Many millennials get bored by their job routines. Some dare to dream and go off on their own to start their own venture, get their clients, lay down their rules.

It’s never too late to launch your own startup. And one could have what it takes to make it. The question is: do you have the money and can you afford it?

Here’s a beginner’s guide to leaving your job and starting off on your own.

Set your personal finances in order

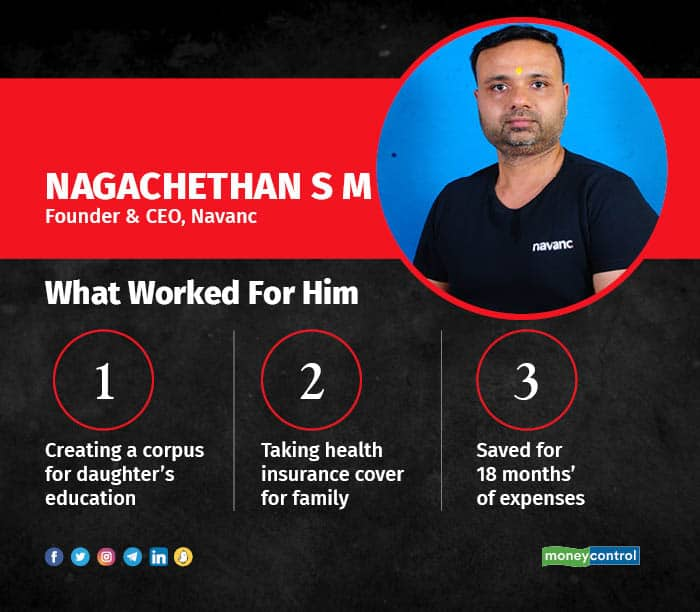

For Nagachethan SM, founder of Navanc, setting aside funds for his daughter’s education was top priority. He invested in bank recurring deposits. He started investing in July 2020, a year before he incorporated Navanc, a fintech firm that provides property credit scores. These are similar in concept to a CIBIL score that measures an individual’s creditworthiness. His venture took off in January 2022.

“I spoke with a couple of my friends who had been through this journey. I felt that Rs 3 lakh to Rs 3.5 lakh would be sufficient for my daughter’s education-related expenses in Bengaluru. I have religiously kept this amount untouched, and this has worked out well for me,” said Nagachethan.

Alongside, he started setting aside money for 18 months’ of living expenses. He took health insurance with a cover of Rs 5 lakh – similar to what his employer provided. Based on advice from his chartered accountant, he decided not to dip into his employee provident fund to meet expenses.

For Anirudh Krishna, an investment advisor and founder of Cumulus Wealth, what worked was savings and a working spouse. “I had adequate savings for two years’ worth of expenses and my wife was working, too. So there was not too much pressure. And I already had life and health insurance,” said Krishna. He left his job to start out as a financial planner.

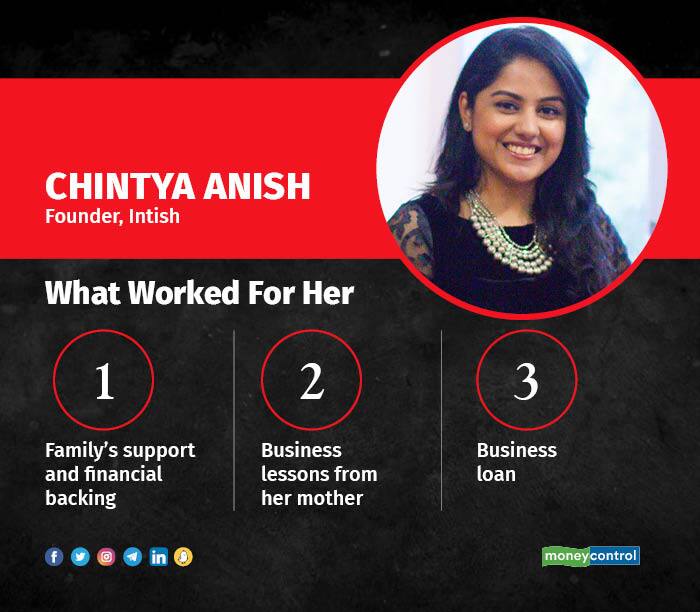

In the case of Chintya Anish, who started a boutique by the name of Intish, support from her family meant she could manage her expenses.

“We were living with our in-laws and my husband was also there to back me financially. Without this, I would have thought twice about starting my business,” said Anish. She worked for her mother, a boutique owner, for two years before setting out on her own. What helped was that her father owned a place that she could use.

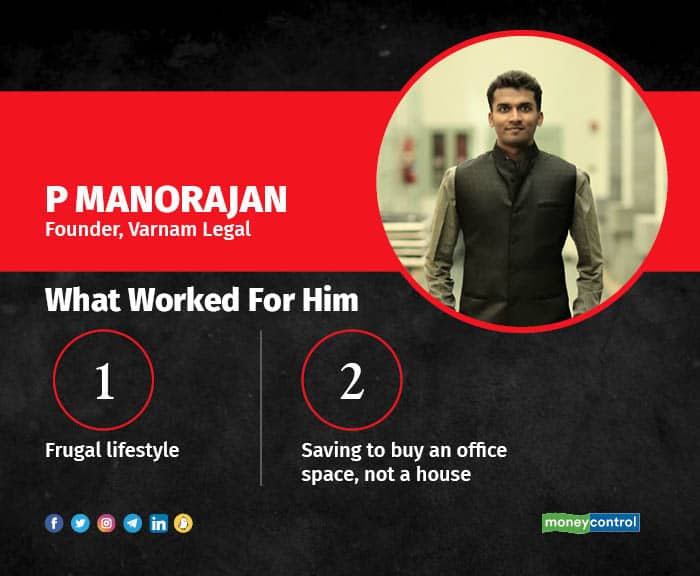

However, P Manorajan did not plan his personal finances before starting his firm, Varnam Legal, in 2016. “The initial 10 months were a huge struggle and I found it hard to meet even my basic needs. I started promoting myself by word of mouth and ensured that I got some work to meet my monthly expenses of around Rs 8,500,” said Manorajan.

