This week the National Payments Corporation of India (NPCI) launched a slew of new features for its real-time payments platform UPI that could propel the platform to 100 billion transactions a month, something NPCI CEO Dilip Asbe aims for.

The new features include credit line on UPI, voice activated UPI payment mode ‘Hello UPI’, BillPay Connect that facilitates conversational chat-based bill payments, UPI Tap & Pay based on near-field communication (NFC) technology and UPI Lite X, which is an on-device wallet facility. NPCI also demonstrated how customers can withdraw cash from ATMs through UPI without using cards.

The speed at which NPCI brings innovation on the UPI platform prompted Infosys Chairman and architect of Aadhaar, Nandan Nilekani to call the organisation the crown jewel of India’s technology sector.

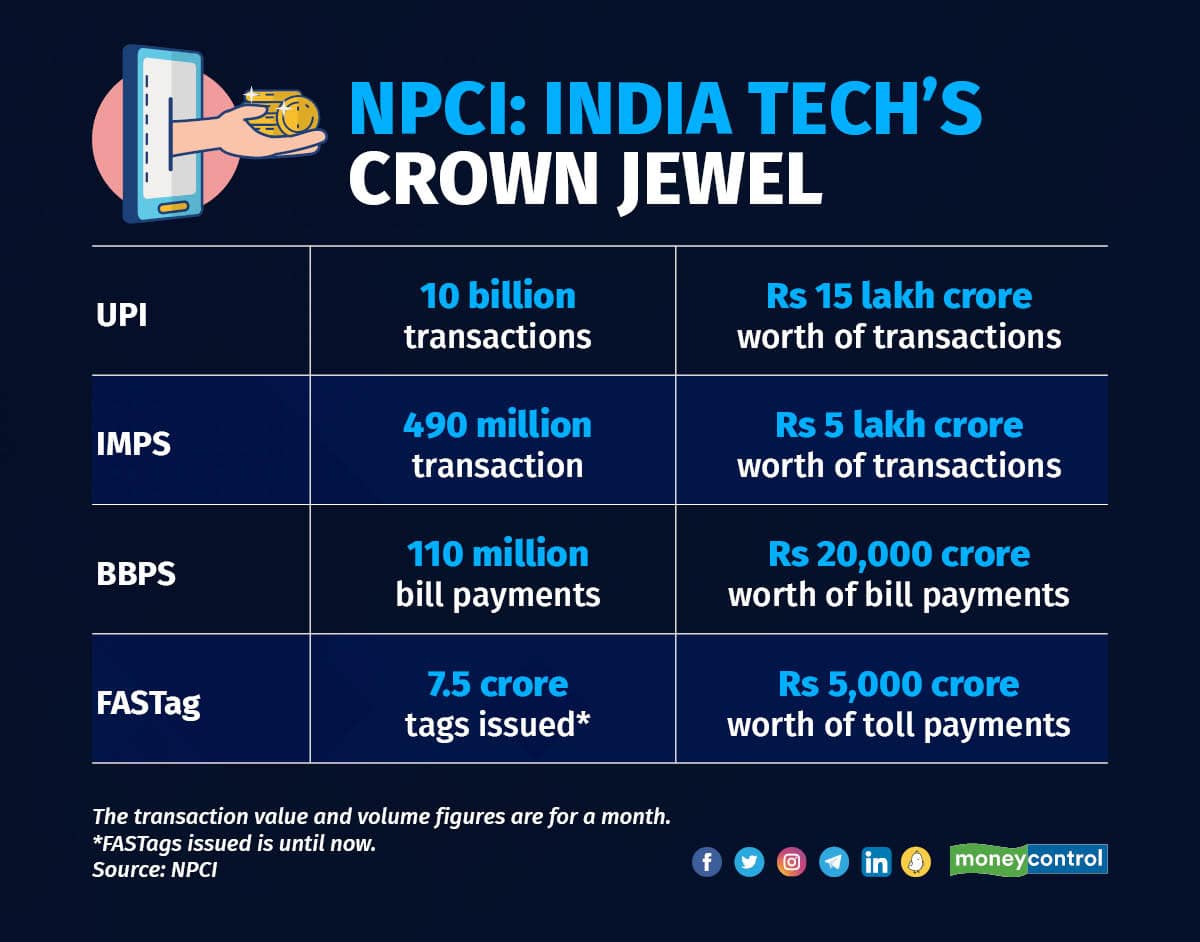

With the support from the Reserve Bank of India (RBI) and the government, UPI has made massive strides, with the platform registering more than 10 billion monthly transactions in August for the first time.

“NPCI is a great example of an RBI initiative that has over time become an independent organisation developing their own fintech products enabling overall innovation, interoperability and inclusivity in the fintech space,” RBI Governor, Shaktikanta Das, said on social networking platform X.

How does NPCI do it?Being founded under the aegis of the central bank, NPCI’s innovations are an easy pass through with the regulator since those are already built on top of existing platforms such as UPI, Rupay, FASTag, BBPS, NACH, AePS, NFS, e-RUPI and IMPS.

