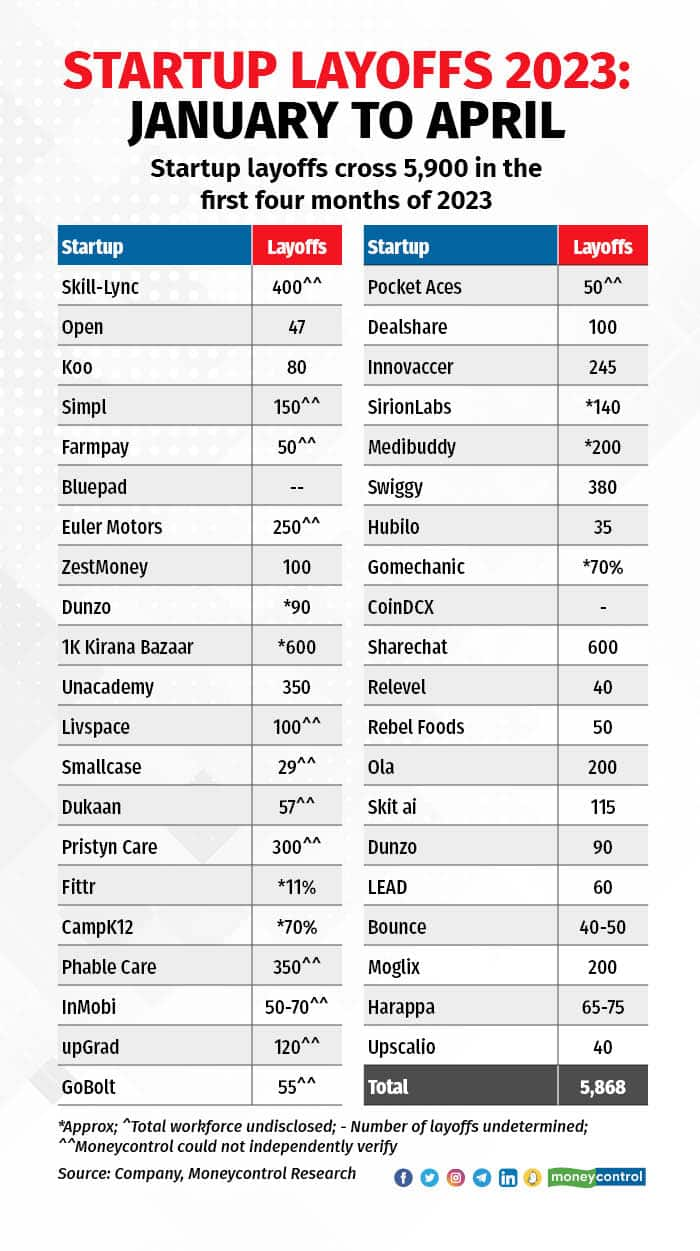

With funding taps down to a drip, Indian startups have let go of almost 6,000 employees in the first four months of 2023 in a bid to reduce costs and target profitability.

About 41 startups let go of approximately 5,868 employees in the first four months of 2023.

Layoffs from January to April 2023

Layoffs from January to April 2023

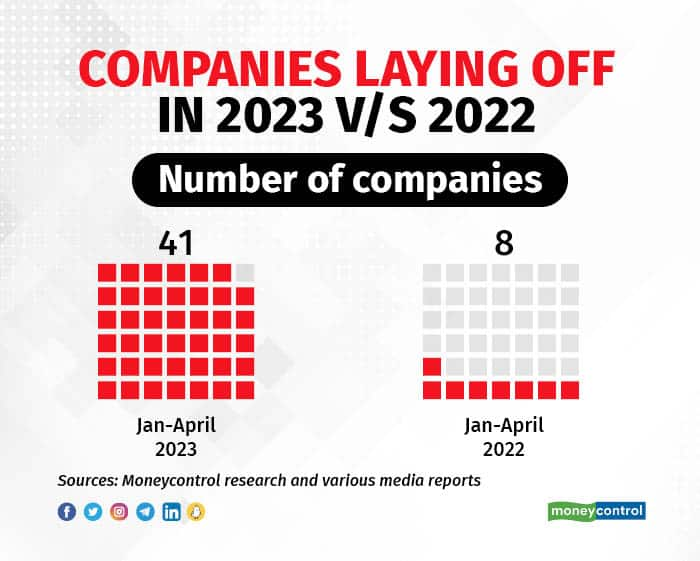

Last year, during the same period, eight startups had done most of the downsizing, letting go of 6,040 people, a tad more than in 2023.

