With the automobile sector on a secular growth path and uptick in industrial segment, the bearing sector, which caters primarily to these two segments, seems to be in a sweet-spot. Improvement in technology also make this space worth considering as this is expected to increase content per vehicle and strengthening financials of companies. While the overall sector looks interesting from a growth versus valuation standpoint, we like SNL Bearings (SNL), Menon Bearings (MBL) and NRB Bearings (NRB).

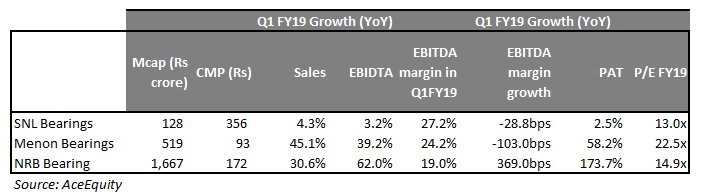

SNL Bearings We had initiated coverage on SNL, a needle bearings manufacturer that caters to automotive, original equipment manufacturers (OEM) and aftermarket segment. It posted a 4.3 percent year-on-year (YoY) growth in topline and 3.2 percent growth in earnings before interest depreciation and tax (EBITDA). Despite posting flat growth, EBITDA continues to be the highest among industry players. EBITDA margin was almost flat YoY. We continue to have confidence in the company on the back of strong opportunities for the industry and robust financials. The stock is trading at a significant discount compared to its peers.

Menon Bearings MBL is a manufacturer of bi-metal engine bearings, bushes and thrust washers for light and heavy automobile engines, two-wheeler engines as well as compressors for refrigerators, air conditioners etc. It posted a strong set of earnings on robust growth in the commercial vehicle segment.

It declared a 45.1 percent growth in net revenue on increase in wallet share from major OEMs and 16 percent growth in exports. EBITDA margin was however marred by rise in raw material prices (contraction of 103 bps), although part of the decline was countered by reduction in employee cost (down 297 bps) and operating and manufacturing expenses (down 107 bps).

EBITDA margin stood at 24.2 percent, the second highest among all players. Profit after tax rose 58.2 percent. It planned to increase its bearings capacity by 30-35 percent over the next one year to meet rising demand from the commercial vehicle segment. This coupled with strong financials and reasonable valuations beckon investor attention.

NRB Bearings (NRB) NRB is the largest manufacturer of needle roller bearings in India, with segmental market share of around 70 percent. It continues to declare a strong set of numbers on the back on industry tailwinds and operating leverage. Net operating income grew 30.6 percent led by two-wheeler and commercial vehicle (CV) demand, though after sales market continues to remain muted.

EBITDA grew 62 percent and margin expanded 369 basis points on operating leverage and favourable product mix towards CVs. Strong operating performance, higher other income and fall in interest cost led the company to report 173.7 percent growth in PAT.

Presence in the entire automobile spectrum, expectations of robust growth, and target of increasing market share in aftermarket provides us comfort in the company. However, muted demand in CV due to new axle norms is expected to limit near term growth. The stock is trading at reasonable valuations.

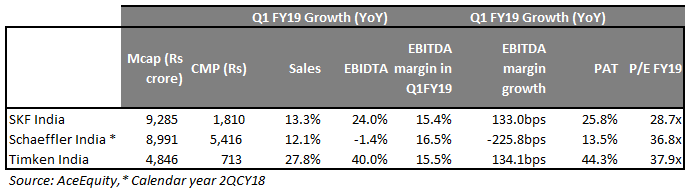

SKF IndiaThe company reported a 13.3 percent growth in net sales on favourable mix within the automobile segment. Auto segment grew 21 percent led by a 29 percent and 14 percent growth accruing from the aftermarket and industrial segments, respectively. EBITDA grew 24 percent, EBITDA margin expanded 133 bps and margin stood at 15.4 percent. The latter was lower due to lower contribution from traded goods.

The management said industrial sales were impacted during the quarter gone by on poor sales from wind. It expects the same to grow from July. The company’s plants are running at close to 100 percent utilisation and has guided at Rs 100 crore capex in FY19 to meet this demand.

In terms of valuation, the stock trades at 28.7 times FY19 earnings, which is above our comfort level.

Schaeffler IndiaNet sales grew 12.1 percent due to 36 percent and 14 percent growth from domestic automotive original equipment and industrial segments, respectively. Exports fell 18 percent on a YoY basis. On a pro-forma basis, the combined entity (includes LuK India and INA Bearings), grew 15 percent driven by INA Bearings which saw a 28 percent growth in revenue.

The company posted a 225 bps contraction in EBITDA margin due to increase in lower margin product contribution, which grew to 37 percent from 28 percent of revenue. The 4 percent price hike was across all products, effective April 1, and would be visible in Q3 CY18.

Given the strong growth in industrial and automotive segment, strong product portfolio and addition of new products, capacity expansion plans and completion of merger with LuK and INA, the stock deserves attention. The stock is currently trading at 36.8 times FY19 earning, the second highest among all players.

Timken IndiaTimken India is a market leader in tapered roller bearings and is the only indigenous manufacturer of freight application bearings for railways.

It posted a 27.8 percent and 40 percent YoY growth in net sales and EBITDA, respectively. Despite a significant rise in raw material price, EBITDA margin expanded 134 bps. This was due to significant reduction in operating expense, owing to operating leverage. The company is currently trading at a very expensive valuation – the highest among all players - which leaves us cold.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.