In an era where digital payments dominate everyday life—from buying groceries via UPI to shopping online with credit cards—transaction failures can be frustrating and financially disruptive. These glitches, often stemming from technical or authorization issues, affect millions annually.

Common causes of digital transaction failures

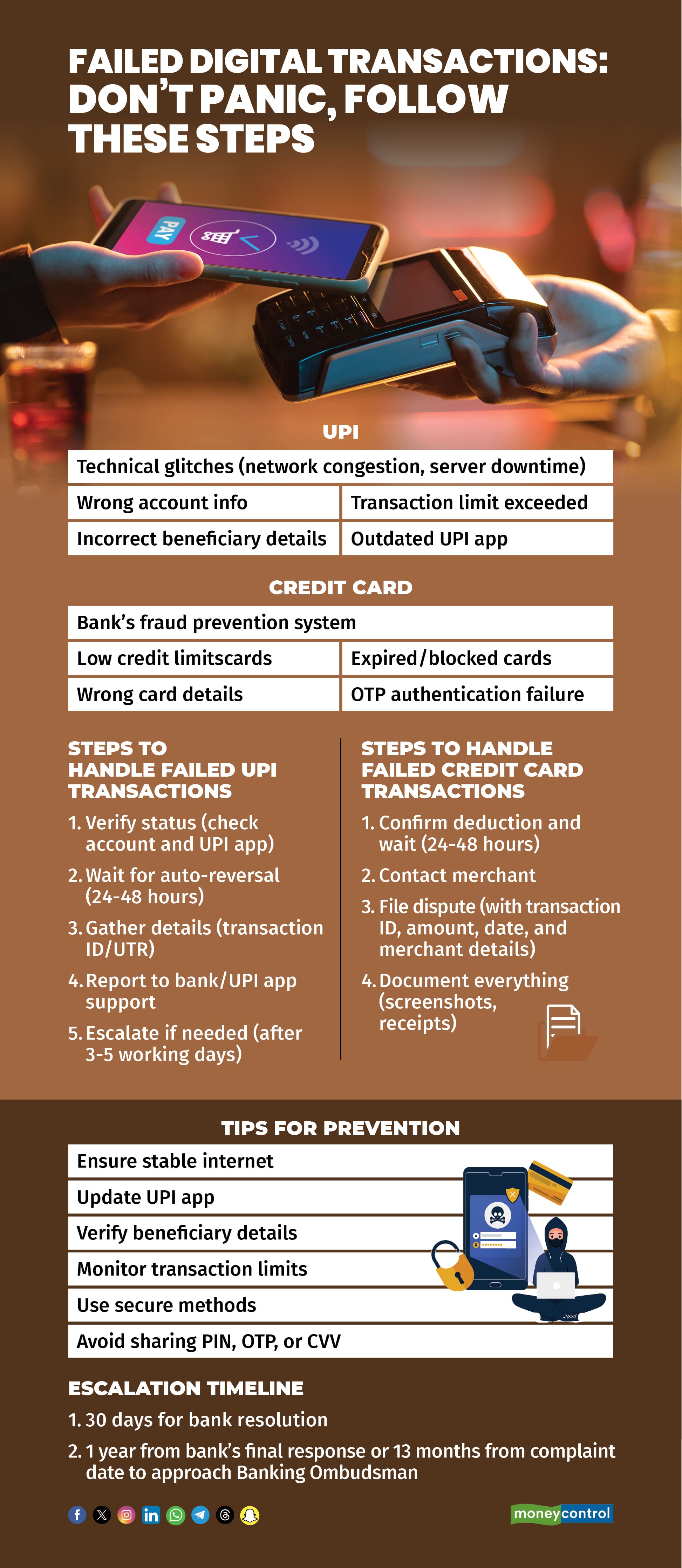

Understanding the root causes is the first step toward prevention and resolution. For UPI transactions, failures often arise from ecosystem vulnerabilities. "Technical glitches like network congestion, bank server downtime during peak hours, and maintenance of NPCI and banks are some of the reasons for UPI transactions failing," says Advocate Ashwini Kumar, Founder of My Legal Expert. Other factors include wrong account information, and transaction limit exceeded.

