In January, so far, Sensex has risen around half a percent. But broader markets are still lagging frontliners with the BSE Midcap index falling 1.6 percent and Smallcap index down a third of a percent.

In comparison, Sensex gained 6 percent in 2018. BSE Midcap index fell 13.5 percent and Smallcap index was down 24 percent in 2018.

Overall, especially after the run in November, the market has been rangebound and stock-specific action has continued, which is likely to be the top theme in the rest of 2019 as well.

Most experts feel the volatility will continue in the first half of 2019, so it is better to go with stock-specific action rather than looking at index return.

"We believe that the first half may be muted on account of upcoming elections. However, if a stable, reform-oriented government were to assume power, that would be a positive trigger for equities, which we believe will be the case. Thus, the first half may be a good time for investors to buy stocks," Vivek Ranjan Misra, Head of Fundamental Research at Karvy Stock Broking told Moneycontrol.

Even after the recent recovery, the market is still down 7 percent from its peak hit in August 2018 and broader markets are far away from their historic highs but that gives analyst an opportunity to pick good quality stocks at right time.

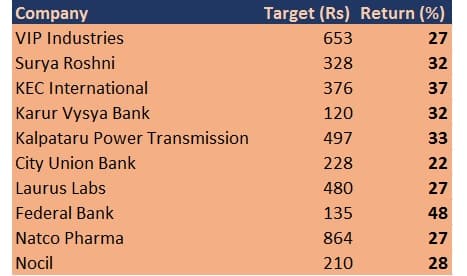

Here is the list of top 10 stocks where analysts initiated coverage with buy call and are expected to return 20-50%:

VIP Industries is India's leading luggage brand (around 55 percent organised share), #1 player (value terms) in backpacks and making inroads into ladies handbags (less than 2 percent share, $1 billion market).

Distribution architecture, product quality and brand segmentation across price points drove 25 percent EBITDA CAGR over FY14-18. Experienced team investing in brand and now own capacities (Bangladesh) should drive 24 percent revenue CAGR over FY18-23.

Despite currency volatility and rising procurement costs, 29 percent EPS CAGR over FY18-23 should be led by 1) 24 percent revenue CAGR from rising contribution of backpacks/handbags and 2) EBITDA margin improving to 16.9 percent (versus 13.7 percent) led by captive production, premimumisation and operating leverage.

We initiate coverage with buy call and target price of Rs 653 is built on high-teen revenue growth over the next decade as penetration and brand salience rise. Risks are management attrition and market share loss in economy segment.

Brokerage: Kotak Securities | Stock: Surya Roshni | Target: Rs 328 | Return: 32%We initiate coverage on Surya Roshni (SURL) with buy rating and a target price of Rs 328 based on SOTP (Sum of the parts) valuation methodology.

We believe that SURL valuations can get rerated on back of 1) potential demerger of company’s consumer electrical and steel pipes business 2) strong growth in company’s estimated consolidated profits through FY18-20E driven by a) meaningful growth in fans & consumer appliance segments supported by improved penetration on the current lower base b) stability in LED prices c) recovery in the pipes business driven by improved public spending in infrastructure.

We project 18.7 percent CAGR between FY18-20 in consolidated profits from Rs 108 crore in FY18 to Rs 150 crore in FY20E, expect improved return ratios and balance sheet strengthening-building a case for stock re-rating.

Brokerage: Karvy Stock Broking | Stock: KEC International | Target: Rs 376 | Return: 37%With the growth imperatives in international and domestic T&D sector along with huge potential in other infrastructure sectors like railways and civil, we initiate a coverage with buy rating for a target price on KEC (Rs 376).

The revenues are expected to grow at 16 percent CAGR during FY18-20E by execution of huge order book. The overseas T&D opportunities are strongly visible, also the non T&D business is gaining traction in the international markets.

The current order book of Rs 20,135 crore stands at 1.9x the revenues which provide a very strong revenue visibility of 16 percent CAGR during FY18-20E.

Brokerage: Karvy Stock Broking | Stock: Kalpataru Power Transmission | Target: Rs 497 | Return: 81%A very strong order book in T&D business and a very strong momentum of growth in Non T&D business would lead the revenues to grow at 15 percent CAGR during FY18-20E. The overseas T&D business is expected to grow on the back of strong orders from Africa, Middle East and SAARC nations.

