Nobody saw it coming. Just three days before Franklin Templeton mutual fund shut six of its debt schemes, Santosh Kamath, Chief Investment Officer at Franklin Templeton Fixed Income India and Sanjay Sapre, President, Franklin Templeton-India had a teleconference with a large section of distributors. It was a courtesy call to talk markets in general and Templeton’s debt schemes’ performance. Over the call, both Santosh and Sanjay allayed fears and concerns of many distributors and reassured them that all was well. There was no sign of the coming storm.

The house is India’s ninth largest mutual fund with average assets under management (January-March 2020) of Rs 1.16 trillion.

On April 23, Franklin Templeton announced the closure of its schemes. The combined size of these six schemes was Rs 25,856 crore as on April 22. Looking at its past track record, nobody would have expected that things would come to a stage where the fund house would have had to close six of its debt schemes.

A unique strategy….Until around 2006, Franklin India’s debt schemes’ performances were in line with those of most other fund houses. That year, Santosh joined Templeton and decided to use his own expertise to the hilt. Having started his career in project financing at Shipping Credit and Investment Corporation of India (SCICI), which was a subsidiary of what was then ICICI, Santosh had an early grooming in analysing company balance sheets, a trait that also made him an equity fund manager at SBI Funds Management 1993. Santosh decided to put his knowledge to good use at Templeton.

After the 2009 credit crisis, he refocused many of Templeton’s debt schemes to look at corporate bonds. In 2011, Franklin launched the Templeton India Corporate Bond Opportunities Fund (TCBF), which changed the way the mutual funds industry viewed and invested in corporate bonds. Santosh also rightly realised that the best way to make these funds work is to ensure that investors stayed put in them for a long time. Franklin Templeton imposed exit loads to penalize early withdrawals – 3 to 1 percent for redemptions made between 12 and 30 months.

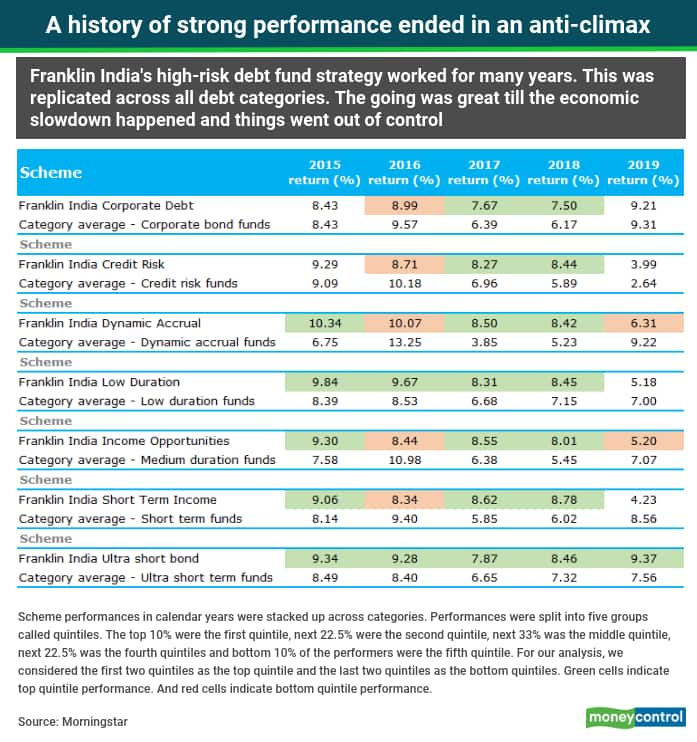

Having tasted success in this fund, Santosh decided to follow a similar credit risk strategy across many other debt fund categories. The strategy worked.

For instance, Franklin India Ultra short bond fund’s performance in each of the calendar years from 2015 to 2019 was in the top quintile. TCBF, which later became Franklin India Credit Risk and was shut down last week, also did well for a number of years and gave high returns.

“Templeton debt schemes also took an early liking to pass-through certificates, which were again innovative instruments designed to earn slightly higher returns than AAA-rated bonds,” says an advisor who did not wish to be named.