Sarika Shetty, Co-founder and CEO of RentenPe, a rent credit score platform, said, "Failures can also happen if beneficiary details are incorrect or if the UPI app being used is outdated or crashes. In some cases, double payment requests triggered by repeated taps can also lead to transaction interruptions."

Credit card failures follow similar patterns but with unique triggers. Some of the common reasons are low credit limits, expired or blocked cards, wrong card details, or the bank’s fraud prevention system going off. Then, card not activated for online or international transactions and OTP authentication failure are frequent culprits.

Ramakrishnan Ramamurthy, Chief Delivery and Operations Officer, India, Worldline, a secured payment and transactions solutions firm said, "Authorisation-related failures occur when the issuing bank declines a transaction because of reasons such as insufficient balance, expired or hotlisted cards, or incorrect authentication inputs like wrong OTPs or CVV."

Step-by-Step guide to handling failed UPI transactions

When a UPI payment fails, act methodically to avoid escalation.

Verify the status immediately: Check your bank account and UPI app for deductions or pending status. "Wait for a few minutes, sometimes it takes 1–2 hours to reflect in the bank," advises Shetty.

Monitor for auto-reversal: Many issues resolve themselves. Consumers are advised to check their bank accounts to see if the money has been deducted and then wait for 24-48 hours, since usually the reversals are done automatically in this time frame.

Gather details and report: Note the transaction ID or UTR. Contact your bank or UPI app customer support with the transaction details. “If unresolved, file a complaint through the UPI app and also inform the bank of the transaction ID," said Kumar.

Escalate if needed: For persistent problems, reach out to higher authorities. Shetty said, "If unresolved after 3–5 working days, escalate to the bank’s grievance cell."

“The payment ecosystem is working together to improve infrastructure, reduce technical issues, and enhance monitoring systems to make digital payments smoother,” said Ramamurthy.

Handling failed credit card transactions

Credit card failures, especially when amounts are deducted, require prompt merchant and bank involvement.

Confirm deduction and wait briefly: Check if the amount was deducted from your account and wait for 24–48 hours for pending transactions to reverse.

Contact the merchant first: The first step consumers should take when dealing with transactions that were not successful but resulted in debited amounts is to contact the merchant.

File a dispute: If unresolved, contact your bank’s customer care with the transaction ID, amount, date, and merchant details. If that does not work out, then the next option is to file a dispute or ask for a chargeback through the card issuer, presenting the evidence of the transaction and communication."

Document everything: Keep evidence of failed transactions (screenshots and receipts), to strengthen your case.

Also read | Moving from group health to individual cover without losing benefits

Tips for preventing future failures

Proactive habits can boost success rates. For UPI, users must ensure uninterrupted internet access, have the latest UPI apps, check beneficiary details with extreme accuracy, and keep an eye on your daily transaction limits.

Shetty said, "Avoid repeated clicks; wait for the app to respond and enable app notifications to get instant transaction updates."

"Risk or fraud-related rejections also contribute to failed transactions when the system flags unusual spending patterns for additional verification," Ramamurthy said.

General advice includes using secure methods, avoid sharing UPI PIN, OTP, or card CVV with anyone.

When to escalate to the banking ombudsman

If bank efforts fall short, know your escalation timeline. It is suggested that consumers give a maximum of 30 days for their respective banks to fix the complaints. "In case the complaints are not settled, the customers have the option to escalate the issue to the Banking Ombudsman within a year from the date of the bank's final response or within 13 months from the date of the complaint, whichever period is shorter," said Kumar.

Also read | Infosys buyback: Should you participate or skip it this time?

Final consumer empowerment tips

Empower yourself with knowledge. Customers are encouraged to keep transaction evidence and to inform the bank about any questionable transactions at once. "Being aware of RBI rules, dispute rights, and consumer protection rights enables users to master digital payment failures with assurance," said Kumar.

Regularly monitor your bank statements for discrepancies and for repeated failures, consider alternate payment methods (net banking, wallet apps, or a different card)."

By following this guide, consumers can turn transaction failures into manageable hurdles, ensuring smoother digital financial experiences.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.