On June 15, Kotak Mahindra Bank launched its ActivMoney feature, which gives customers the benefit of fixed deposit (FD)-like interest up to 7 percent per annum, and the flexibility to access their funds at any time from the linked savings account. This is an auto sweep feature that is offered by several other banks, including Axis Bank, HDFC Bank, ICICI Bank and IndusInd Bank.

What is an auto sweep feature?

This allows a savings account holder to earn higher interest as offered in FDs while retaining the liquidity offered by a saving account. Some banks like Jana Small Finance Bank and Kotak Mahindra Bank extend this facility to their current account holders.

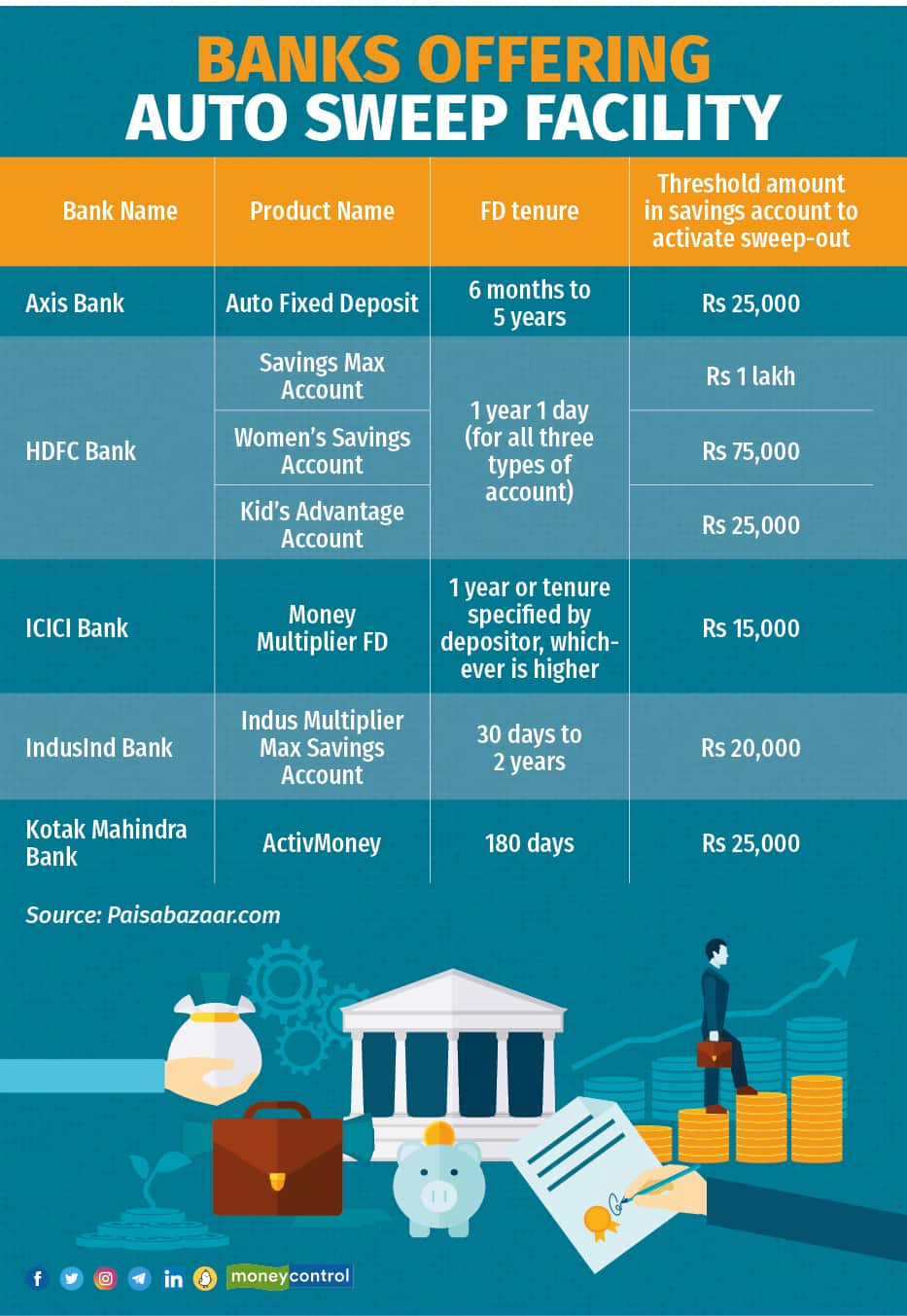

As and when the balance in the savings or current account crosses a preset threshold, the excess amount is automatically used to open FDs for a pre-determined tenure (also called sweep-out). Similarly, when the savings account balance falls below a pre-determined limit, the linked FD(s) are automatically closed and the proceeds credited to the savings account to make up the deficit (also called sweep-in). The threshold limit for sweep-out varies. For instance, at Axis Bank and Kotak Mahindra Bank, the required threshold amount in the savings account is Rs 25,000, at ICICI Bank its Rs 15,000, and at IndusInd Bank its Rs 20,000 (see graphic).