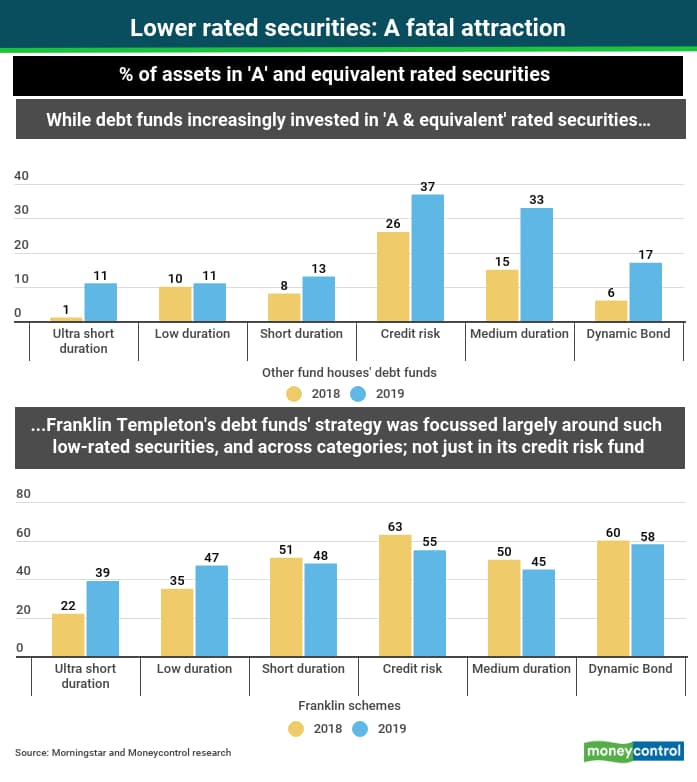

…gone out of controlIt wasn’t as if Santosh didn’t understand interest rates and duration strategies. It was just that he had enormous confidence in credit risk bets. At some point, Franklin Templeton, under his guidance, decided to follow the same strategy across many other funds. Even shorter tenure schemes such as Franklin India Low Duration and Franklin India Ultra Short Bond started to look at corporate bonds. That wasn’t all. A cornerstone of Templeton’s strategy was to invest in bonds that came with low credit ratings. Franklin India Ultra Short Bond fund, a debt scheme meant for 3-6 months’ investment tenure, had nearly 28 percent of its assets in securities with credit rating of ‘A’ and below. Similar schemes from other fund houses had just about 3 percent on an average.

Another of its short-term fund, Franklin India Low Duration fund (a debt scheme meant for 6-12 months’ investment horizon) had invested around 44 percent in such risky assets. Similar schemes of other houses had just 10 percent in securities rated ‘A’ or below.

“If there is a specific credit risk fund, which is meant to take credit risks, then how can any fund manager take credit risks in several other schemes? This was not acceptable to many conscientious advisors, but the strategy went unabated till it came undone after the defaults in some underlying papers in 2019,” says Deepak Chhabria, CEO and Director, Axiom Financial Services.

Chasing yieldsCompetition is tough in debt funds. By and large, debt funds give returns of between six and nine percent with the exception of government securities funds that have been known to deliver more during falling interest rates. But Franklin Templeton’s strategy of investing in corporate bonds of lower-rated companies (Santosh and team always insisted on calling them well-managed and waiting for a re-rating) ensured that its debt funds stayed ahead of competition for many years.

