Ishita Sengupta

The most sought-after employees are the ones that are globally mobile. Till a few years ago, ‘brain-drain’ was one of India’s greatest losses in terms of collective manpower strength. The tide is thankfully turning and nowadays it is common to see many Indians who had been working outside India for several years returning home. There are many aspects to be taken care of while relocating to India, such as housing, children’s schooling and bank accounts. While being globally mobile gets you the right career opportunities, there are some important tax considerations to be cognisant of when you return to India. This article provides an overview of the things you need to bear in mind before making the move back.

Residential status

Taxability is determined based on an individual’s residential status for the given financial year (FY). As per the Indian Income-tax Act, 1961 (the Act), if an individual qualifies as an Ordinary Resident (ROR) in India, global income is taxable in India. For a Non-Resident (NR) or Not Ordinary Resident (NOR), incomes earned or received in India are taxable. Among the various scenarios of residency, as a thumb rule, if your aggregate stay in India is for less than 60 days in the returning FY, you will qualify as an NR in India. In all other cases, you should seek expert advice on your correct residential status. Residency is determined by your physical stay, both in the current FY as well as in the last 10 FYs. Hence, as a starting point, you should carefully evaluate your likely residency in India based on the above. Things can go horribly wrong if you have assumed that you will be considered an NR and hence not be taxed on your income outside India.

Salary income

Salary earned/accrued in India is taxable, regardless of your residential status. If you qualify as an ROR, your overseas salary from any prior employment during a part of the FY could also become taxable in India. In such a situation, you can explore relief available based under the Double Taxation Avoidance Agreement (tax treaty) with that country.

Trailing liabilities

Trailing liabilities are deferred incomes arising at a later point in time but pertaining to the erstwhile services rendered in a country. For RORs, overseas trailing income can be subject to Indian taxes and Foreign Tax Credit (FTC) may be explored in case of double taxation. Deferred bonus, tax equalisation settlements or the exercise of stock options in various tranches are some examples of trailing liabilities for a returning NRI.

Social security receipts

When you have rendered service in an overseas location, you/your employer would have made social security contributions. In the event that you are eligible to withdraw such contributions on returning to India, taxability on such receipts would need to be evaluated based on your residency, place of receipt, social security plan and tax treaty.

Stock options

If you were provided with stock options overseas, their taxability in India during the FY will depend on your residential status in India in the year of exercise, as well as the vesting schedule of such stock options specified in the plan. If you hold stock option grants that are still valid for exercise, it is strongly recommended that you carefully evaluate the possible tax consequences in India after your return.Capital gains

Sale of overseas investments, including company stock underlying your stock options, would trigger capital gains taxes in India if you are an ROR in such a year. Typically, as long as you are an NR or NOR, sale of overseas shares will not trigger capital gains taxes in India if the sale proceeds are also received outside India. In case of double taxation, relevant treaties need to be evaluated for FTC.

Other income

If you qualify as an ROR, other income such as rental income from a house owned by you overseas, and other overseas incomes such as dividends and interests could become taxable in India. These would require evaluation based on the Act read with the tax treaties to assess their taxability in India and claiming of FTC in case of double taxation.

Other considerations

Re-designating Indian bank accounts: On your return, you should check with your bankers about re-designating your Indian bank accounts to resident accounts. Also, in case you have provided any instructions to overseas bankers or your employer for direct credit of money to your Indian bank account owing to relocation, such direct receipts are taxable in India on a receipt basis.

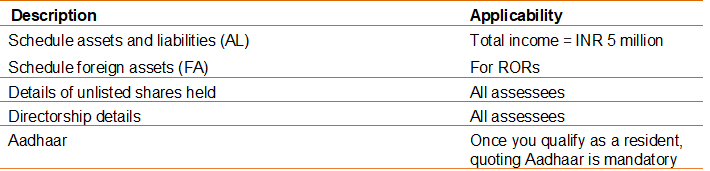

Reporting requirements in India: The Indian tax filing forms also require reporting as below:

As you can see, there are several important aspects to consider with respect to your relocation to India. Accordingly, it is important to plan your move back to India so that your taxes are planned well and you remain compliant.

(The writer is Partner, Personal Tax and Global Mobility, PwC India. Santhosh S, Associate Director, also contributed to this article. Views expressed are personal.)

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.