By Harpreet Singh

In sync with Modi Government’s intent to provide affordable housing for masses, the GST Council in its last meeting held on 18 January 2018 recommended for concessional rate of 12 percent (8 percent effective tax after deducting value of land) on houses constructed under Credit Linked Subsidy Scheme (‘CLSS’) scheme for Lower Income and Middle Income Categories (LIG and MIG).

In terms of the overall tax cost, GST (Goods and Services Tax) is beneficial for the home buyers as under the new tax regime builders are allowed to claim a set-off/ deduction of the taxes paid on their purchases against the output tax charged to buyers, thereby reducing their overall tax cost. Accordingly, VAT and Excise paid on the purchase of cement, steel, bricks etc. and Service tax paid on manpower supply services, leasing of equipments etc. which thus far were a cost to the builder would no longer be a cost.

Let’s try and understand the pre and post GST difference in a little detail in the ensuing paragraphs

Pre-GST regime

In the pre-GST era, builders/ developers were required to pay Service tax at the rate of 4.5 percent and there were variable VAT rates across States ranging from lump-sum/ composition rate of 1 percent (Haryana and Maharashtra) to a normal rate of 4 percent-5 percent (Karnataka, Tamil Nadu). Therefore, the overall tax incidence of Service tax and VAT varied from 5.5 percent to 10 percent on the output price. Further low-cost houses covered under government schemes such as Pradhan Mantri Awas Yojana and other State housing schemes were enjoying exemption from Service tax.

It is worthwhile to note here that, as builders/developers were discharging Service tax on abated rates, they were not entitled to claim cenvat credit (i.e. Excise Duty and CVD) in respect of various inputs used in construction. Similarly credit of VAT was not available, where Developer was enrolled under lump-sum/ composition scheme and thus, the same was the cost to the builder. To illustrate, tax incidence on its principal inputs viz. steel and cement was 17 percent and 24 percent respectively and other imported building hardware such as doors and windows, metal goods etc. attracted CVD, which was entirely a cost in the hands of developer. The tax burden was eventually passed on to the buyers resulting in cascading of taxes and thus, overall higher prices.

GST regime

GST is to be levied at the rate of 18 percent (effective rate of 12 percent after deducting one-third of the amount charged towards the cost of land) on under- construction properties treating them as the supply of services. Further, as per the latest recommendations made by the GST Council, the concessional rate of 12 percent shall be applicable on houses purchased under CLSS scheme (effective rate of 8 percent after deducting one-third of the amount charged towards the cost of land).

Also, under GST, builders are entitled to claim full input tax credit on all its procurements such as inputs, input services, capital goods, consumables etc.

Accordingly, buyers need to discuss the benefit of additional input tax credits with the developers and re-negotiate the price being charged on account of the change in the tax regime.

It is also pertinent to note that while the overall cost of construction seems to have gone down under post GST regime on account of additional input tax credits for the builders, the intent to pass on the benefit of lower cost of construction to the end buyer appears to be missing in the market.

In order to ensure that the aforesaid benefits reach the ultimate buyers, the Government has started questioning the developers/builders who are not passing on the benefit of reduced rates and additional input tax credit by triggering the anti-profiteering measures.

However, it will not be incorrect to say that calculation of benefit of input taxes to be passed on to the ultimate buyers is challenging, considering the complexities of the industry and fact that major raw material (land) and complete product (building) are still outside the purview of GST.

We have discussed few practical examples as under to illustrate the market trend and what buyers need to push for:

ILUSTRATION 1 – Extension/ Renovation work in cooperative housing societies

Since the time Government has approved the increase in carpet area of houses (FAR approvals), many contractors have undertaken contracts for extension of flats in various localities like Dwarka, Rohini etc. in Delhi. In cases where the construction of such extensions was initiated in pre-GST regime but completed after GST implementation, the contractors are asking for a hike on account of increased GST rate.

While an effective rate of indirect taxes may have gone up from say 10 percent (VAT and Service tax) to 18 percent, the benefit of additional input taxes should also be passed on by the contractor to the Society. Thus, the buyer i.e. the Cooperative Housing society should be smart to re-negotiate with the contractors to reduce the base price (of say 100) on account of additional input tax instead of simply paying the tax at the new rate on the base price.

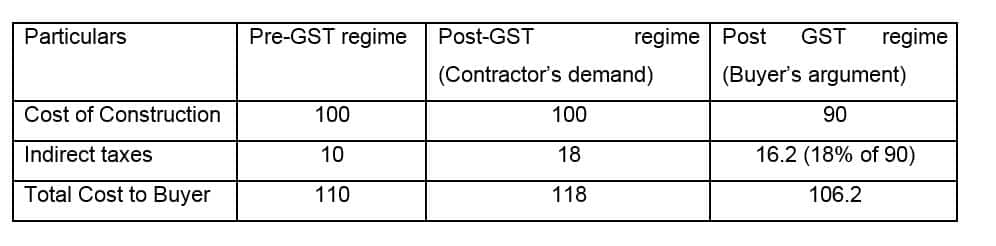

To illustrate:

In the aforesaid example, it has been assumed that the contractor would get additional input tax credit of Rs. 10 and hence, the same needs to be reduced from a base price of Rs. 100 before the new rate of 18% is being applied. Thus, 18% should be applied on Rs. 90 (i.e. Rs. 100 less Rs. 10) instead of Rs. 100, bringing the overall price down to Rs. 106.2 from 110.

ILLUSTRATION 2 - Subvention Scheme (20:80 Scheme)

Under subvention schemes floated by few builders, the buyer is asked to pay a small portion (say 20 percent) as advance towards the purchase of a flat and the balance portion (80 percent) is paid only at the time of possession of the flat. Thus, in this case, three is no construction linked payment.

Th are a lot of on-going construction projects, in which the buyer has paid the initial portion of advance (say 20 percent) under the pre-GST regime and the final payment of (say 80 percent) would be made under the GST regime.

In terms of transitional provisions under GST, no GST is applicable on transactions on which tax has been leviable under erstwhile laws. Accordingly, GST shall only be applicable to those tranche/ portion on which erstwhile taxes have not been paid.

However, there have been instances, where a builder is enforcing GST on the full contract value (i.e. 100 percent) instead of only the balance portion of 80 percent, from the flat buyers on such semi-constructed properties. In view of clear transition provisions, buyers should pay GST only on post GST installments.

To conclude, while at a broader level, it is evident that effective output tax rate has increased from 5 percent-10 percent to 8 percent/12 percent, it can be seen that GST levied on most of the inputs used in construction of property viz. cement, steel and other fittings shall be a pass-through in the hands of a builder/ developer and accordingly, benefit of the same should be passed on to the ultimate buyers.

At an industry level, while few builders have extended the benefit to the buyers by way of offering festive discounts and waiver of GST, there are many more contractors/ builders who are unwilling to pass on the benefit of input tax credit to the buyers.

Thus, in their own interest, all home buyers should be aware of the basic concept of input tax credit under GST and the benefit accruing from this to their builder/ developers, so that they can negotiate reasonably with the builders, and are not taken for a ride.

(The writer is a Partner at KPMG)

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.