Krishna Karwa

Moneycontrol Research

Highlights:

- Product mix moving towards premium variants

- Network expansion, marketing to bolster visibility

- Competition, input costs could impact margin

- We prefer Relaxo Footwears, Sreeleathers

--------------------------------------------------

Why branded footwear?

Growth in retailing, quality consciousness and higher disposable incomes are likely to provide a stimulus to branded footwear companies (BFCs). The industry is transitioning towards fashion, comfort and performance as against just being a basic need.

Product innovation, improved styling and creative marketing campaigns are among the added levers that should help BFCs achieve a better recall among masses. The right sales mix (volume versus value-based), coupled with periodic product launches, will strengthen their positioning further.

To expand into new geographies, a multi-channel brick-and-mortar presence (across large format stores, exclusive brand outlets, multi-brand outlets) is pivotal for all BFCs. To keep capex low, majority of the new stores will be franchise-run. Simultaneously, BFCs are developing their own websites and mobile applications, besides entering into tie-ups with e-commerce majors.

However, the ability to manage margin pressure associated with stiff competition and increasing commodity prices (rubber, leather, crude-linked materials) will differentiate the men from the boys.

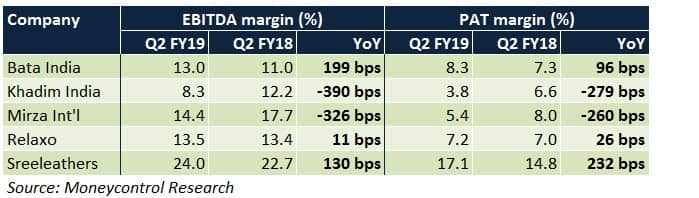

Q2 FY19 showed divergent margin performance

The improved topline performance of BFCs was attributable to branded premium products (for Bata India and Mirza International) and volume growth (for Khadim India, Relaxo Footwears and Sreeleathers).

While the likes of Bata, Relaxo and Sreeleathers succeeded in achieving cost efficiencies, Khadim and Mirza’s operating margins predominantly bore the brunt of higher input costs.

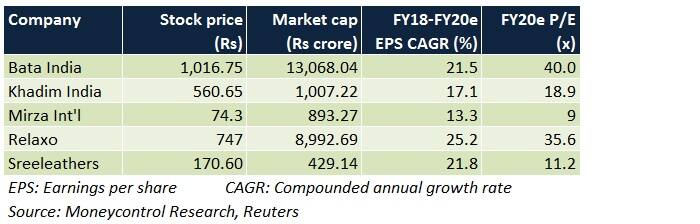

The stocks we are bullish on

Why Relaxo Footwears?

For the company, volume-based sales growth and mid-range products will remain the focus area. To expand reach, markets in western and southern India are being explored. New products like ‘Hawai’ flip-flops will be launched in H2 FY19. Cost rationalisation drives are underway as well.

Given the company’s strong brand appeal, leadership in the value footwear market and robust financials, its rich valuations are likely to sustain. The stock’s downtrend in recent times provides a good buying opportunity.

Why Sreeleathers?

The company has been reporting industry-leading margins and is expanding its footprints through store additions in northern and north-western India. It has managed to maintain costs across different time periods too and has negligible debt in the books. Lastly, the stock trades at undemanding valuations.

Why about the rest?

Bata India

The company is taking a number of initiatives like store renovations, experience centres and celebrity programmes to attract more footfalls. Around 100-150 new retail outlets will be opened each year. Impetus towards high-margin premium products will continue. Renegotiation of rent agreements and improved stock management processes should save costs.

Albeit these positives, the stock’s sharp rally in the past 20 days limits the scope for a noticeable re-rating, at least in the near future.

Khadim India

For the company, festive season traction in H2 FY19 is a key positive. The company plans to repay more debt from its IPO (initial public offer) proceeds. However, weak pricing power, drop in footfalls and lack of scale are its big challenges. A dip in the stock’s price in the coming months may provide a better entry opportunity for the long term.

Mirza InternationalPopularity of its Red Tape brand and foray into new categories (women, sports, canvas) in India are important drivers of future growth for the company. However, exports (primarily to the UK) aren’t likely to recover soon. Inventory build-up is anticipated to cause some working capital strain. The stock may, therefore, be avoided for now.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.