Weighing in on the moratorium on loan payments, former Reserve Bank of India (RBI) governor Raghuram Rajan said banks should end soon. He recalled the Andhra Pradesh microfinance crisis to buttress his rationale. “Once you told people don't pay, it became hard to get them back into the payment habit because they have not saved any money. They did not have any money.”

On May 22, Reserve Bank of India (RBI) extended the moratorium on term loan equated monthly instalments (EMIs) by another three months, until August 31. The moratorium, which was launched on March 1, was aimed at providing relief from the financial crises seeded by the coronavirus pandemic. On the fears of a spike in non-performing loans once the loan moratorium term ends, Rajan said sometimes you recover more on your loan by writing down your debt and recognising losses. “More than private sector banks, public sector banks are worried about writing down their debts as they have to face various enquiries.”

Lauding RBI’s role in handling of the crises, Rajan said thanks to the credibility of the central bank, the rupee has not plummeted “despite our inability to contain the virus, fears around our growth trajectory as well as our fiscal situation”. Ahead of the Monetary Policy Committee’s (MPC) decision expected on August 6, Rajan, feels it is important that the RBI shows commitment towards inflation “for that confidence to continue.”

Rajan warned that the pandemic may change people’s consumption habits, making them more frugal. He called on the government to announce steps to bring the virus under control rather than wait for a vaccine as does not see one being rolled out until the first or second quarter of next year in a virtual interview moderated by Anku Goyal, founder of IndiaPodcasts. Srinath Sridharan, business leader and market commentator, on cryptocurrencies and Rajeev Poddar an economics teacher from Kolkata and founder of Knowledge Capsules also participated in the interview. Edited transcripts:

Rajan warned that the pandemic may change people’s consumption habits, making them more frugal. He called on the government to announce steps to bring the virus under control rather than wait for a vaccine as does not see one being rolled out until the first or second quarter of next year in a virtual interview moderated by Anku Goyal, founder of IndiaPodcasts. Srinath Sridharan, business leader and market commentator, on cryptocurrencies and Rajeev Poddar an economics teacher from Kolkata and founder of Knowledge Capsules also participated in the interview. Edited transcripts:

Goyal: It has been almost four months since we have been living with the novel coronavirus. Which sectors do you see a recovery pattern in? Are you already seeing green shoots there?

Raghuram Rajan: The extent of the lock down in India was very severe. As a result, activities fell to lows that have not been seen historically in India. Which means that once you lift the lockdown restrictions there will be a sharp recovery for some time. The question is how far up does it go to, and that depends on two or three things.

One, it depends on the pace of opening up. Are you opening up all parts of the country quickly? Are you opening up every business? If people don't have a job, then they don’t have the ability to consume.

Two, whether the factories that are opened up can produce because their supply chains are in places which have not opened up. As much as the demand side, you need the supply side to come back also.

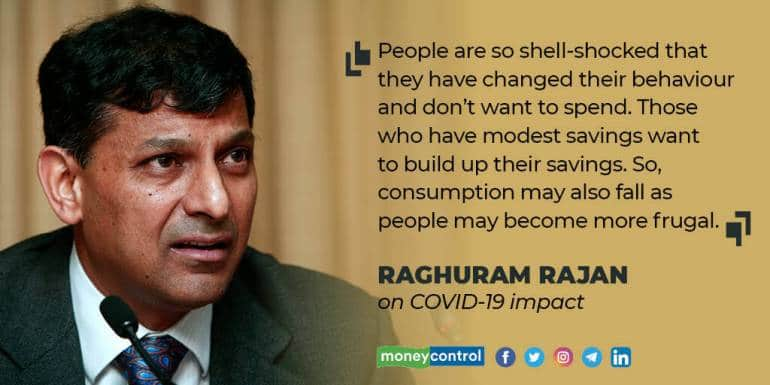

The third factor is the consumer behaviour. People are so shell-shocked that they have changed their behaviour and don't want to spend because they fear the virus may return in a bigger way or something else may happen. People who have modest savings want to build up their savings. So, consumption may also fall as people may become more frugal.

Goyal: Even when that opening up happens, will the fear psychosis allow real consumption to come back on track?

