India’s economy grew 7.8 percent in the June quarter, its fastest pace in five quarters, beating economists estimates and dimming hopes of a policy rate cut in October by the Reserve Bank of India.

Gross domestic product topped both the RBI’s 6.5 percent projection and the 6.6 percent median in a Moneycontrol poll. Growth was also stronger than the 7.4 percent rate in the preceding three months ended March 31 and 6.5 percent recorded a year earlier.

"India's GDP growth accelerated to a robust five-quarter high 7.8 percent in Q1 FY2026 from 7.4 percent in Q4 FY2025, contrary to the expectations of a sequential slowdown as signalled by high frequency indicators. The 7.6 percent growth in GVA was boosted by a sharper than anticipated expansion in manufacturing and the services sector, even as agriculture and mining & quarrying underperformed our forecasts," said Aditi Nayar, chief economist, Icra.

Economists note that the sharper than expected print is expected to dampen any hopes of a rate cut in October meeting of the Reserve Bank of India.

"The sharper than expected GDP growth print, which represents an acceleration over the previous quarter, has doused any expectations that the tariff related turmoil could prompt monetary easing in the October 2025 policy review," Nayar added.

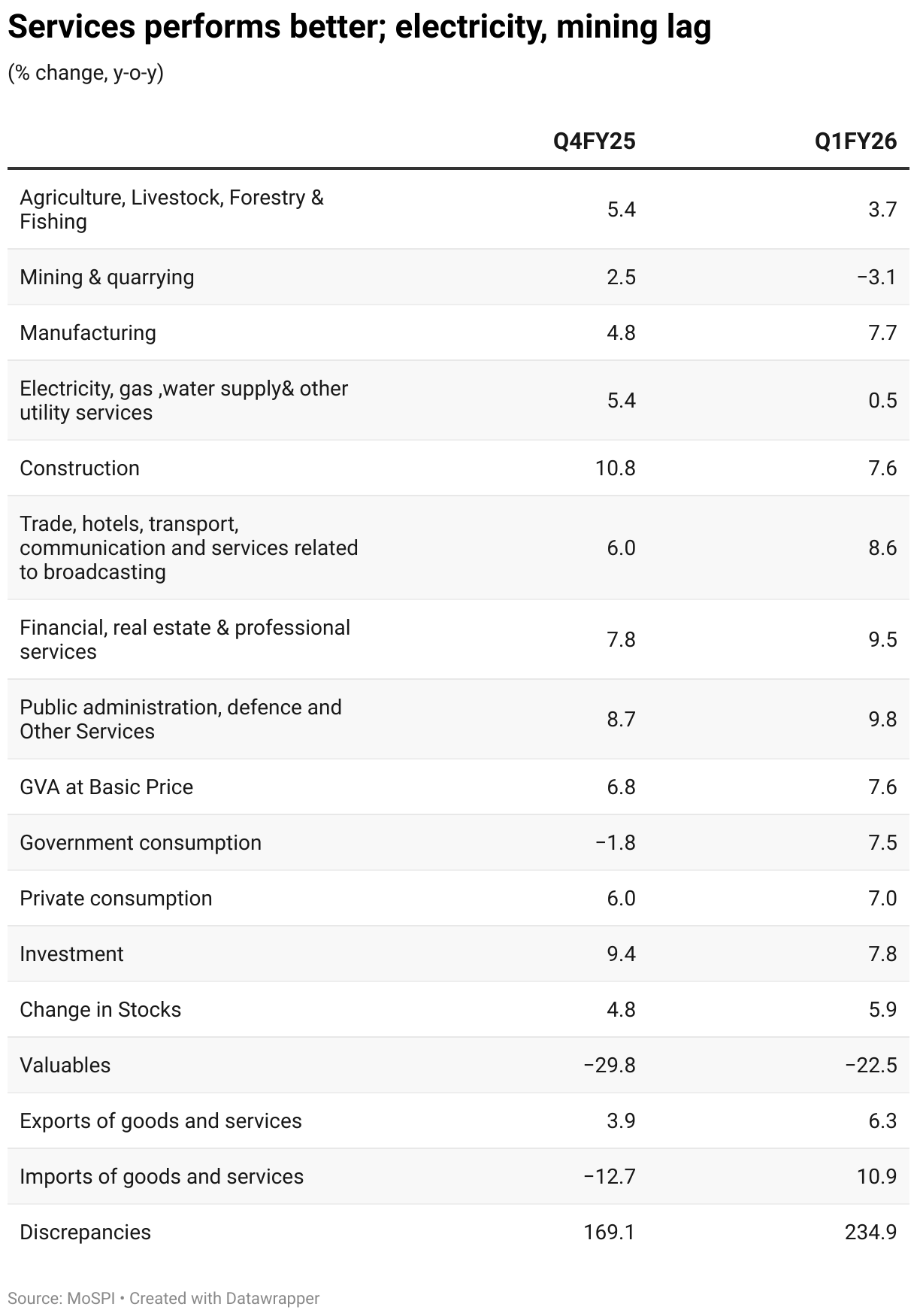

Services Lead the Surge

The services sector was the standout performer, expanding 9.3 percent, its strongest growth in two years, compared with 7.3 percent in Q4FY25. Government services surged to a 12-quarter high of 9.8 percent, while financial services (8.6 percent) and trade, hotels, transport and communications (9.5 percent) recorded their fastest growth in two years.

Services now account for 53 percent of India’s GDP.

Manufacturing Holds Strong, Construction Disappoints

Despite muted industrial production signals, manufacturing grew 7.7 percent, nearly matching last year’s high base of 7.6 percent. Construction growth slowed to 7.6 percent, compared with 10.8 percent in Q4FY25 and 10.1 percent in Q1FY25.

Mining was the biggest drag, contracting 3.1 percent, its weakest performance in 11 quarters. Electricity output grew just 0.5 percent year-on-year, a 19-quarter low, as the early onset of monsoon hit output.

Export growth also was muted at 6.3 percent compared with 8.3 percent a year before.

Private consumption rose to a three-quarter high of 7 percent, supported by a strong rural economy. Government consumption increased 7.5 percent, while gross fixed capital formation moderated, though the investment-to-GDP ratio climbed to a three-year high of 34.6 percent.

Private consumption now accounts for 56.7 percent of GDP, reflecting its central role in sustaining growth momentum.

"The outlook for private consumption is bolstered by developments like income tax relief, 100-bps rate cut, healthy progress of kharif sowing, and upcoming rationalisation of GST slabs, even as discretionary purchases by households could be deferred in Q2, until tax cuts are implemented during the festive season. Moreover, potential job losses in sectors affected by US tariffs could sour sentiment for some households," Nayar added.

The better-than-expected performance underscores India’s resilience, economists noted.

"The economy hence does look poised to clock the growth rate of 6.5 percent for the year notwithstanding the tariff effects which could affect growth by 0.2-0.4 percent. The low price deflator effect would also help in supporting the growth number," said Madan Sabnavis, chief economist, Bank of Baroda.

The low price deflator also played a part in Q1FY26, as nominal growth was just 8.8 percent in the first quarter.

S&P Global Ratings had recently upgraded India's rating after a near two-decade hiatus to BBB, projecting a 6.5 percent growth for the economy in FY26 and 6.8 percent over the next three years.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.