Even as the International Monetary Fund (IMF) cuts world economic growth projections for the current year, the US-China trade war has intensified weakening prospects for global steel demand. Steel prices have corrected sharply on account of the fall in steel demand globally.

However, Tata Steel faced little impact of the happenings in the steel sector. Despite these issues hurting sentiment, Tata Steel, during the June quarter, recorded 11 percent year-on-year growth in group revenue. This was largely on account of strong performance from its India operation, which accounts for close to 60 percent of total revenue.

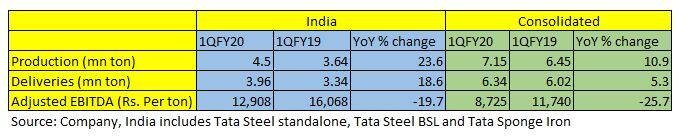

Its India operation reported 19 percent growth in sales volumes largely due to strong demand in the long products category. This provided some cushion from falling volumes in Europe.

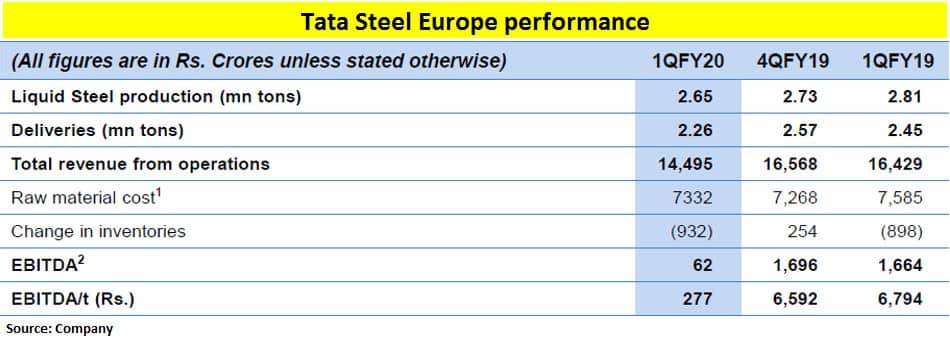

Europe, which contributes about 40 percent to consolidated sales, saw a 7.8 percent drop in sales volumes because of low demand and planned production shutdown. Consolidated volume growth was 5.3 percent.

Nevertheless, lower steel prices had an impact and benefits of higher volumes were reduced to that extent. For instance, Chinese HRC export prices, which stood around $625 a tonne last year, have dropped to around $500 in Q1 FY20.

Due to lower realisation, consolidated revenue grew a modest 1.3 percent to Rs 35,947 crore during the quarter under review.

Operating performance

While the performance at the revenue level was still reasonable, the impact of higher cost, due to higher iron ore and coking coal prices, impacted the company’s operating performance.

In the standalone business, which has integrated operations, raw material cost as a percent of sales moved up marginally (260 basis points) on a year- on-year basis. At the consolidated level, the impact was 586 bps, largely because of Europe and other entities (recently acquired assets).

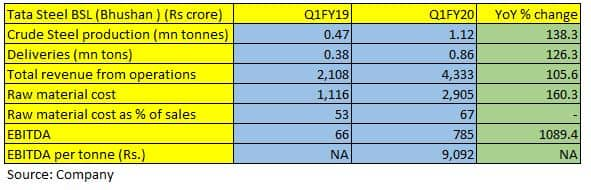

For instance, Tata Steel BSL’s (Bhushan) raw material cost, as a percent of sales, jumped to 67 percent in Q1 FY20 from 53 percent in Q1 FY19. This despite an over 100 percent jump in sales turnover to Rs 4,333 crore in Q1 FY20.

Operational parameters

The same was is reflected in the EBITDA-level performance. At the consolidated level, EBITDA dropped 26 percent to Rs 8,725 per tonne. European business saw a steep decline to Rs 277 a tonne in Q1 FY20 from Rs 6,794 per tonne in the same period last year.

Lower realisations, due to falling steel prices and higher cost, led to this poor performance at the operating level. This also impacted net profits. Largely because of a steep drop in European profitability, consolidated net profit dropped 64 percent YoY to Rs 702 crore in Q1.

Valuation and outlookSteel prices are expected to remain subdued in the near term and pressure is increasing on account of higher raw material. These issues and lower demand, particularly during monsoons, would reflect in Q2 FY20.

Moreover, with fresh hiccups in divesting its South Asian business and European operations as well as high debt on its books as a result of the acquisition of Bhushan Steel and Usha Martin, we remain cautious on the counter in the near term.

In an uncertain environment, managing debt and monetising assets could face difficulty, particularly if there is a longer-than-expected slowdown in demand and decline in steel prices.

At the current market price of Rs 382 per share, the stock is trading at 5.4 times its FY20 consensus estimated enterprise value (EV)-to-EBITDA and 5.3 times its estimated FY21 EV/ EBITDA.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.