For more than a year now, there’s been no shortage of economists declaring that the US consumer was nearly tapped out, having run through pandemic-era fiscal largesse while inflation raged. As a result, a recession was just around the corner. Time and time again, though,American households have proven those forecasts wrong. Now, a major revision to government data on personal income and savings reveals why.

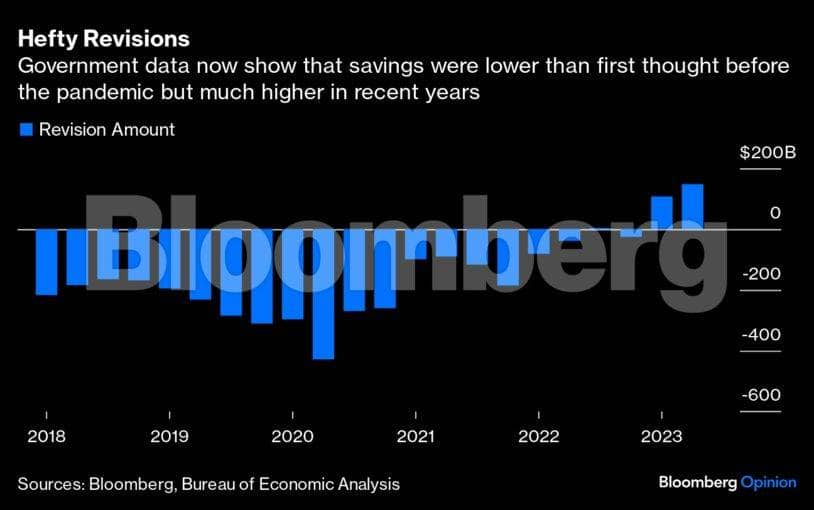

The updated numbers reveal a consumer with some $400 billion more in earnings since 2019 along with more prudent spending than previously reported. Crucially, the revisions confirm that the massive savings buffer households built up during the pandemic remains largely intact. In terms of the numbers, Americans are socking away $100 billion a year less than they did before the pandemic, which is worrisome but not as apocalyptic as the $830 billion less that was first reported.

With revisions as large as those, perhaps the recession many economists are still predicting may be delayed yet again — if it happens at all.

Having a handle on where household finances stand is critical because consumer spending accounts for about two-thirds of the economy. The pessimism began with an analysis of savings released by the Federal Reserve in October 2022. The central bank estimated that households built up excess savings of $2.3 trillion beyond what would normally be expected over the course of 2020 and the first half of 2021.

The increased saving was driven by both government stimulus payments during the pandemic and a sharp reduction in consumer spending as the economy shut down and Americans stayed home. Yet, by the summer of 2021, Fed economists estimated that surging inflation, increased consumption and the end of government stimulus were leading households to deplete those savings. By mid-2022, a quarter of that $2.3 trillion was gone — or so they thought.

Two essential inputs are required to estimate personal saving. One is how much households “should” have saved and the second is how much they actually saved. The recent government revisions reveal that Fed economists were wrong on both counts. The reason why is that new data indicate that Americans saved less than previously thought in the years leading up to the pandemic, and have saved more than thought during and after the pandemic. Revisions to the earlier years are important because the Fed used the wrong data to calculate how much households “should” have saved.

So, both the level of savings in 2019 and the pace at which those savings grew were lower and slower than the economists estimated. Those two effects amplify each other and suggest that the amount Americans “should” have saved is likely $2 trillion to $3 trillion less than what the Fed economists initially calculated. The Fed’s overestimate was not only massive, but insidious as well. Its analysis made it look like excess savings were being steadily spent down by $150 billion each month, putting households on a spending trajectory that would inevitably end with empty bank accounts and maxed out credit cards.

It's not as if there weren’t signs that something fishy was going on with the data. Although the Fed estimated that savings had been depleted by $2.3 trillion by the second quarter of 2022, total checking account deposits were at an all-time high. Those deposits have since declined by a few hundred billion dollars but remain more than $3 trillion higher than before the pandemic. The Fed analysis forecasted excess savings would be depleted by August.

The good news goes beyond just households having a larger cash cushion. The fact that excess saving has barely declined means that spending was never as out of whack as we were led to believe. It casts the recent strength in retail sales and increase in credit card balances in a more positive light. If you believed that excess savings were nearly gone but that consumers just couldn’t stop spending, then record credit card debt looks like a looming disaster. But once you see that households still have trillions of dollars in cash, it’s clear that spending and incomes are well matched. Indeed, the rise in credit card balances suggests a consumer that is optimistic about rising incomes.

Optimism is also confirmed by the comprehensive data revision. It reveals that personal income increased more rapidly over the past two years than first reported. Personal income that is both higher and rising faster implies that high levels of consumer debt are a result of people feeling more comfortable making big-ticket purchases that are paid off over time.

Contrary to popular belief, consumers have not been spending beyond their means, depleting their savings, or turning to credit cards in desperation. There is no looming consumer disaster on the horizon and no reason to expect a consumer-led recession anytime soon.

Karl W. Smith is a Bloomberg Opinion columnist. Views do not represent the stand of this publication. Views are personal and do not represent the stand of this publication.

Credit: Bloomberg

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.