Ruchi AgrawalMoneycontrol Research

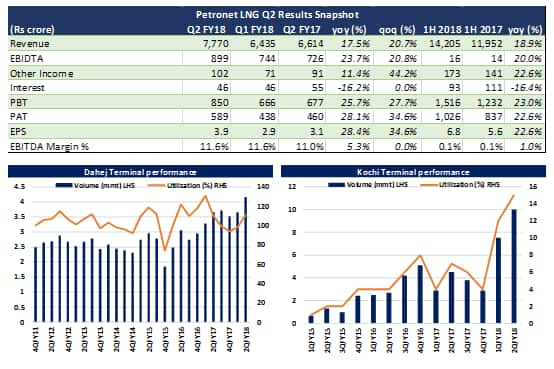

Petronet LNG (PLNG) reported a stellar performance in Q2FY18 mainly on account of an uptick in volumes. Revenues stood at Rs 7770 crore -- a 17.5 percent increase YoY (year-on-year) and 20.7 percent sequentially. EBITDA at Rs 899 crore and PAT at Rs 589 crore, grew 23.7 percent and 28.1 percent YoY respectively with a substantial margin expansion. EBITDA margins were up 5.3 percent YoY while PAT margins expanded 9.1 percent. Uptick in PAT was further supported by high other income component.

The company reported the highest ever total volumes at 220 trillion British thermal units (tbtu), an increase of 15 percent from Q1FY18, mainly on account of sequential recovery in off-take from fertiliser plants. PLNG enjoyed a better operating leverage due to higher capacity utilization of the Dahej terminal and marginally higher utilization at Kochi as well.

Dahej – utilization ramp-up

During the quarter, the Dahej terminal operated at 110 percent utilization with long-term volumes at 127 tbtu, up 23.3 percent YoY and 21.2 percent QoQ. Spot volumes were at 4 tbtu and re-gas volumes at 79 tbtu.

Higher volumes led to higher PLNG profitability with efficiency gains and margin improvement. The off-take at Dahej was boosted by a sharp spike in power demand due to coal shortages and unavailability of Dabhol terminal during the monsoon period.

The Dahej terminal capacity expansion from current 15 mmtpa to 17.5 mmtpa is going as per schedule and is expected to get completed by Q4FY19 post which there would be some further volume expansion.

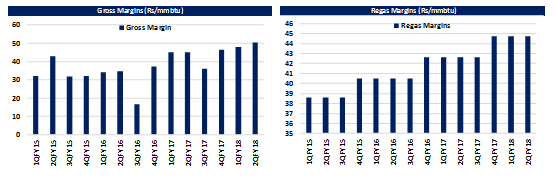

The margins remained steady during the quarter with overall margins ramping up 5 percent YoY at Rs 50.3 per mmbtu and Regas margins at Rs 44.7 per mmbtu.

Kochi on track

The Kochi terminal utilization was up from 11.5 percent to 15.4 percent sequentially mainly due to continuous off-take from the BPCL’s Kochi refinery. The management expects utilization levels to remain low for coming few quarters until December 2018, when the full commissioning of the terminal is planned, post which there is an expectation of rapid uptick in utilization levels.

There has been retaliation by locals against the Kochi-Mangalore pipeline construction. However, the company believes that with government’s support the commissioning is on track and would be completed as per scheduled.

International expansion on cards

The company is in advanced discussions with Bangladesh and Sri Lanka governments to set up regasification units and expand its presence internationally. While timelines are not clear, this will help PLNG maintain its future growth momentum and utilise surplus cash.

The PLNG stock is currently trading at FY19 PE of 17x and an EV/EBITDA of 10 which is much in line with the industry average. The stock has rallied 43 percent since the beginning of the year and 2 percent since the announcement of the Q2 results. With continued shortage of LNG domestically and capacity expansion that should support Petronet’s volume in the future, we see the stock as a steady long-term performer.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.