Ruchi Agrawal

Moneycontrol Research

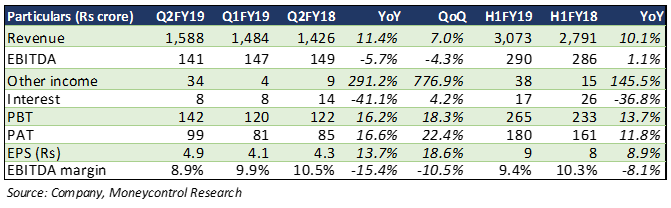

Godrej Agrovet (GAVL) reported a subdued Q2 FY19 earnings, with mixed performance across segments. Revenue saw a healthy 7 percent year-on-year (YoY) uptick on the back of a healthy volume growth. However, earnings before interest, tax, depreciation and amortisation (EBITDA) margin saw a sharp 160 basis points (100 bps = 1 percentage point) contraction due to impact on aqua feed, palm oil and dairy segment margins. Uptick in the other income includes proceeds from the sale of land, which led to an uptick in net profit, excluding which overall profitability remained compressed.

Animal feed

The 16 percent volume growth was driven by layer and broiler feed business, which led to a healthy 16.3 percent sales growth for the segment. High input cost and low pricing power in the shrimp feed segment impacted profitability of the aqua feed business.

Low milk prices continued to impact pricing in the cattle feed business, where margin remained subdued. GAVL is strategically focussing on gaining volumes going forward, which, as per the management, might impact margin in the short term. However, the company would stand to benefit in the longer run as better plant utilisation levels leads to lower cost of production.

Sale of products below the minimum support price (MSP) in the current kharif season augurs well to lower procurement cost for raw materials in the animal feed segment.

Crop protection

The crop protection segment posted a 25.2 percent growth in revenue and a 15.4 percent growth in profit. Strong performance was a result of strong traction from new products launched in the past quarters. Astec Lifesciences posted a 17.4 percent revenue growth and a 430 bps EBITDA margin expansion.

Foreseeing irregularity in supply from China, the management ventured into backward integration since last year. Benefits of this aided growth in Q2. Positive traction from the export market and benefits from a weaker rupee also boosted segment growth.

Going forward, while export traction and growth of new products stand to boost the segment, below MSP kharif sales might lead to lower disposable incomes with farmers and impact sale of products in the upcoming rabi and next year’s kharif season.

Palm oil

While sales for the segment remained largely flat, profitability saw a sharp 26 percent contraction owing to late arrival of fruit bunches due to a below normal monsoon. The management, however, highlighted that the same is more of a timing issue and the spill over benefit of the same should be seen in Q3 and Q4 FY19.

Dairy

Declining butter prices, along with a supply glut for buffalo milk and butter, continued to impact profitability of this segment. However, the company is now focussing on expanding its value-added product portfolio, with strong marketing for new product launches like flavoured milk, ice-creams and ghee. With a higher margin profile, this is envisioned to improve profitability of the segment going forward.

OutlookWith strategic plans and policy support, segment performance is expected to improve in the second half of the year. The spill over impact of late arrival of fruit bunches is expected to improve performance of the palm oil business. New product launches in crop protection segment are expected to drive growth by FY19-end. Animal feed performance has started to stabilise now.

The aqua feed segment might remain an overhang and overall animal feed margin might remain under pressure in the short term. However, with increasing scale, the segment is expected to show healthy growth in the longer run. With clearing of inventory in the dairy segment and strategic launches in the value added product portfolio, sales for the segment are expected to improve in the second half.

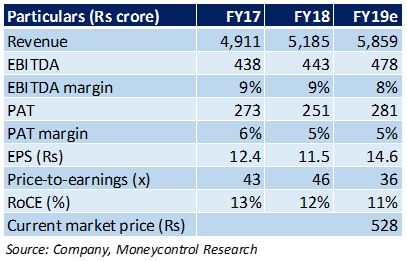

The stock is trading 15 percent above its October 2017 issue price of Rs 460. In the past three months, the stock has corrected around 12 percent and is trading at a 2019 estimated price-to-earnings of 39 times and an enterprise value-to-EBITDA of 22 times. Although some hurdles in the operating environment have curbed growth at present, we expect these to stabilise and overall earnings to improve in FY19. We view GAVL as a quality stock, positioned to deliver healthy long term returns.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.