In August 2022, Rs 12,693 crore came into mutual funds (MF) through systematic investment plans (SIP), the highest-ever monthly SIP inflow in MF history. Clearly, many investors over time have understood the benefits of investing in a staggered manner. But there is another avenue where you can invest systematically. Though returns are modest, the risk is far lower than a mutual fund. It’s called a recurring deposit and you can invest through your bank. Is it worth it?

What is a recurring deposit?

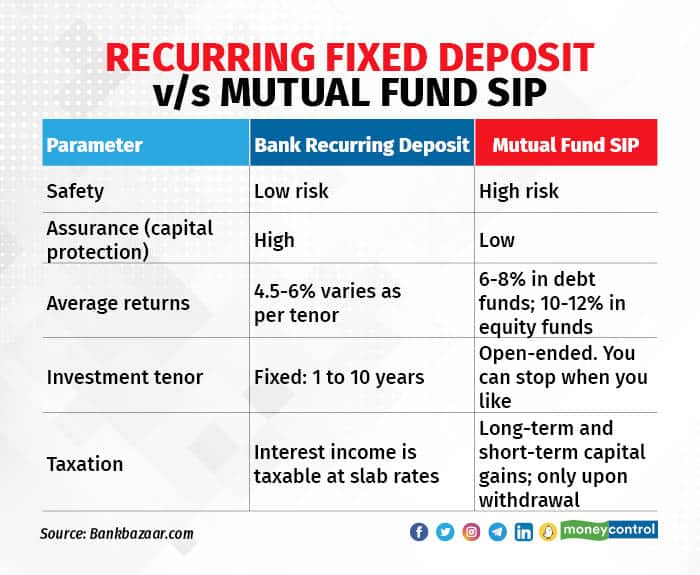

Recurring deposits (RDs) are debt instruments that provide capital guarantee to investors.

Banks offer RDs for tenors of one to 10 years. The instrument allows investors to invest a fixed amount every month and build a corpus for short-term needs. It works just like a mutual fund's SIP. Investing in RDs brings in discipline. The catch, just like an MF SIP, is that you need to have money to invest at the end of every month.

RDs are taxable. Neither the money invested nor the interest earned is exempt, and both are taxed as per the tax slab.

Both RDs and SIPs operate on the principle of regular investments. They allow investors to invest small sums over a period and build a corpus. They also offer a high degree of flexibility.

You can stop your RD and SIP at any time and withdraw your money. However, some banks may charge penalties for premature withdrawals from your RD account. “Both need investors to be consistent with investments as the RD and SIP can lapse and may need to be restarted if the payouts are missed,” says Adhil Shetty, CEO, BankBazaar.com.

Flexibility

MF SIPs come with more flexibility. You can invest in them daily, weekly, fortnightly, monthly, quarterly or annually. Unlike an RD, which is akin to a debt instrument, MFs also allow you to invest in equities, through SIPs. “Investing through SIPs is a better way of participating in equity market because it provides rupee cost averaging, which is the best way to build wealth in the long term especially for investors with regular monthly income,” says Amol Joshi, founder of Plan Rupee Investment Services.

“The SIP amount invested in the equity market makes the right tool to build the long-term corpus. Typically, SIPs work best when you are invested for at least 5 years or more,” says Shetty. Keep in mind though, that the returns from SIP in equity mutual funds are volatile in nature as they are market-linked.

RDs come with lock-in; you cannot withdraw your investments before the tenure ends. This could be 1-10 years.

Also read: Recurring Deposit Rates | These banks offer up to 7.35% interest for 5-year tenor

On the other hand, you can stop or withdraw from your SIPs easily. Only SIPs in equity-linked saving schemes (ELSS) come with a lock-in of three years. In an ELSS scheme, each SIP gets locked in for three years. Simply put, your redemption also gets staggered, just like your monthly investments. “Non-ELSS funds usually don’t have a lock-in but some may have an exit load if you decided to exit the fund in less than a year,” says Shetty.

“SIPs do not provide capital protection, and market cyclicity may erode your savings in the short term before building it again, as we have seen during the Covid years,” he adds.

