Prasenjit Dey, a Vadodara-based businessman selling mobile phones, invested Rs 10 lakh in May 2023 in the flexi scheme operated by MobiKwik Xtra and handled by Lendbox, a regulated non-banking financial company (NBFC)-P2P (peer-to-peer) lending platform operating under Reserve Bank of India (RBI) rules.

Vadodara-based chartered accountant Deepak Shah too invested in the same Lendbox P2P scheme via MobiKwik Xtra, putting in Rs 40 lakh in June 2023.

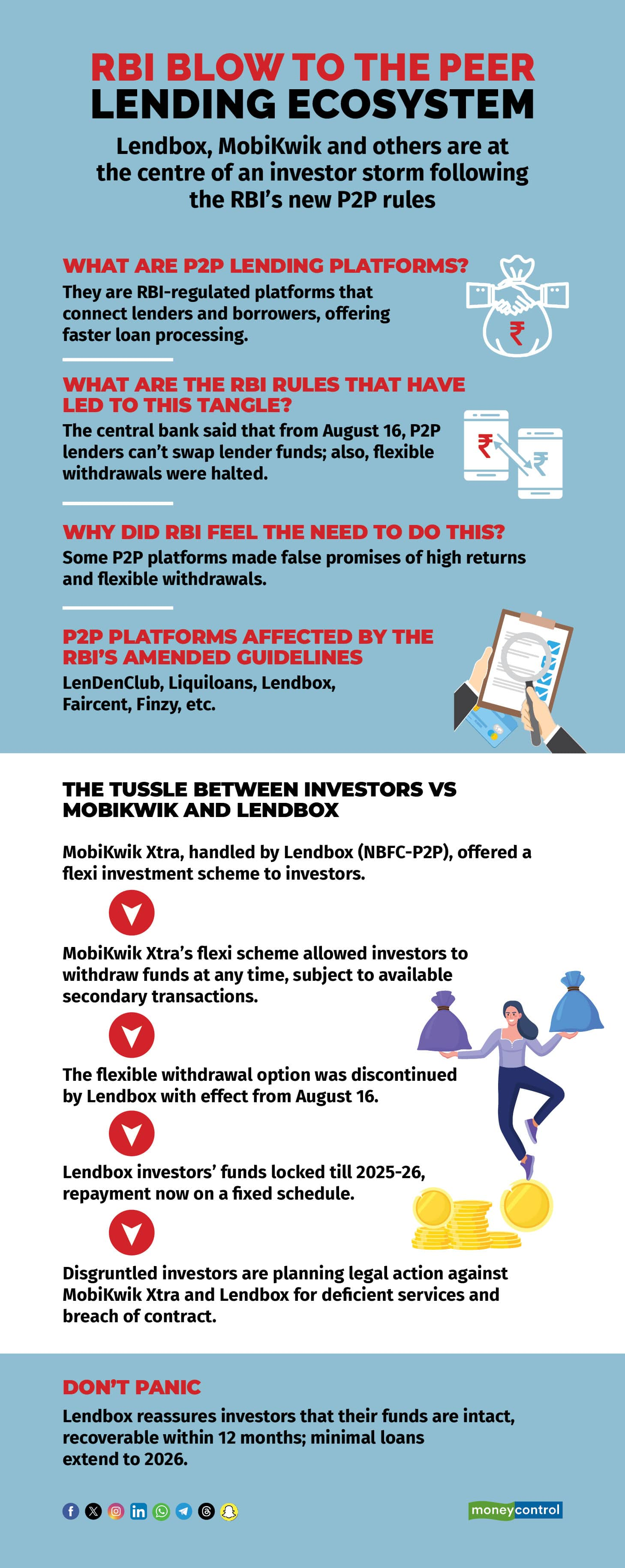

The scheme offered investors (in effect, the eventual lenders as their money was used to advance the loans offered) the flexibility of withdrawing their funds at any time, contingent on secondary transactions being available as per the agreed terms.

RBI's new rules freeze investments

The RBI shook up the P2P lending landscape on August 16 with revised guidelines. As a result, popular features like Lendbox's flexible withdrawal option were suddenly discontinued, effective immediately, to comply with the new regulations.

Sumanta Mandal, founder of TechnoFino, a platform that reviews debit and credit cards, pointed out that many P2P lending platforms were misleading investors with promises of a 12 percent fixed income opportunity and flexible withdrawal options. This led to the RBI stepping in and establishing new norms for these companies and their customers.

Following the guideline changes, investors like Dey can now withdraw funds only as borrowers repay, on a monthly basis—that is, from the 12th of each month—along with applicable interest. Consequently, Dey's Rs 10 lakh investment in Lendbox is now locked in until May 2026, as per the repayment schedule provided by the company, effectively ending the flexibility he initially enjoyed.

Similar to Dey's situation, Shah's funds are now tied up until June 2026, as per the repayment schedule outlined by the company, in effect freezing his investment for nearly three years from when he invested.

