to investigate matter under the provisions of Section 26(1) of the Act, ordered an investigation report within 60 days (Representative Image)")

Nitin Agrawal

Moneycontrol Research

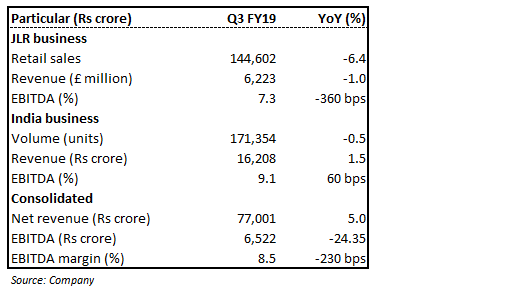

Tata Motors continued its disappointing result streak and posted a very bad set of Q3 FY19 earnings, led by pain emerging from its Jaguar & Land Rover (JLR) business.

JLR posted subdued numbers on the back of further deterioration of market conditions in China and uncertainties regarding diesel vehicles in Europe and UK. This led JLR to post a 6 percent year-on-year (YoY) decline in its retail volume.

Decline in volumes, coupled with negative operating leverage, led to 360 basis points (100 bps=1 percentage point) contraction in earnings before interest, tax, depreciation and amortisation (EBITDA) margin. The management continues to focus on cost control measures to arrest the fall in EBITDA margin. JLR reported a loss for the third consecutive quarter. It also provided one-time asset impairment charges to the tune of Rs 27,838 crore, or 3.1 billion pounds.

On a standalone basis, the company posted meagre net revenue growth of 1.5 percent on the back of muted volume growth. The latter was muted due to challenging domestic market conditions. Notably, the company continued its market share gains in commercial (CV) and passenger vehicle (PV) markets, gaining 60 bps and 50 bps, respectively. EBITDA margin remained stable and stood at 9.1 percent.

Overall outlook for the company remains subdued. We see limited upside from here on and advise investors to stay away.

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed here

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.