Two non-convertible debentures (NCD) are set to hit the market on January 4. Mahindra & Mahindra Financial Services has come up with its first tranche of NCDs. Shriram Transport Finance has come up with its third tranche of NCDs. Should you invest?

What is it about?

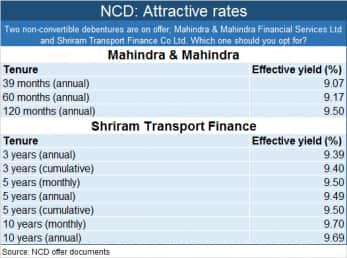

NCDs are fixed return instruments that aim to pay you a regular return on your instruments, either monthly, quarterly or annually. Mahindra Finance has four tenures; 39-month option, 60-month option (five years), 96-month option (eight years) and 120-month (10 years) option.

All these options will pay interest annually. Each NCD is available at a face value of Rs 1,000. The minimum investment is 10 NCDs or Rs 10,000 (10 NCDs x Rs 1,000).

Shriram Transport Finance has three options broadly; monthly, annual and cumulative that come with an effective yield of 9.39-9.7 percent and tenures of 3-10 years. Just like Mahindra Finance, the minimum investment here is Rs 10,000.

Both the NCDs are available only in dematerialised form. Mahindra Finance NCD will remain open from January 4 to 25th, while Shriram Transport Finance NCD opens on January 7 and closes on 31st.

Higher returns and good ratings

There are broadly three parameters that you should look at before buying an NCD. On top of this list should be its credit rating. Mahindra Finance NCD comes with a credit rating of AAA by rating agency Care, which indicates highest safety. Care classifies AAA-rated instruments as those that ‘considered to have the highest degree of safety regarding timely servicing of financial obligations. Such instruments carry lowest credit risk.’

Shriram Transport’s NCD comes with a slightly lower credit rating of ‘AA+/Stable’ by rating agency Crisil. This indicates that the instrument ‘have high degree of safety regarding timely servicing of financial obligations. Such instruments carry very low credit risk’, according to Crisil’s website that elaborates what each of its ratings mean.

A high credit rating in an NCD helps as it indicates the credit rating firm’s comfort in the company’s ability pay timely interests. Since investors who invest in NCDs are those who want regular and assured income, it helps if the company is able to honour its interest commitments.

According to Shriram Transport Finance NCD’s offer document, its credit rating for this issue is the same as that of the NCDs it came out with in the past three years; ‘AA+/Stable’. Infact, its rating has gone up slightly since its NCD that it had offered in the year of 2015.

Returns on both these NCDs are attractive. Shriram Transport Finance offers higher interest rates of the two NCDs on account of its lower credit rating. Typically, lower the credit rating of an instrument, higher its need to pay a higher interest to compensate investors for that extra risk taken.

For the 5-year NCD, Mahindra Finance offers 9.17 percent whereas Shriram offers 9.49 percent, both for their annual interest paying options. For the 10-year option, Mahindra Finance offers 9.50 percent, while Shriram offers 9.69 percent.

These rates are higher than bank fixed deposits of similar tenures. As per BankBazaar, the best interest rate offered by a bank on its term deposit for ‘5 years and above’ is 8.51 percent.

State Bank of India’s term deposit of a similar tenure offers an interest rate of 7.03 percent. To that extent, the NCDs offer 2 percent points more in terms of the yield that investors can earn.

Can they pay timely interest?

The biggest concern with any fixed income earning instrument is the company's ability to pay interests regularly and timely. An NBFC, like a bank, borrows and lends money. The biggest threat to meeting its commitments depends on how efficiently it can recover its dues from its borrowers. Hence, it’s important to understand the company's business model and whether it is capable of paying its loans on time.

Mahindra Finance lends money largely to people who wish to buy new and pre-owned cars, tractors and even commercial vehicles. Shriram largely lends money to transport firms that need money to buy commercial vehicles, like trucks. To that extent, since Shriram lends money to road transport operators, the borrower profile of Mahindra Finance works out to be slightly better.

Since any corporate firm is likely to have many borrowers, it helps if your NCDs are secured. A secured instrument ensures that lenders like you, the NCD investor, are ahead in the queue should the company face liquidation of its assets. Mahindra Finance’s 39-month, 60-month and 96-month NCDs are secured. The 120-month (10-year) instrument is an unsecured one. All of Shriram Transport Finance’s NCDs are secured.

What should you do?

Unless a debt instrument comes with a government guarantee, it doesn’t make sense to lock your money with a company for a very long time, say 8-10 years. Avoid the 8-year and 10-year options of, both, Shriram and Mahindra Finance. Further, the 10-year Mahindra Finance NCD is also an ‘unsecured’ instrument; the only one in this lot.

Although the difference in yield between its 5-year and 10-year NCD is hardly 0.33 percent points, sources say Mahindra Finance has offered “a far higher brokerage” to distributors for the 10-year option.

“The 10-year NCD is offering us 1% brokerage, the 5-year NCD is offering us 0.33% brokerage,” says a Mumbai-based distributor who did not want to be quoted. That’s one more reason to avoid the 10-year Mahindra Finance NCD.

Says Ashish Shah, founder of Wealth First: “The 5-year option of Mahindra Finance is decent. It’s not short-term and not very long-term.”

Given that interest rates are expected to fall this year and the attractive NCD interest rates, you can afford to lock your money for a 5-year time periods.

Therefore, avoid the 3-year NCDs. Mahindra Finance’s returns are only slightly lower than Shriram Transport Finance’s 5-year NCD, but the former’s credit rating is better.

Bottom line: Opt for the 5-year option of Mahindra Finance NCD.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.