Ruchi AgrawalMoneycontrol Research

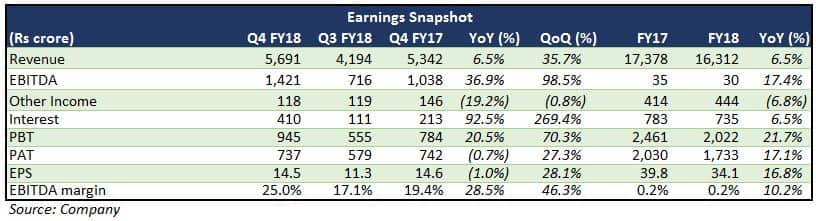

UPL reported an in-line set of Q4 FY18 earnings, aided by a decent eight percent year-on-year growth in volumes, which was evenly spread across regions. Prices remained nearly flat despite higher input costs. While revenues saw a moderate 6.5 percent YoY growth, earnings before interest, tax, depreciation and amortisation (EBITDA) saw a healthy 37 percent YoY growth with a 560 basis points YoY margin expansion. Though the quarter gone by saw some operating cost savings, interest costs nearly doubled YoY.

New product launches drive domestic revenues

UPL’s domestic business grew almost six percent during Q4 on the back of a positive response to new product launches. Rainfall in southern states remained mixed during the Rabi sowing season, with overall deficit around 11 percent. This coincided with the outbreak of the pink bollworm issue in cotton in various states, which impacted sales. Improvement in minimum support prices, farm incomes and a normal monsoon forecast are expected to drive profitability in coming quarters.

High channel inventory keeps demand subdued in Latin America

Despite an overall industry contraction of around four percent, UPL saw revenue growth of almost seven percent in Latin America on account of new products. Delayed rains, dry weather and high channel inventory at the start of the year kept demand subdued.

Low channel inventory in North America and Europe aid volume growth

Q4 revenue growth of seven percent YoY was led by the herbicide portfolio in Europe and wholesome growth of herbicides, insecticides and fungicides in North America. Low inventories at the start of the year aided volume growth in both regions, despite prices continuing to remain depressed.

Improved local business in China

Key regions in other parts of the world saw a healthy double-digit growth in Q4, ticking up overall growth to five percent YoY. Its China business was a major revenue driver despite Australia being impacted by severe drought.

Situation in China

Closure of factories in China owing to environmental concerns have impacted sourcing of inputs, which in turn has hit margins across the industry. UPL too was hit. However, the same was limited as the company is now venturing into manufacturing, though raw material sourcing still remains a concern in some cases. Going forward, the company plans to expand its manufacturing facilities and benefit from a supply glut.

Outlook

Tight cost controls and steady volume growth across regions has facilitated growth despite a tight industry environment. The management has been focussing on technological enhancement and new product developments which aided growth during the year. We believe new launches would bear fruit in the coming term. Improving trend in commodity prices would help enhance revenues and realisations for UPL. Expected recovery of loans to associates in the coming year would help improve its net debt position.

The stock has corrected around 1.3 percent in the last one month and around 10 percent in the last 12 months. It is now trading at 15.7 times FY19e price-to-earning and EV/EBITDA of 9.9 times. The management strategy to expand into manufacturing seems opportune given the closure of Chinese factories. Key positives include an above normal monsoon forecast, focus on technological innovations, new product launches, a geographically diversified portfolio and decent order book line-up. The stock is a long-term play and any underperformance would be a good opportunity to accumulate.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.