According to Parijat Garg, a digital lending consultant, the revised guidelines will likely impact existing lender-borrower relationships starting from the effective date. He noted that many loans are for 12-24 months, implying that the changes will affect ongoing contracts and not just new investments.

Also read | RBI’s new rules for P2P platforms: A net positive for lenders, borrowers, say experts

Locked funds spark legal action: Investors seek relief

Dey and Shah are among numerous investors who have found their funds locked into Lendbox's P2P scheme via MobiKwik Xtra, with repayment now tied to a fixed schedule. Having invested before August 16, 2024, when flexible withdrawals were permitted, these investors are now seeking legal recourse. Several investors have decided to file a case against One Mobikwik Systems Limited and Lendbox's parent company Transactree Technologies Pvt Ltd, seeking resolution and recovery of their invested amounts immediately.

Moneycontrol has obtained and reviewed the legal notice drafted on behalf of these disgruntled investors, alleging deficiency of services and breach of contract against One Mobikwik Systems and Transactree Technologies. The notice invokes the Consumer Protection Act, 2019, and other relevant laws. To understand these litigations, Moneycontrol has also reached out to the companies involved to understand their stance on the allegations.

The investors' legal notice raises several critical issues. Here are the main points of contention and stance from the companies.

Violation of contractual terms

Dey claims that when he invested in 2023, the terms mentioned flexible fund withdrawals without any lock-in period. He strongly believes that changing this agreement to a lock-in plan in September 2024 without his consent is a blatant breach of contract.

A MobiKwik spokesperson said, “Following the RBI's amendment to the P2P-NBFC master directions on August 16, 2024, Lendbox was required to restructure the product, resulting in the stoppage of 'anytime withdrawals' among other changes. Specifically, the updated master directions mandated that loan repayments to lenders could only be made from the actual repayments received from the mapped borrowers.” The changes made in September 2024 were directly in response to the RBI's new regulatory guidelines, which were implemented immediately without exception, he added.

Bhuvan Rustagi, co-founder and COO of Lendbox, has revealed that an association of P2P platforms has sought clarification from the RBI on whether recent amendments apply to existing investors. Specifically, they're asking if grandfathering of existing portfolios is permitted, and they're awaiting a response. If the RBI gives the green light, allowing grandfathering, Lendbox will permit liquidity options for investments made before August 16, provided secondary sales are available.

This move would provide relief to investors who had invested under the terms as previously existed, which mentioned flexible fund withdrawals without any lock-in period.

Fake borrowers' lists and non-disclosures

Dey has raised concerns about Lendbox's lending practices, alleging that loans have been disbursed to potentially fake or fraudulent borrowers without proper disclosure to investors. Specifically, he pointed out that borrower names are not fully disclosed, instead only showing initials, which raises suspicions. Furthermore, some lending amounts are unusually small, from single to double digits, leading Dey to question their legitimacy. These claims suggest a lack of transparency and potentially compromised due diligence in Lendbox's lending processes.

“We categorically deny that loans were disbursed to fraudulent borrowers. The decision to disclose only the borrowers’ initials is to protect their identity, as the amended master directions mandate that disclosure of personal information of a borrower is subject to the consent of the borrowers,” the MobiKwik spokesperson said.

According to Rustagi, Lendbox employed a diversification strategy for investments prior to August 16 to mitigate risk by fragmenting investments across multiple borrowers. "By spreading investments thinly, we minimised exposure to potential defaults," he explained. This approach ensured that, even if a small percentage of loans went into default, investors' returns would remain largely unaffected. He emphasised that the total amount disbursed to borrowers was precisely matched to investors' contributions, further safeguarding their interests.

Also read | Lending on P2P platforms: A risky proposition; not an investment

Failure of payment schedule

Investors have expressed concerns about Lendbox's handling of their investment, citing gross negligence and breach of trust because of the company's failure to meet the payments schedule deadline of September 30, 2024. Moreover, the lack of communication regarding this failure has only exacerbated the issue. Investors also highlighted that Lendbox's inability to release their funds in a timely manner, or without interest, and providing less than the minimum promised amount constitute an unfair trade practice that is completely unacceptable.

Rustagi said, “All investors who were eligible for the September 30 payout have already been notified of the repayments available for withdrawal. It is important to note that payouts to investors are directly dependent on the repayment of loan amounts received from the borrowers mapped to each investor’s account.”

Also read | Millennials comprise largest segment of active users on P2P platforms

Don’t panic

Rustagi sought to reassure investors, stating that their funds are still intact and merely subject to a changed withdrawal dynamic. "There's no need for panic; the money hasn't vanished," he underlined. Instead, the instant withdrawal option is no longer available. Rustagi pointed out that borrowers are continuing to repay their loans, with most lenders already receiving over 30 percent of their investment back with interest in just three payouts since August 16. He is optimistic that, based on repayment schedules and loan tenures, the majority of investors will recover their entire investment within the next 12 months. Only a small fraction of loans will extend into 2026, as per the predetermined repayment schedule, according to him.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.