He also set aside a small sum regularly to buy law books and journals. This helped give his small rented office a more professional look. Having learnt the hard way, Manorajan began regularly saving and investing some money from 2018. Thanks to this and the sale proceeds from property bought in 2016, he recently purchased an office space in Chennai.

While each business has its own gestation period, experts highlighted the importance of preparations on the personal finances front.

“Set aside money for at least two-three years’ of personal expenses. Even if you cut down on your expenses, some bare minimum will still be needed. Take up health and life insurance while you still have a job,” said Santosh Joseph, founder of Germinate Investor Services.

According to Suresh Sadagopan, founder of Ladder7 Financial Advisories, one should assume it will take at least three years to get a business going and so set aside enough to meet family expenses for this period.

More importantly, pay off liabilities and loans before starting out on your own. Or make sure the equated monthly instalments (EMI) are limited. Remember: one needs to pay EMIs even if the venture takes time to get going.

Also see: MC SecureNow insurance ratings

Set realistic expectations

Beyond budgeting for personal expenses, Sadagopan said one should set a limit on how much to invest in a venture.

“Have a business plan and a cashflow plan. If you think your expenses will be x, assume they will be 2x. And as far as income is concerned, be realistic. Many people are very, very aggressive in terms of their potential business income,” said Sadagopan.

Also read: Don’t have an emergency fund yet? Here are steps to get you started

According to Sandeep Jethwani, cofounder of Dezerv, the biggest mistake that many founders make is underestimating the time taken to break even and so they under-budget the amount needed to invest in the business and the time needed before one can meet lifestyle expenses from business income.

Lovaii Navlakhi, CEO of International Money Matters, said people tend to miss budgeting for certain expenses based on areas they lack expertise in. Someone with experience in marketing may overlook potential legal costs that a business may have to incur.

In Nagachethan’s case, getting a grant and later, funding from angel investors, helped him with his business expenses. Moreover, with approval from his investors, he began taking a small salary once his business completed a year.

According to Ronak Shah and Vignesh Sundararaman, founders of Conscience Multi Family Office, they were able to generate a good revenue stream in three-four months. The two worked for the IIFL Group before starting their distribution business in August 2019.

“We dealt with high net worth clients and many of them easily transitioned to us as we knew their history well. With retail clients, this would have taken at least a year or even longer,” Shah added.

When planning for expenses, one must account for the time needed to get the business started. “It is important to remember that it can take up to three to four months just to have the business registered, get a PAN card and bank account, and all the required licences,” said Joseph.

Prepare for surprises

Being ready on personal finances ensures that you are in a better position to handle business surprises. Anish underestimated labour costs of her boutique. “I thought I could have higher margins while keeping the pricing affordable. But the salaries for skilled tailors were very high and this lowered my margins,” she said.

Later, she decided to take a business loan, which came in handy when she had to pay staff salaries during the first Covid wave. But her experience of applying for the loan was very unpleasant. “The bank manager was unwilling to take me seriously as I was a young woman. This was despite my showing him proof of how my business was performing,” Anish recollected.

While she finally managed to get the loan, she said many women from less-privileged backgrounds may fail to do so despite the existence of government-backed collateral-free loans for women entrepreneurs.

As a person focused on investment research, Krishna did not anticipate the challenges that came up in his investment advisory business. “I was handling both the backend and the frontend work, and it became too much for me. I was initially hesitant to hire someone because I was trying to keep my expenses low,” he said.

On the other hand, this wasn’t a challenge for Shah and Sundararaman. “I am a research person, and Vignesh is good at managing accounts and people. So, we complemented each other well,” said Shah.

Also read: How much money do you need to be truly financially free?

Set a firm deadline

Experts emphasised the importance of setting a deadline for yourself. In simple words, do you have a back-up plan if your venture doesn’t take off and you need to go back to your job?

“I know a lot of people who were unable to convince recruiters about their genuineness and that they had left their jobs to pursue something of their own,” said Sadagopan. He recommended that unless you have a strong network or a good relationship with your boss and are reasonably confident that you can return to work, it’s important to think about the options you have if the venture does not take off.

Joseph recommends that one should first evaluate why they want to switch from a job to launching their own venture.

“Don’t do this simply because you are bored with your job or are unhappy about the money that you are making. Ask yourself if you are trying to be adventurous or are doing this due to peer pressure or FOMO (fear of missing out), or if you think starting your own venture will help you retire early,” said Joseph. These should not be your reasons for making the switch.

If you are passionate about what you want to do and feel that you can make a difference and stand out, go ahead and take the plunge. Just tie up your finances before that.

Also see: MC30 Best Funds

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!