Layoffs so far: 2023 v/s 2022

Layoffs so far: 2023 v/s 2022

“Companies that laid off at the beginning of 2022 were those that could not survive if they did not take the decision. The layoffs that we see now are more precautionary. Founders, who earlier had the mindset, ‘If we need capital, give me 3-6 months, we will get it,’ now know they cannot rely on that anymore,” Scaler co-founder Abhimanyu Saxena told Moneycontrol.

Prolonged funding winter

This comes at a time when private equity and venture capital investors have been going slow in funding high-growth companies amid the uncertainty stemming from elevated inflation, rising global interest rates, the spectre of a recession confronting the West, and the war in Europe, which has disrupted supply chains.

Moneycontrol, citing figures from startup data platform Tracxn, had reported earlier on how the first quarter of 2023 saw funding for India’s startups fall to about a third of the level it was at in the same period last year. In March alone, investors participated in 122 rounds and invested about $3.6 billion, against $5.69 billion invested across 406 funding rounds in the year-ago period.

Investment has only favoured companies with positive unit economics and a clear path to profitability. In a bid to appear eligible for funding, startup founders are now trying to chase these metrics, which just a year ago used to be set aside as a worry for the future.

Many had to moderate their burn, reevaluate growth expectations, pivot from their current business models, and in some cases, even get acquired or shut down.

“Founders understand that there is no point waiting, burning cash for an entire year with a model that is not scaling, and then having to shut down,” Saxena added.

