Anubhav Sahu

Moneycontrol research

Fourth quarter results from Balaji Amines and Alkyl Amines indicate improving end markets and better realisations, amid challenges of higher raw material costs. A mix of backward and forward integration will help both companies maintain their near term profit margins. Alkyl Amines benefited from new capacity in methylamines - the building block for various value-added derivatives, and Balaji Amines is focusing on a range of products which are mostly imported at present.

Quarterly snapshot: Sequential impact of higher raw material cost for Balaji Amines

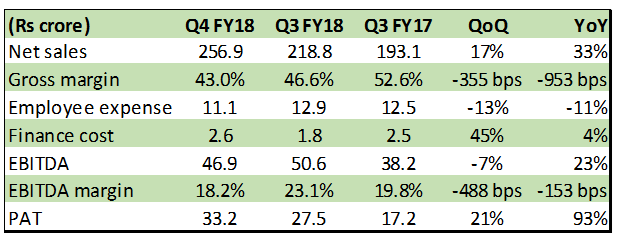

Balaji Amines’s sales grew 33 percent year-on-year (YoY), led by the amines division (98 percent of sales) and about 10 percent YoY volume growth. Compared to the preceding quarter, sales rose 17 percent.

Operating profit (EBITDA) margin fell 153 basis points (bps) as raw material prices surged 66 percent YoY. The drop was partly cushioned by a moderate increase in other expenses (20.5 percent of net sales versus 26.3 percent of net sales in Q4 FY17) and lower employee costs.

Margins were hurt also by a sharp rise in contracted methanol prices and a lag (2-3 weeks) in passing on higher costs to customers. Quarter-on-quarter, higher raw material costs dented EBITDA margin even more sharply. Also, shutdown of a plant for a week impacted operating performance.

Net profit got a leg up from lower tax of around 16 percent (versus 46 percent in Q4 FY17) after the recent amalgamation of Balaji Greentech and Bhagyanagar Chemicals.

Alkyl Amines reported a 33 percent YoY growth (14 percent QoQ) in sales aided by double-digit volume growth. In contrast to Balaji Amines, EBITDA margin improved to 48.1 percent (379 bps QoQ) on better gross margins and decrease in other expenses.

Balaji Amines result snapshot

Source: company

Alkyl Amines result snapshot

Source: company

Capacity expansion on the anvil

Alkyl Amine’s Dahej facility was commissioned in Q4 FY18, boosting its methylamine capacity to 33,000 metric tonne (MT). The plant is expected to operate at a utilisation rate of 70 percent by FY19-end. This saves some cost due to proximity to major raw materials sources. Also, its current methylamine capacity (15,000 MT) in Patalganga may now be used for higher margin derivative products. The management plans to increase acetonitrile capacity from 10,000 MT to 30,000 MT.

Balaji Amines continues to wait for a no objection certificate (NOC) from the government to kick-start its acetonitrile and morpholine plants. These, along with the new facility for dimethylamine hydrochloride (DMA HCL), is expected to turn operational in the next 1-2 months. DMA HCL is used as a pharma ingredient for ranitidine and metformin (diabetic drug) and has a production capacity of about 25,000 MT.

The management expects Rs 150 crore in revenue addition in FY19 due to the above initiatives as new capacities would be operating at about 50-60 percent utilisation in the first year.

Other expansion and acquisition projects

Balaji Amines’ investment (55 percent stake, Rs 66 crore) in Balaji Speciality Chemicals provides it exposure to specialty chemicals like ethylene diamine (18,000 MT), piperazine (4,000 MT) and diethylenetriamine (DETA) that have applications in agri-end markets, fuel additives, rubber additives and pharmaceutical industry. Operations are expected to start in October with revenue of about Rs 100 crore expected in FY19.

Work on the greenfield mega project in Solapur (capex outlay of around Rs 300 crore) is expected to start by October and contribute to revenue from FY20 onwards.

The management is now focusing on monoisopropyl amine (15,000 MT), isopropylamine (50,000 MT) and additional capacities for methylamine and ethylamine. At present, there is heavy import dependency in India for monoisopropyl amine and isopropylamine. Anti-dumping duty imposed on monoisopropyl amine in March aided pricing. In Phase II of expansion, the company plans to look at products like methyl isobutyl ketone (MIBK) and diphenylamine.

Anti-dumping duty triggers positive for Balaji Amines

Due to the anti-dumping duty on dimethylacetamide (DMAC, 6,000 MT capacity), capacity utilisation improved and went past 70 percent. The management said margins have normalised.

In case of dimethyl formaldehyde (DMF), anti-dumping investigation is ongoing and the company expects a clarification in June. Balaji Amines has an installed capacity of 30,000 MT and utilisation rate can ramp-up from sub-30 percent levels on the back of a favourable decision.

Stock price to move in tandem with earnings growth

Based on near-term capacity expansion plans, improving end markets, product pricing scenario and expanding product portfolio both Balaji Amines (16.3 times FY19e earnings) and Alkyl Amines (17.5 times FY19e earnings) are well placed for growth in the near duopoly market. While both companies benefit from enriched technical knowhow, we are enthused by the promptness and flexibility shown by amine companies on their capex plans with regard to changing market conditions. Based on all the above factors, the recent correction in their stock prices provides an opportunity to enter, in our view.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.

Bill, 2025: India’s attempt at third generation power reforms")