“Dilip Asbe’s vision along with the proximity or alignment to the government and regulator allows for quick approvals for use cases. The open architecture allows all of the ecosystem players to innovate using application programming interface (APIs) on top of UPI,” says a senior executive who works with a large UPI payments player. API connects and let two different software communicate.

It also helps that NPCI does not have to do product integrations with banks like other start-ups have to. Banks and start-ups often take months to integrate new products, because there are multiple products being launched.

“The focus of the organisation is key to achieving such results. It also helps that they don’t have to drive direct business. They also have great talent within the organisation and many of them are young fresh graduates who are trained well. Most of our hiring for the UPI division used to be from NPCI,” says a former banker who has worked closely with NPCI on UPI.

The organisation’s technology stack architecture allows for infinite scalability. The ability to think of the network effect of innovations also help NPCI to bring out features that customers and its partners want the most.

“Some of the products have been in the works for a while but full marks to NPCI. They do have a great product team and technology team that supports banks in implementing these features,” says Akhil Handa, a senior executive at Bank of Baroda.

The profit centreThe monopolistic power of the organisation does help NPCI to be a large profit centre among all payment companies. The non-profit organisation had reported profit of Rs 773 crore for the financial year ending March 2022, a growth of over 84 percent over the preceding financial year.

The financials for FY23 are not public yet. The company’s revenue was Rs 1,629 crore during FY22, indicating that its margin is more than 47 percent, whereas most payment fintechs working in the ecosystem are still making losses. Income from payment services constituted 96.1 percent of NPCI’s operating revenue.

While some payment gateway companies are making profits, all of them put together will still not be able to match NPCI’s profits. This prompted PhonePe Co-founder, Sameer Nigam, to say that the highest profit pool in payments still lies with NPCI. “But in this industry, barring a few B2B players it is difficult to make money. In fact, the highest profit pool last year was actually NPCI's,” Nigam said at the Moneycontrol Startup Conclave a couple of months ago.

The payment industry's long-standing demand has been a reinstatement of the MDR or commission charged for facilitating payments. The government had withdrawn the MDR to accelerate digital payments in the country and this has indeed helped a lot of small merchants to adopt UPI payments. However, this has hurt most ecosystem players, including banks, as they lost an avenue to make money from a division that requires a lot of investment to run and add all the new features that NPCI keeps coming up with every now and then.

NPCI is owned by the banks and other payment companies and being a non-profit organisation, NPCI is likely investing all the profits to build more products and add more features.

Of late, the organisation is focusing on internationalisation of UPI apart from expanding the scope and attractiveness of Rupay credit cards through offers and partnerships.

Payment tentacles of NPCINPCI’s most successful product platform remains UPI, which is expected to surpass Mastercard's daily transaction volume of 440 million . UPI does around 340 million transactions a day. Visa, the world's largest card network, processes an average of 750 million transactions per day.

These companies operate in over 200 countries, many of which are much wealthier than India, and they have been around for over 60 years. On the other hand, UPI has achieved this scale in less than eight years.

IMPS was the precursor to UPI and is still widely used for inter-bank money transfers. While flying under the radar, IMPS is fairly big. In terms of transaction value, the platform does transactions worth one-third of UPI’s every day.

Bharat Bill Payment System, established by the RBI and NPCI in 2016, is now run as a separate subsidiary and has more than 20,000 billers on the platform, from electricity companies to telecom companies to loan repayments and school fees payments, among others. Before BBPS was established only 20 percent of bill payments were happening digitally. Today, more than 70 percent of bill payments happen digitally.

FASTag, another NPCI platform, which manages electronic toll collection on most of the country’s highways, today has issued more than 7.5 crore tags. Its monthly collection stood at Rs 5,000 crore every month during this year.

While Rupay is the most successful debit card platform with a more than 80 percent market share in cards issued, it trails Visa and Mastercard in credit cards, where the spending is much higher. However, with the linking of Rupay credit cards with UPI, the platform has now cornered a 25 percent market share in new credit cards issued in the country.

The crown jewelNPCI, with its various products, has not only revolutionised and digitised India’s payments space, it has also created an ecosystem for fintech players to offer products on top of the platform and created multi-billion-dollar private enterprises.

The government is also trying to help developing countries build similar domestic instant mobile and card payment systems for goodwill. This will, in turn, help the Indian government make these systems interoperable with India’s systems such as UPI for international payments and transfers, and could, in the long run, displace the Society for Worldwide Interbank Financial Telecommunications (SWIFT), which handles international bank transfers.

The recent blockade of the Russian payments systems from using American networks such as Visa and Mastercard has made every country realise that a parallel domestic payment system is vital for survival.

Thanks to NPCI, India has the ability to withstand any such financial blockade with a payment technology infrastructure that is superior to what is in use overseas. NPCI has clearly earned the crown jewel title.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.