Krishna Karwa Moneycontrol Research

Symphony is one of India’s leading residential and industrial air cooler brands, with the former accounting for nearly 80-90 percent of annual sales. The company, through its earlier acquisitions in Mexico (IMPCO) and China (Munters Keruilai), has managed to strengthen its presence in international markets as well.

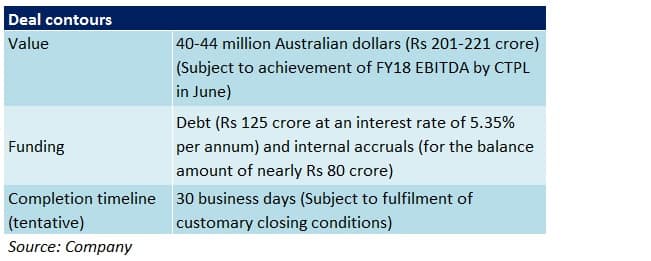

For better access to overseas markets and technology, the company recently acquired 95 percent stake in Climate Technologies Pty (CTPL). The Adelaide-based company is a manufacturer of evaporative air coolers, ducted gas heaters and other cooling products. It caters to clients in Australia and the US.

How does Symphony benefit?

A ‘hot’ market: Australia is characterised by dry, hot and humid climatic conditions for most part of the year. Like India, demand for its cooling products is expected to remain robust, thus ensuring adequate revenue visibility in the long run.

Access to brands: With iconic brands such as ‘Bonaire’ and ‘Celair’ in its kitty for at least four decades, CTPL is one of the most renowned cooling and heating appliance players. Its market share in Australia’s evaporative air coolers/ducted gas heaters market stands at 30/25 percent, respectively.

Tapping the US market: CTPL has a tie-up with Home Depot, an American home improvement retailer, and a product assembly centre in the US. Purchase of stake in CTPL will complement IMPCO’s partnerships with America’s large format stores. The US also happens to be the largest air cooler market in the world.

Diversification: Symphony will be better positioned to mitigate risks from subdued demand in India in seasonally weak quarters (winter months in particular) by laying impetus on the Australian market (summer is typically at its peak from October to March).

Product synergy: Adoption of newer technologies (evaporative air coolers) should help the company capitalise on its already strong innovation track record, eventually giving it an edge over domestic and foreign competitors.

Business similarities: Like Symphony, CTPL has strong relationships with clients (40 builders and 50 premier dealers in Australia), follows an asset-light model, commands a high market share in core markets and has been at the forefront of innovation.

Distribution: Symphony’s investment in CTPL should enable the former to achieve a higher degree of brand visibility as far as its new products (post-CTPL acquisition) are concerned. Symphony’s existing international distribution network spans over 60 nations worldwide.

Debt free: About Rs 80 crore of the total acquisition amount of Rs 200 crore will be funded through borrowings. Symphony’s management remains confident about CTPL’s cash flow generation ability from its Australian operations. Therefore, debt repayment won’t be an issue.

Should one invest?

Symphony remains in a promising space given its growing emphasis on industrial and centralised air cooling, apart from sales traction in its 2 air cooler brands – Diamond and Sense – that were launched by the company in H2 FY18.

Steps taken to turnaround IMPCO and Munters Keruilai have been yielding positive results. The former has gradually turned EBITDA positive in 2018, whereas the latter has seen a substantial reduction in losses in the last 2-3 years.

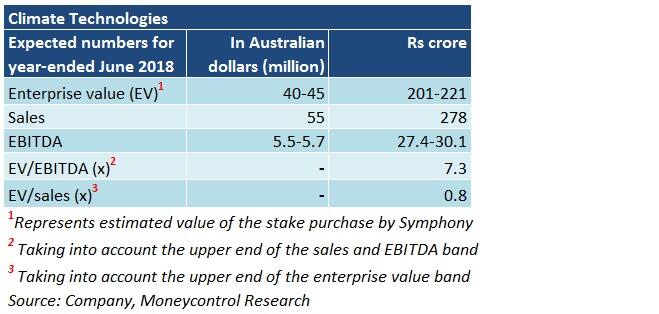

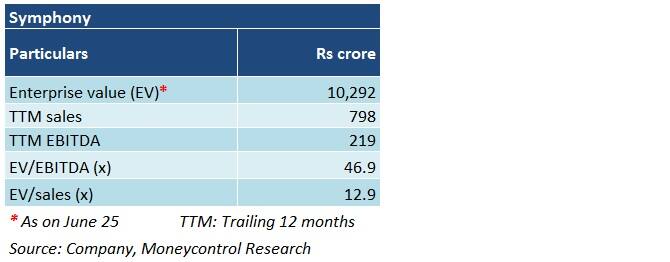

Financially, the deal with CTPL makes sense for Symphony. Integration of CTPL’s business with the company will be sales and earnings accretive (due to bulk raw material sourcing and economies of scale) from the start, thus yielding higher returns on capital (potentially more than 20 percent).

Symphony’s funds in its treasury investments generate returns of 7-7.5 percent, which will pretty comprehensively offset the marginal interest cost of 5.5 percent on the borrowed amount. Prima facie, the value of CTPL’s acquisition doesn’t appear steep.

However, in Q1 FY19, consumer demand was disrupted owing to unseasonal rains in north and north-western India (among Symphony’s prime markets). This, in turn, could lead to a lower-than-anticipated set of numbers for the June quarter.

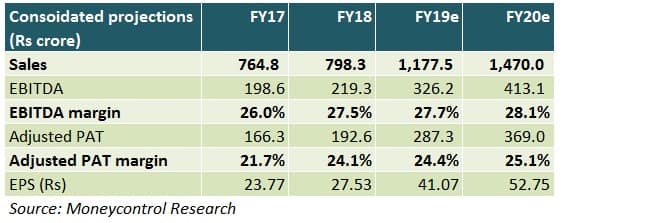

Nonetheless, at 27.8 times FY20 projected earnings, we remain confident about Symphony’s long term prospects. Healthy fundamentals and successful inclusion of a profit-making entity (CTPL) at an undemanding consideration should bolster the company’s top-line and profitability.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.