Also Kalpataru is trying to gain traction in the international markets for its non T&D business. With subsidiaries going to perform strongly, it should support the cash flows for the company.

We arrive at a target price of Rs 497 for a buy rating.

Brokerage: JM Financial | Stock: Karur Vysya Bank | Target: Rs 120 | Return: 32%Karur Vysya Bank's track record of consistent profitability over the last 102 years and unbroken dividend payout is pretty commendable.

Reasons to be sanguine on KVB now is a new CEO at helm (completing over a year in office now), taking charge from a large MNC with a brilliant track record in retail banking, focus back to serve SME/Individuals which has always been its core strength, digitization of its product suite to ensure it remains competitive and relevant in the current data age and last but not the least with asset quality pain over, credit costs is expected to normalize leading to a bounce back in ROAs from 0.5 percent in FY17/18 to an estimated 1.2 percent in FY21E.

We initiate coverage on Karur Vysya Bank and assign a buy rating with a target price of Rs 120.

Brokerage: Axis Securities | Stock: City Union Bank | Target: Rs 228 | Return: 22%City Union Bank, over last few years, has witnessed relatively better and stable valuations owing to consistent return profile vis-a-vis midsized private bank peers.

We believe the bank with superior net interest margin, best return profile, grip on asset quality with greater bottomline visibility over the medium term should continue to fetch higher multiple.

We initiate buy with a target price at Rs 228 per share.

Brokerage: HDFC Securities | Stock: Laurus Labs | Target: Rs 480 | Return: 27%Laurus is likely to come out stronger as backward integration for the key molecule is already in place and the formulations business is about to be in the black with fresh orders.

With a likely initial tender win, Laurus is set to enter the $1.8 billion ARV formulations market in FY20. It can capture at least 15 percent market share (in 3 products), supported by one of the largest API capacities.

At FY21E formulations revenues/EBITDA of $85/25 million, earnings can triple over FY19-21E (on a soft base). Moreover, we expect a couple of big ticket formulations launches in the US market by FY21 which can further boost profitability. Initiate coverage with a buy rating and target price of Rs 480.

Brokerage: Centrum | Stock: Federal Bank | Target: Rs 135 | Return: 48%We initiate coverage on Federal Bank with a buy call and target price Rs 135. The bank is evolving to a more prolific private banking franchise on the back of its balance sheet size, quality growth trajectory, pan India expansion strategy, branch light-distribution heavy model, digital architecture and senior management pedigree.

Incremental flow to higher rated assets has maintained capital adequacy at healthy levels (CAR - 13.3 percent). Stressed asset ratio has substantially declined over FY14-Q2FY19 and we expect credit cost to recede.

All these levers will enhance return on assets / return on equity to by 41 bps / 520 bps over FY18-21 to 1.1 percent / 12.6 percent. Valuation looks attractive.

Brokerage: Arihant Capital Markets | Stock: Natco Pharma | Target: Rs 864 | Return: 27%Natco Pharma is a leading player in the oncology and the hepatitis C business in India and had successful product launches in USA led by prime molecules such as Tamiflu, Copaxone, Doxorubicin and Lanthanum.

Company has partnered with leading generic player which reduces company's litigation cost. A large untapped domestic market growing in mid-teens and US-driven international business with 29 ANDA’s in the pipeline and relatively lower risk of sharp pricing erosion puts Natco in a sweet spot among peers.

We expect Natco to report 14 percent CAGR in its revenue and PAT over FY18-20E. EBITDA margin is expected to stabilise at 40 percent. We are positive on the future prospects of Natco and initiate coverage on the stock with a Buy rating and a target price of Rs 864.

Brokerage: Anand Rathi | Stock: Nocil | Target: Rs 210 | Return: 28%Capacity expansions of tyre companies (demand side) and the doubling of Nocil’s production capacity (supply side) should keep volume growth steady for the company.

However, auto sector sales would determine OEM demand and, growth in the logistics sector, the tyre replacement market, and in turn utilisation of tyre-companies’ new capex. This would govern realisations of rubber chemicals.

Potential growth in this jamboree of binary events keeps us cautiously optimistic about Nocil. Nevertheless, we initiate coverage on it, with a buy rating, for a target price of Rs 210.

Risks are removal of the anti-dumping duty on Chinese rubber chemicals and tyres, reduction in the average selling price (ASP) of rubber chemicals.

Disclaimer: The above report is compiled from information available on public platforms. Moneycontrol advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.