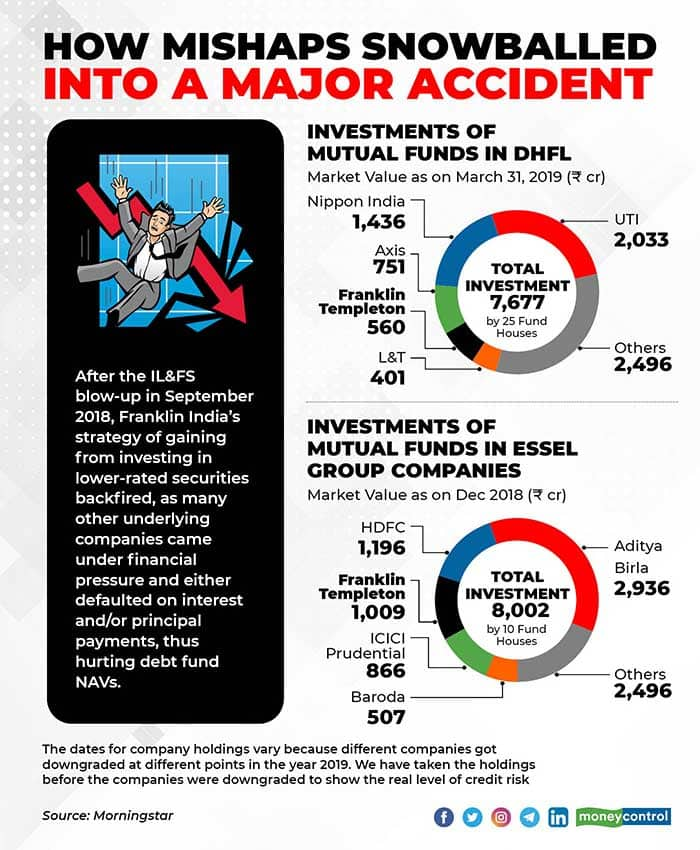

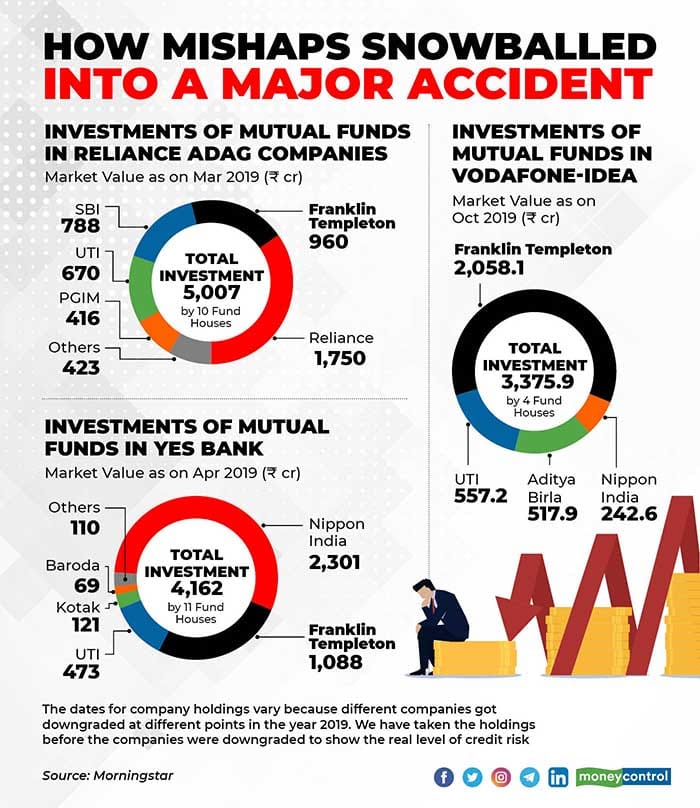

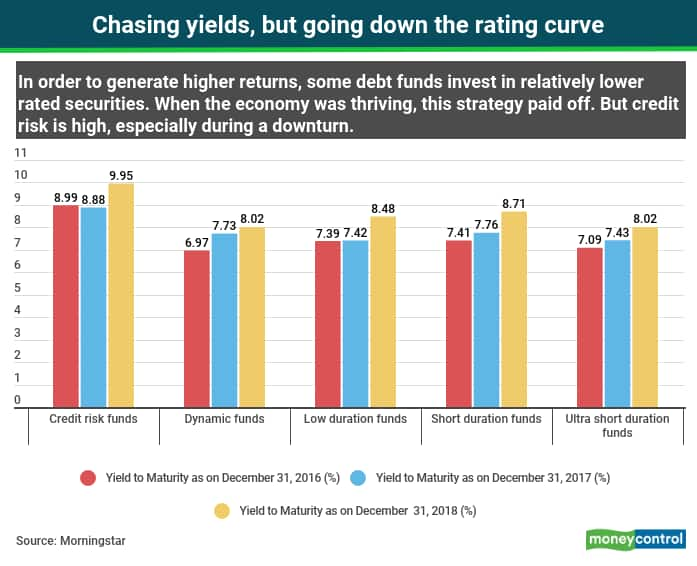

Eventually, other debt funds also smelt blood and started following the credit strategy <See: Chasing yields, but going down the rating curve>. By the end of 2018, Franklin Templeton (and many other debt funds, to be honest) had invested in companies and corporate houses such as Dewan Housing Finance Corporation, Essel Group, Reliance Anil Dhirubhai Ambani group, Yes Bank and Vodafone-Idea.

In fact, some distributors Moneycontrol spoke to point out that Templeton ought to have cleaned up its portfolio in 2016, when the Franklin Templeton Asset Management bought its schemes’ entire holding in Jindal Steel and Power Ltd (JSPL) after a series of downgrades. But Franklin Templeton continued its credit strategy, regardless.

The advisor quoted anonymously above says that his firm stopped putting in incremental money in Templeton’s debt schemes after this episode.

“The credit strategy became a category by itself. This is a popular category known as junk bonds abroad. But here as well, despite the debacle at Franklin Templeton, credit risk category will continue. It’s just that investors should not make this a part of their core portfolio, which is what happened. Just like you allocate a small portion to small caps, in debt funds as well you need to asset allocation,” says Vinod Jain, Principal Adviser, Jain Investment Planner.

Ironically, Franklin Templeton had not invested in the IL&FS group. But the credit crisis that unravelled after the IL&FS debacle reduced the liquidity in the market, which forced many other companies – and many of these were present in Franklin Templeton’s portfolios – to default on their interest and principal payments.

Bad judgement or liquidity crisis?One by one, the cookie crumbled at Templeton. The downgrades of some of its investments led to the segregation of portfolios. For instance, Franklin India Low Duration Fund has two side-pockets. Franklin India Short-Term Plan and Franklin India Credit Risk Fund have three side-pockets each, as per the March-end factsheet.

The onset of the COVID-19 crisis made matters worse. As redemptions grew from many debt funds, Franklin’s inability to sell its bad securities in illiquid markets caused by a massive sell-off in bonds in the month of March meant that the fund house could not gather generate funds to pay off its investors. A closure of schemes was its only choice.

But can the fund get away by blaming the COVID-19 crisis? The capital markets regulator, Securities and Exchange Board of India’s (SEBI’s) rules on portfolio segregation (side-pocketing) say that fund managers as well as the chief investment officers would not be eligible for their bonuses if their portfolios are segregated. That is the price fund managers are made to pay for taking bad decisions.

When Sanjay was asked about this in the April 23 call, he avoided a direct answer and instead said that the priority was to return investors’ money over time. In fact Sanjay’s responses appeared to blame the illiquidity in the debt markets rather than the aggressive credit strategy the fund house had followed in many funds.

Financial advisors and investors will not forget this episode in a hurry.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.