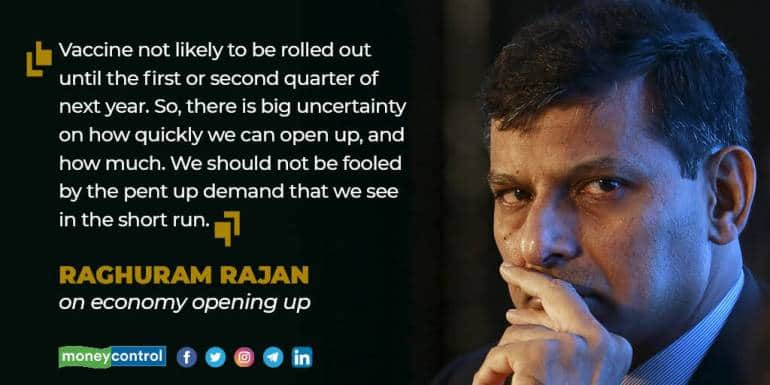

Rajan: It will take time and for that it will require that we control the pandemic. A vaccine is not likely to be rolled out until the first or second quarter of next year. So, there is big uncertainty on how quickly we can open up and how much can we open up. We should not be fooled by the pent up demand that we see in the short run. We see agricultural demand and some industries are happy that there is pent up demand. But once that demand is met, is there going to be something behind it that is a big worry.

Goyal: How do we kick-start credit demand? Where will the growth capital come from?

Rajan: I think you first need real demand before you get credit demand. If I am not selling, I don't need working capital financing because I am not producing. Let us not say that lack of demand means there is nobody who can benefit from credit. It may be that there are over indebted firms who know that when they go to the bank the latter is going to laugh at them because they don't have collateral. I was in a meeting with a micro, small and medium enterprise (MSME) from Chennai and Kolkata. If they are given credit, they will take it. But many of them, seeing their situation, don't really think they can access credit. So, we need other parts of economy to fire. We should also not be complacent that the lack of demand is purely due to lack of demand. It may also be that people may see that there is going to be no supply if I do demand it because banks are going to be totally risk averse -- a point that the Reserve Bank of India has also been making now.

Goyal: The actual impact of COVID-19 will be assessed when we see financial institutions recognise their non-performing assets (NPA) once the moratorium period ends. We know that the NPA rate will increase drastically as has been insinuated by the recent financial stability report. Since you played a pioneer role in bringing into recognition the NPA issue, would you support the halting of the insolvency and bankruptcy process. Restructuring outside the court could be one way. As the whole issue with regards to NPAs and capital requirement is a complicated one, are banks being risk averse for that reason.

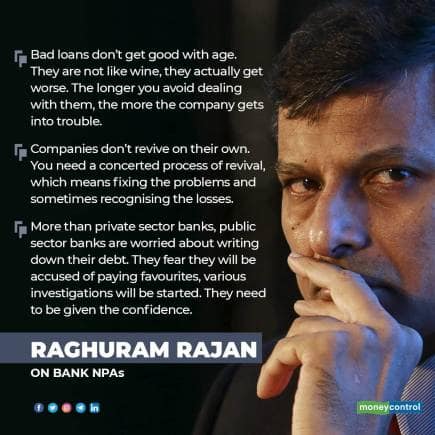

Rajan: I think it is complicated, but not doing anything is the worst thing to do under these circumstances. There is a temptation to say let us push it into the future. Bad loans don't get good with age. They are not like wine, they actually get worse. The longer you avoid dealing with them, the more the company gets into trouble. There is little chance the promoters will be willing to invest in the company as they know it's a bankrupt entity.

Companies don't revive on their own. You need a concerted process of revival, which means fixing the problems and sometimes recognising the losses. Sometimes you recover more on your loan by writing down your debt.

For instance, if I keep it at Rs 100, it is going to be difficult for the firm to raise working capital and even operate. Promoters are going to lose interest. If I keep that loan at Rs 100, it will give me back Rs 50 when I sell off the plant and equipment. On the other hand, if I write it down to Rs 80 and the promoter has the ability to borrow and invest working capital, may be that Rs 80 loan will be worth Rs 80. So, restructuring can be beneficial even to lenders if it makes an asset, which is deteriorating in value, a better asset. That is really what banks have to think about.

More than private sector banks, public sector banks are worried about writing down their debt. They fear they will be accused of paying favourites, various inquiries and investigations will be started. They need to be given the confidence that they can restructure and not be accused of corruption. For that, banks have to put in place structures that allow bank officers to take decisions reasonably and not face inquiry commissions. There will be an odd corrupt official but we have to find a way to get them without halting the process.

