The spread of the COVID-19 pandemic and the resultant lockdown have impacted people across industries. Several salaried and business persons are reeling under cashflow strains, salary cuts and job losses. The government and the central bank have taken steps to ease financial burden by offering moratorium on loans, allowing withdrawal from provident fund and so on.

Banks have also started offering personal loans specifically for tiding over the COVID-19 crisis.

Now, most banks offer a top-up home loan scheme. The interest rates are lower. But should you go for the product? Before taking a top-up loan you must be aware of how it works and its suitability for your needs.

What is a top-up home loan?

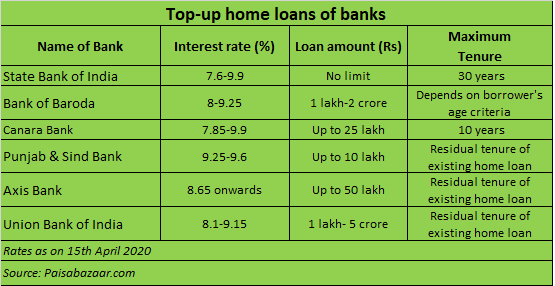

A home loan top-up is an additional loan that you can avail. The maximum loan amount and the tenure available varies from lender to lender. Customers have the flexibility of taking a top-up loan from their existing lenders or from a different lender through balance transfer. The State Bank of India (SBI) is offering top-up home loans at a lower rate compared to other banks. SBI’s top-up home loan interest rate starts from 7.6 per cent a year, while other banks are charge more than 7.85 per cent.

Top-up home loans do not come with any restriction on the end-usage of the amounts. You can use them to fund your children’s education fees, meet your day-to-day financial necessities, renovate your house, invest in your business, etc.

Ratan Chaudhary, Head of Home Loans, Paisabazaar.com says, “The interest rates of most top-up home loans are usually lower than other loan alternatives for the people having the same credit profile. Moreover, top-up home loans come with longer tenures than other loan options.” All these make top-up home loans a good alternative to manage the cash flow disruptions caused due to the COVID-19 pandemic.

Sukanya Kumar, Founder and Director of RetailLending.com points out, “You cannot apply for a top-up home loan scheme during the lockdown period because it requires legal and technical evaluation of the mortgaged property with the lender.” However, there are personal loans that have similar features and interest rates. You can apply online for these loans till June 30.

Who is eligible?

Existing home loan borrowers are eligible for top-up home loans depending on the property's market value, your repayment track record and a healthy credit score. Denny Tomy, Business Head at theloanguru.in says, “You should exhibit a regular repayment history of minimum nine months to one year (varies with financial institutions) to get the benefit of a top-up home loan.” Some lenders may provide top-up loans only against completed residential properties, and not against under-construction ones.

You can get up to 75-80 per cent of the property value as per the prevailing market price. “Due to the impact of COVID-19 on the real estate sector, property prices have reduced across cities. This will have an adverse impact on your borrowing after the evaluation of your property by the lender,” says Tomy.

How do they compare with other loans?

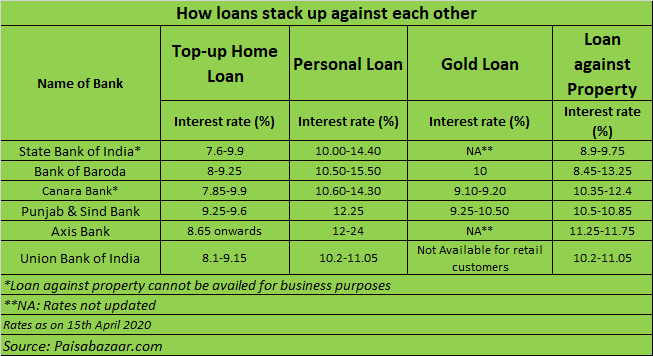

For top-up home loans banks charge interest rates of 0.5-1 percent point more than they do for home loans. “Still, top-up home loans from banks clearly outscore other loan options because they come with lower interest rates compared to personal loans, gold loans and loan against property,” says Kumar. For instance, the top-up home loan from Canara bank starts from 7.85 per cent per annum, whereas the rates for personal loan, gold loan and loan against property the rates are10.6 per cent, 9.10 per cent and 10.35 per cent, respectively. Interest rates are based on the repayment history, credit score, etc. of loan applicant.

The maximum loan tenure for the home loan top-up is higher compared to other loan schemes. For SBI, it extends up to 30 years. But a personal loan, gold loan and loan against property are to be repaid by 3-15 years at SBI.

You can borrow up to Rs 2 crore in the home loan top-up scheme. The maximum personal and gold loan amounts are generally Rs 20 lakh and Rs 25 lakh respectively.

Make an informed decision

Before taking a top-up home loan, make sure you compare the interest rate, processing fee and loan tenure offered by your existing lender with those offered of others. You can change the lender through the balance transfer facility. While transferring the loan, you should calculate the costs involved and assess whether you are actually saving or not.

Tomy cautions, “Some banks consider the top-up home loan scheme as loan against property and sanction it at a higher rate to customers. You have to be careful while applying for it.”

You should check in your agreement whether there is any lock-in period for top-up home loan offered by the bank. In case, you plan to pre-pay the top-up home loan during the lock-in period, banks charge a penalty of up to two per cent of the outstanding loan amount.

Kumar says, “You must check with your bank whether the top-up loan sanctioned is linked with an external benchmark (i.e., repo rate or treasury bills). This will reduce your interest rate.”

Should you opt for it?

Any type of loan should be your last resort, especially in these times of salary and job cuts. In case you face a financial crunch, then first utilise your emergency corpus. If you don’t have one, sell your existing equity and debt investments, or gold holdings.

Do not take a top-up home loan just because it is offered at low interest rates. You need to repay this loan, along with your regular EMIs. Only in case of an emergency situation should you should apply for this loan. Kumar says, “Over a longer tenure, you will have end-up paying higher interest on the borrowed amount. So, you must pre-pay the loan when have surplus income.”

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.