RDs are taxable. Neither the money invested nor the interest earned is exempt, and both are taxed as per the tax slab. The interest generated on RDs tends to be below inflation. After tax, this return can be negative. So it may not be the right tool for long-term investments.

Also read | MC30: The best mutual funds to invest in

Are guaranteed returns better?

Typically, we like guaranteed returns. But they look good if you do not wish to take any risk or your risk tolerance is nil to negligible. In this case, your returns expectation should also be low. “RDs offer capital protection, which can be important while saving for the short term,” says Shetty.

“The Deposit Insurance and Credit Guarantee Corporation, a subsidiary of the central bank, guarantees investments in RDs of up to Rs 5 lakh,” says Joshi. There is no such assurance while investing in MFs through SIP.

On the other hand, returns from SIPs are linked to the market. When markets go up, your MF scheme makes more money, and vice-versa. Over the long period of time, equity funds tend to outperform debt funds.

Who should invest in RDs?

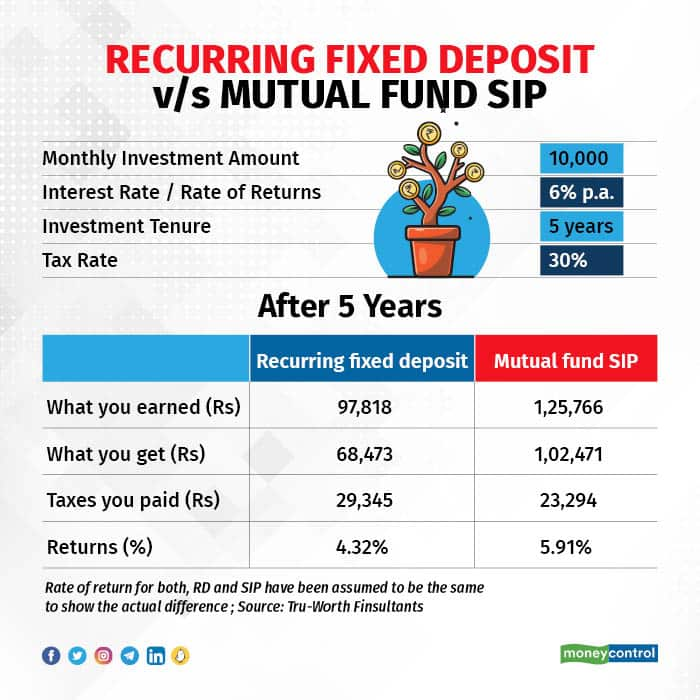

Although RDs give you guaranteed returns, they aren’t tax-friendly. Back-of-the-envelope calculations show that Rs 10,000 invested monthly at the rate of 6 percent per annum for a period of five years earns a little over Rs 97,000 in an RD as opposed to around Rs 1.26 lakh in a debt fund. However, interest earned in an RD is taxed at your income-tax rate; 30 percent for the highest tax slab. Debt funds, on the other hand, are eligible for capital gains tax; long-term capital gains come with indexation if you hold your units for three years or more.

Also, besides the tax on interest income in RD, banks deduct TDS (Tax Deducted at Source). This TDS, says Tivesh Shah, CEO of Tru-Worth Finsultants, comes out of your interest accrued. This means, that your accumulated interest goes down to the extent the TDS is deducted. This affects your compounding.

So, which one is better? RD or SIP? Investors who are not very familiar with the financial product landscape and have a conservative outlook should prefer investing in RDs. “Even people just starting with the first job can prefer part of savings in RDs to build contingency fund and achieve short-term goals,” says Joshi. Investors who are much ahead on the information curve regarding financial products availability and risks involved should prefer investing in mutual funds through SIP, he adds.

“An investor should first decide the time horizon for investment, evaluate his risk profile and then select the investment instrument,” says Raj Khosla, founder of MyMoneyMantra.

What should investors do?

RDs are for a fixed tenor and interest income is taxable. However, they are debt instruments that provide capital guarantee. “This makes them perfect for building corpuses required in the near term – typically for accumulating funds you would need in the next year or so,” says Shetty.

SIPs, on the other hand, can be for as long as you wish to continue them linked with the goals. “Those looking for investment over the longer time horizon, i.e. more than five years, should prefer investing in mutual funds through SIP,” says Khosla.

Take your pick.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.