Goyal: The extension of the moratorium, even if the loan amount piles on, is okay to do for now because we are in a pandemic? So, there is no way out for anybody?

Rajan: The moratorium will have to come to an end at some point. The longer the moratorium lasts, more is the unpaid loan amount and tougher is it to restart payments. Do you recall the Andhra Pradesh microfinance crisis? Once you told people don't pay, it became hard to get them back into the payment habit because they have not saved any money. They did not have any money. So, those became serious NPAs and a lot of microfinance institutions were severely impaired after that. The longer we tell people not to pay, the harder it will become for banks to collect anything on those loans.

Goyal: Rajan you have always spoken about the inflation target as being important for the growth trajectory of the economy. Now that we have crossed that boundary of +-2 percent, for 4 percent inflation, is the focus required to be on inflation containment. Can we reasonably be there around that going further?

Rajan: One of the Institutions working well right now is the central bank. The credibility of RBI is one reason why the currency has not plummeted despite our inability to contain the virus, fears around our growth trajectory as well as our fiscal situation. People still have confidence in the rupee and it is very important that the confidence continues. For that confidence to continue, it is important that the RBI shows commitment towards Inflation. If there is no expectation that it will contain inflation going forward, there will be more worries about the rupee plummeting and that could be a source of concern going forward.

The inflation targeting regime served us well and it is important that RBI continue to emphasise that it will keep inflation within those bands. Occasionally, it may go outside because of some disruption but it should come back within the band in a reasonable time. That will give RBI more flexibility to do what it needs to do on the liquidity side like supporting various forms of lending, even government debt. I would not disrupt this by saying we should be targeting inflation or move to something else. It has actually served us quite well and lets recognise that rather than have a whole set of dialogues, which take us nowhere.

Srinath Sridharan: Couple of years ago you were not too ready to recognise cryptocurrency as a formal currency, but as a Professor of Finance what would your view be, not just on cryptocurrencies, but more about block trading and banking technologies that have emerged. Do you think it is safer to bring them to mainstream finance?

Rajan: We have just come out with a report for the Group of 30, titled, ‘Central Bank Digital Currencies & Stable Coins’, which addresses some of these issues. It actually released on August 4. I have always been of the view that financial innovation should not be shut down. We should allow it to emerge and in some ways we should experiment in a contained fashion. The mistake is to either shut it down or to let it flourish without any control or regulatory structures monitoring it as it could become too big and then you recognise there are lots of problems. So, contained experiment has always been my view.

When cryptocurrencies initially came out, there was more of a wave in favour of them. RBI, in my time, said be careful, but did not ban cryptocurrencies at that point. Going forward, the Chinese central bank is going to come out with a digital currency. If other countries too come out with their own cryptocurrencies, we will have to explore a possibility of a rupee digital currency.

There are lots of problems with digital currencies, including the possibility of hacking and the question of information. The central bank gets the information of all transactions you make .On one hand that is good for tax authorities, but on the other hand that is bad for privacy. So, one needs to see what kind of structures are placed over and above the technology we put in place.

Also, the bigger question is should it be the central bank which issues the digital currency, or should you have a variety of private digital currencies. Can you have both like a hybrid currency -- many digital currency competing with each other and the central bank also issuing its own cryptocurrency? Should the central bank issue or should it, like in case of cash, issue to the banks and then let banks issue it to customers? It is time we can think about how we move in that direction.

What’s interesting is the reduction in transaction cost and the ability to use data effectively? There are possibilities created by cryptocurrencies and not all of them should have the same structure as Bitcoin. But we should learn from this experience and think of how we move forward.

Sridharan: The stock market has seen a huge run-up in the last many weeks. As the famous saying goes, the last one holding the bucket in the stock market is the retail investor. To correlate to the famous adage, ‘never waste a crisis’, what would your advice be if you had a friend as a retail investor?

Rajan: I would say that markets are generally quite efficient and that retail investors are the least informed. The best thing to do is to be reasonably well-diversified. A lot of easy money has already been made in the market. So, just for the fear of missing out, do not enter a party when it is going to end.