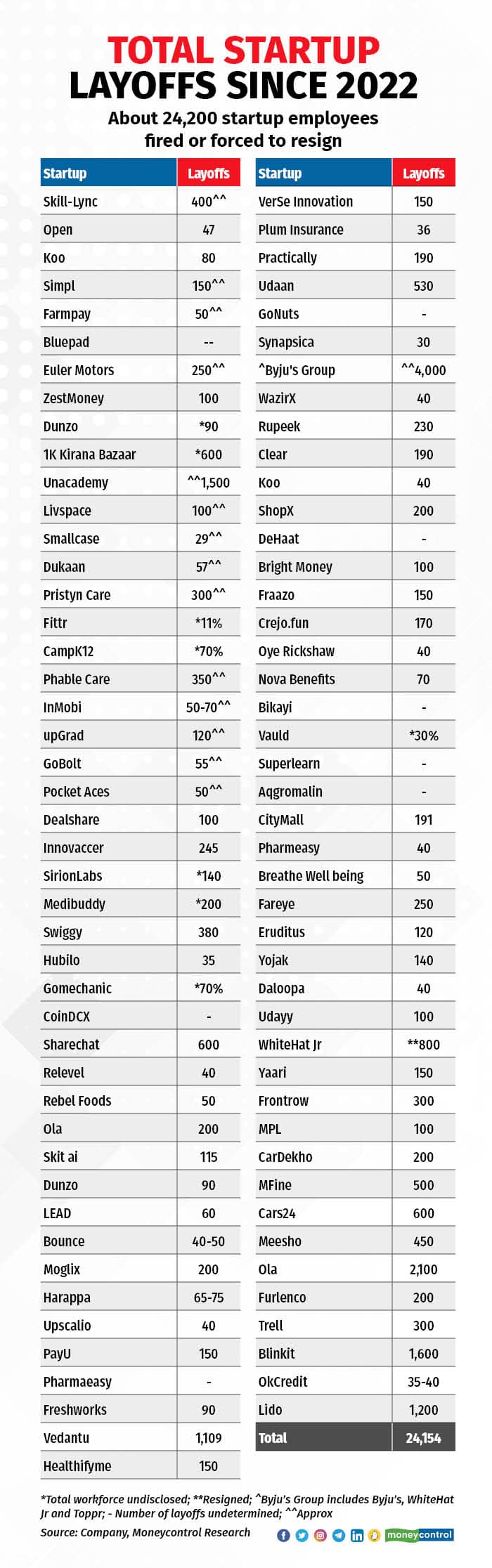

Downsizing of staff has become one of the decisions companies have had to take. To date, close to 90 Indian startups have sacked a total of 24,200 staff members since the beginning of 2022.

The graphic is based on Moneycontrol research and various media reports, Pristyn Care maintains that the company let go of about 45 employees only

The graphic is based on Moneycontrol research and various media reports, Pristyn Care maintains that the company let go of about 45 employees only

This is in sharp contrast to 2021, when funds were flowing in freely, and new-age startups, especially in sectors such as education and tech, hired aggressively and ran up high employee costs as they sought to sustain their unprecedented growth.

Also Read: How many jobs did startups create since 2020?

“You overhired and you paid more for talent than you had budgeted for and you're not getting the productivity, neither are you getting the demand. What are you going to do? The most expensive resource is labour after all,” said Anirudh A Damani, managing partner of Artha Venture Fund.

Pain in Edtech continues

Edtech is a sector in which employee costs are generally the biggest expense head. Unacademy, PhysicsWallah, Vedantu, Eruditus and upGrad, the five edtech unicorns that have filed FY22 results, cumulatively spent about Rs 5,465 crore on employees, including non-cash ESOP costs. This was a 47 percent increase over the previous year, when the five companies spent nearly Rs 3,724 crore, the filings showed.

“Any company that has created an extremely large team during a hyper-growth phase will lay off. When headcount reaches that scale, it becomes a fixed cost for the company every month,” said Saxena. “During some months, the revenues aren’t that great, which is nothing to do with team performances but more due to market conditions. Regardless, you can’t do away with that cost, they have to let go of people.”

To be sure, Indian edtech, which became the poster boy for the startup boom in 2021, has accounted for more than half of the total layoffs since the beginning of 2022. To date, startups in the sector have let go of about 10,700 people since the beginning of 2022.

Slowing demand for online learning, coupled with a drop in funding from Private Equity and Venture Capital firms, has had a domino effect on India’s once thriving edtech companies.

The latest to join the growing list of edtech startups axing jobs is Skill-Lync, an upskilling startup for engineering students and graduates, which has handed pink slips to as many as 400 of its employees citing tough macroeconomic conditions.

“Given the macroeconomic conditions, we’ve decided to moderate our growth expectations and slow down some of our projects focused on the future. In the existing business, we have changed our delivery model to provide better learning outcomes using a combination of technology and experts — this led to some role redundancy,” said SuryaNarayanan PaneerSelvam, co-founder of Skill-Lync, in a statement.

The company also said it consolidated its operations across Chennai, Bangalore, and Hyderabad, with only corporate teams operating from Pune and Delhi, leading to a further headcount reduction.

Skill-Lync is not alone, many startups have been feeling the heat of the slowdown in demand post-pandemic amid the bleak funding environment.Slowdown in demand

Scaler’s Saxena said the company is trying to navigate through the funding trickle with frugality and will stay away from hypergrowth.

“We are not targeting massive topline growth in the current environment. We will continue to grow at a sustainable pace but will not look at growing our business at triple or four times,” he added.

Damani added that while revenues are not contracting, the pace of growth has slowed. “Companies are looking back and saying, ‘We were expecting, let’s say, 50 percent growth this year, but we got 30; next year if the expectation was 40 percent, we have to now prepare for 20 percent growth.’ The differential is pretty huge,” said Damani.

“When you are aiming for a certain kind of growth, you hire people in anticipation of that demand to show up. When it doesn’t, you might hold on to them for one month, or two months. But how long can you hold on? Eventually, you have to lay people off,” he added.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.