a not-so-common currency pair, the less common the currencies involved, the greater will be the number of correspondent banks needed to complete the payment. At each stage, there will be fees charged and operational delays, including something as simple as normal business hours.

How would a CBDC solve this? Enter Project Dunbar.

The Bank for International Settlements' Project Dunbar brought together the central banks of Australia, Malaysia, Singapore and South Africa to test a multi-CBDC platform for settling international transactions.

Commercial banks would be able to use the various CBDCs issued to pay each other directly in CBDCs of different currencies. This would make cross-border transactions faster and cheaper as it would do away with the need for intermediaries like correspondent banks.

Of course, it would be quite impossible for all CBDCs to be settled on a single platform. But as the Monetary Authority of Singapore observed in April 2021, such a model would still be beneficial for certain regions.

Project Dunbar is not the only experiment being conducted to test the applicability of CBDCs for international transactions. Others such as Project Jura have been successfully completed with encouraging results.

Closer to India, the Asian Development Bank has set out to connect the central banks of the ASEAN+3 nations—Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines, Singapore, Thailand, Vietnam, Japan, China, and South Korea—via blockchain technology to make their cross-border securities transactions faster and more secure.

While the implications of CBDCs for areas such as monetary policy may not be entirely clear at the moment, it may be that the need to quash the get-rich-quick temptation of private cryptocurrencies could pave the way for a more efficient global payments system.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

| 1W returns-10.43% |

| 1W returns-10.64% |

| 1W returns-11.35% |

| 1W returns-11.73% |

| 1W returns-12.78% |

| 1W returns-13.33% |

| 1W returns-13.57% |

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.