The tenure of FDs and interest rates vary with the banks. For instance, Kotak’s ActivMoney is a facility of automatically sweeping out funds above a threshold from your savings account to a FD account for 180 days. In case of insufficient balance in your account, the FD will be broken prematurely, with no early withdrawal charges, and the required amount will be transferred to your account. This facility will allow depositors to earn interest up to 7 percent per annum on their deposits, compared with an average 3.5 percent per annum for a normal savings account.

“An auto sweep facility is extremely beneficial for consumers who have to maintain large balances in their savings accounts to deal with cash flow uncertainties,” said Naveen Kukreja, co-founder and CEO, Paisabazaar.com. He added that others can also use the auto-sweep facility to build and park their emergency fund and corpus meant for their short-term financial goals.

On the launch of ActivMoney, Rohit Bhasin, president, retail liabilities products and chief marketing officer, Kotak Mahindra Bank, said, “It fulfils the needs of young, aspirational consumers seeking higher returns on their savings whilst having the flexibility to access funds whenever needed. ActivMoney makes banking more rewarding and enables consumers to use their savings more efficiently and effectively.”

How does auto sweep works?

Assume you have a Kotak Edge Savings Account and you opt for the ActivMoney facility. The default ActivMoney threshold for your savings account is Rs 25,000. Now, in case your savings account balance is more than the threshold of Rs 25,000, the excess amount will automatically get transferred in multiples of Rs 10,000 to a 180-day FD. You will then earn the prevailing FD rate on the balance that has been transferred to the FD. As this FD is linked to your savings account, you can access the funds whenever you wish to, with no penalty charges.

In case you are falling short of funds in your savings account, the deficit will be withdrawn from your FD automatically. This feature works similarly at other banks as well but, as mentioned earlier, the threshold limit, FD tenure and interest rate will differ.

Difference between an auto sweep account and a regular FD

To invest in auto sweep FD, you need to give a consent only one time to your bank for a particular savings account. After that, the surplus amount beyond the threshold limit is automatically converted into FD. As a result, you will earn higher returns and you won’t need to visit the bank branch to obtain an FD or apply for FD online on the bank website every time you have a surplus amount in the savings account.

In the case of a regular FD, you will have to request your bank every time to convert your surplus amount in the savings account to an FD.

Also read | Fixed deposits and debt mutual funds: Which is better?

Tax implications on auto sweep account

In the auto sweep account, there will be multiple interest earnings because of sweep-in and sweep-out at regular intervals. You need to reconcile the account statement appropriately for taxation purposes.

The interest in the savings account is exempt till Rs 10,000 under Section 80TTA. On FD under a sweep-in account, interest is subject to income tax according to the applicable tax slab. TDS or tax deducted at source at a rate of 10 percent is deducted from FD interest if it exceeds Rs 10,000 in a year. It’s important to note that your income slab will determine how much tax you have to pay for the interest earned on FDs. For instance, if your income is over Rs 10 lakh, you are subject to a 30 percent tax rate.

Also read | Fixed deposits: Three pointers to resolve the dilemma of peak interest rates

Factors to consider before opting for auto sweep accounts

“Consumers should carefully consider the various terms and conditions related to auto sweep accounts like the tenure offered for the linked FDs, interest rates offered on the tenure, levy of premature withdrawal penalty on the linked FDs, threshold amount for FD opening and closures, the size of the FDs created, etc,” said Kukreja. He underlined that since these conditions can vary widely across banks, consumers should weigh these factors and opt for the bank that suits their payment cycle the best.

Also read | This Father’s Day, show Papa you care: Here are 5 financial gifts for your Dad

What should you do?

An auto sweep account is best suited to conservative depositors, i.e., those who avoid high risks. It’s also beneficial to businesses that get no interest in their current accounts with the bank. If you are a small saver, you may prefer to open an account with a bank having lower threshold limits on the auto sweep savings account.

An auto sweep account is useful if you regularly have a surplus amount after your monthly expenses in a savings account at the end of the month.

“You can also consider the high-yield savings accounts offered by some private sector banks and small finance banks for managing their liquidity and payment cycles,” pointed out Kukreja, adding that account holders can earn interest rates of 5-7 percent per annum from these savings accounts depending on the balance maintained. These savings accounts might offer higher flexibility and returns to the account holders than auto sweep facilities.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.