Make sure you are balanced between the different scenarios. You may believe there is a strong probability that the economy may come back. If you close to retirement, do not put all your money into the markets. There is some probability, it may not and things may be much worse.

If I was relatively young, I could take some more risk, but I would not put everything in the market because I could be left empty handed if it collapses. So, diversification across sectors and instruments is important. Don't be overly exposed to any single sector, no matter what the pundits say. Listen to what the big bull says, but recognise that he is in a different position than what you are.

Sridharan: We have a famous quote by a former regulator who said, “The regulatory body is independent and I have the approval of the government and the bureaucracy.” This statement it is so true as the concept of power has to be balanced with accountability. Times like these are unprecedented. What do you think the banking regulator can do better because whatever you do you are judged by what is not done?

Rajan: This is a time when you need to do a lot. It is also the time when you have to maintain stability by not being bold and boastful, which can create instability. So, if you are passive and may be doing what you have always done, you may not be reacting enough to the circumstances. It is a difficult situation as how do you convey the impression, the belief that it is doing prudent things. And that those prudent things have been thought through carefully enough, that they are actually quite beneficial and are the out of the box. How do you think out of the box while being conservative? That really is the challenge at this point because you don't want people to lose trust in the central bank and regulator. You also don't want the regulator to play the old play book. The old playbook, just went out of the window. The big question is how to create any new playbook in this environment.

Rajeev Poddar: Do you think the rate at which the currency is being printed by the central government will create serious side effects in medium to short term for a country like India? May be inflation might shoot up or the currency might weaken? People are saying that the cure might be worse than the disease. What is your opinion about the ‘Helicopter money’ which is going on all through the world?

Rajan: It is not actually money printing in all cases. What the central banks are doing is that they are issuing more reserves. It is not currency notes but the reserves which the banks are forced to hold. So, where does that money go? The central government is issuing those reserves to the bank. While issuing reserves its buying bonds, foreign exchange, etc.

When you look at the RBI, it is currently borrowing Rs 7 lakh crore from banks through the reverse repo window. Banks right now are reluctant to lend themselves. So, the central bank is acting as an intermediary between banks and whatever assets need to be held. That can happen as long as banks are not willing to lend. When the banks want to lend some more, when they feel there is some use for the money they are parking with the central bank, that’s when all the issues you raised become more frontal: there will be more credit growth and fear of inflation.

At that point of time, it is important that the central bank reverse what it does. Sell back some of the bonds in the market. That has to be managed very carefully and sometimes it can be very disruptive. But right now I would say that banks themselves are not willing to lend. There is still some room to do this.

Goyal: What does new economy mean for India where the demographics is young? Are we headed towards the new economy, with the new normal way of life?

Rajan: Certainly our young population gives one scope to do things differently. The pandemic has highlighted different ways of working. What it suggests that some of India's capabilities can be augmented through distance learning and done more effectively. The Kriya University that I am associated with has gone online over the last few quarters, which opens up a huge set of opportunities.

In India, let’s start by teaching students who are left out of the elite system. Can we start tele-meds as most health consultations have moved online? It will enable us if we can create a market for our services globally. We can leap frog the manufacturing stage, which we have not picked up. But we will still need manufacturing to create jobs.

Goyal: Two new normal habits you acquired or want to stick by?

Rajan: Peace and quiet and no travel.

Goyal: Any sports you like to play?

Rajan: I am a half marathoner. I have started playing tennis and also go for my run now. I want to travel a little bit for leisure.

Goyal: Two favourite books that resonate with you or ones you would suggest others read?

Rajan: I am reading older works on India. I have just finished Bipin Chandra and others on the freedom struggle. I have been reading Hillary Milton book, which was nominated for the Booker prize.

Goyal: Your favourite movies and music?

Rajan: My tastes are relatively eclectic. I am listening to old Hindi songs like that of Mukesh and Mohammad Rafi. On Netflix, I have been watching Ozark and The Good Fight with my children.

Goyal: You have worn so many hats. Which role is the most closest to you?

Rajan: I have been lucky to have not had any terrible experience in any role. I have enjoyed every role. At RBI, one of the most joyous things was that at the end of the day you felt you have moved the needle. You were relatively autonomous to do things on your own. You don't have to depend on permissions from elsewhere. There were a number of days when you went back home and you felt you really did something today. It is hard to beat that.

Anku Goyal is the founder of IndiaPodcasts.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.