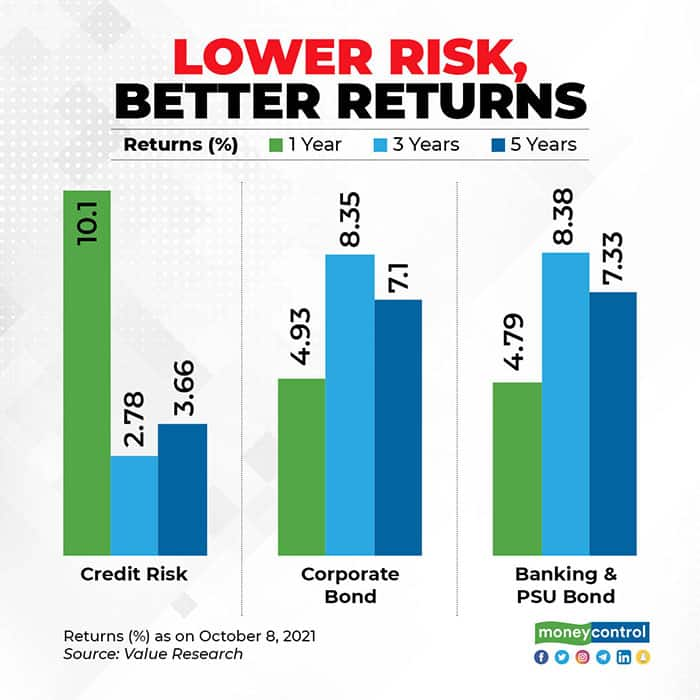

If investors had not sold off their debt funds immediately after the Franklin Templeton crisis last year, they would have benefited. What probably looked like the worst phase for credit risk funds turned out to be quite profitable. And smart investors always knew this. Credit risk schemes were the only debt MF category that gave double-digit returns over the past year. These schemes gave 10.25 percent on an average over the past one year, as per Value Research data. Does this revival mean that you must invest in credit risk funds right away?

Lower quality bonds got support

The performance of credit risk funds needs to be put in perspective. After COVID-19 spread, equity and debt markets around the world fell. Debt securities also became illiquid, especially the low-rated bonds (AA and lower).

Franklin Templeton India mutual fund was caught with some of these bonds. Investors started withdrawing from these funds in panic. This led to fund houses selling securities to meet the rush in redemptions. In May 2020, credit risk funds saw net redemptions of Rs 5,173 crore. A fall in their prices led to a rise in their yields; the gap (or spreads) between yields of AA-rated and AAA-rated bonds rose to as much as 200 basis points. One basis point is a hundredth of a percent point.

However, the table turned when the Reserve Bank of India (RBI) supported the economy by reducing interest rates and offering financial support to stressed sectors through various policy measures. That led to yields falling on bonds issued by large corporates with AA ratings. Simultaneously, prices rose.

Is the worst behind us?

The Modified Credit Ratio (MCR) of CARE Ratings improved from 0.92 in H1FY21 to 1.11 in H1 FY22. “Improving credit ratios issued by rating agencies in the recent past talk about the improvement in financial health of formal sector of the economy. Defaults happen when the economy slows down. If the economy continues to grow, then the chance of widespread defaults go down, making well-managed credit risk funds worth considering for allocation,” says Joydeep Sen, Corporate Trainer- Debt.

There is optimism elsewhere, too. The economic scenario is improving and the same is captured by various indicators such as rising demand for vehicles, rising crude oil prices and rising online spends. Nitin Rao, CEO, InCred Wealth says, “Low interest rates and strong growth in demand is a good combination for the companies to do well.”

If the economy continues to do well, then the low-rated corporates see good profitability and they can keep refinancing their existing loans easily. Robust equity markets have also helped some corporates to raise money and there is not much pressure to raise money by issuing bonds.

Rao says he is selective of which AA-rated bonds investors must invest in, “but retail investors must consider some investments in credit risk funds,” he adds. “Improving macroeconomic scenario, credit cycle over a period of time and reasonable spread make credit risks, that focus on AA-rated bonds, attractive,” says Devang Shah, Co-head Fixed Income, Axis Mutual Fund.

A glance at net yields of credit risk funds offers an idea of the expected returns from the scheme, though this is not a sure way to predict the returns. Net yields of credit risk funds should be higher than those of corporate bond funds (those that invest 80 percent of their assets in AA+ rated and above assets), to justify the additional risks that credit risk schemes come with.

Sen says, “Consider allocating money to well-managed credit risk funds if you are getting decent extra yield compared to that offered by corporate bond funds.”

“Well-diversified credit risk funds focusing on AA-rated bonds with one to two years portfolio duration offer decent spread over AAA rated bond portfolios and also protect you from interest rate risk,” Shah adds.

The dangers of rising interest rates

Experts say that as and when the RBI starts to increase interest rates, credit risk funds with high duration may fall a tad more than short-term debt schemes. If crude oil prices remain high, inflation may persist. That might push RBI to raise interest rates. Some corporates may have to pay more to refinance their debts. Rising yields would result in investors getting exposed to interest rate risk. As of now, there are no such signs and the economy appears to be in structural uptrend. But investors cannot ignore that risk altogether. “Avoid investing in a credit risk fund with a duration of more than three years,” says Vikram Dalal, Founder and Managing Director, Synergee Capital Services.

Dwijendra Srivastava, Chief Investment Officer-Debt, Sundaram Mutual Fund says, “Although credit funds look good given the positive real returns they have managed, they are not high enough to make them a compelling investment option. Do not have them for your core strategy.” Like Dalal, he too recommends credit funds of lower duration – around 1-1.5 years’ timeframe.

Your investments in credit risk scheme should not, ideally, exceed 20 percent of your overall fixed income portfolio.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.