The stock market rebounded strongly and reached a new all-time high in the last week of 2023, despite a minor setback the previous week. This was due to positive global cues, renewed buying by foreign institutional investors, easing of the Red Sea disruption, and rising expectations of rate cuts by the US Federal Reserve, which cooled down inflation. Additionally, there was anticipation of political stability in 2024, which further fueled the rally.

However, in the first week of 2024, the market may experience some consolidation due to the sharp upswing in the past few days. Nevertheless, the overall outlook remains bullish, and the focus will be on manufacturing and services PMI numbers globally, FOMC minutes, US unemployment data, and monthly auto sales.

In the week ended December 29, the Nifty 50 jumped 382 points or 1.8 percent to 21,731, and the BSE Sensex rallied 1,133 points or 1.6 percent to 72,240, taking the total the year gains to 20 & 19 percent respectively, while the broader markets - the Nifty Midcap and Smallcap 100 indices gained 2.4 percent and 2 percent during the week, and 47 percent and 55 percent during the year, respectively.

All the indices except technology closed in green, indicating a positive momentum in the market, driven by healthy macroeconomic conditions, strong inflow of foreign institutional investments, and positive global cues. Siddhartha Khemka, the head of retail research at Motilal Oswal Financial Services, predicts that the next week will be eventful with a series of economic data releases globally. He feels that the market will continue its ongoing positive momentum in the near term.

Vnod Nair, the head of research at Geojit Financial Services, shares this sentiment and predicts that the euphoria will continue at the start of the new year due to rate cuts and the drop in bond yields. He expects a modest return of 10 to 12 percent on the main market in CY24.

Here are 10 key factors to watch:

Auto Sales

The new year will start with the monthly auto sales data scheduled to be released by the original equipment manufacturers for December 2023. Hence, auto stocks will be in focus.

Most of experts expect the double-digit growth in two-wheeler sales, but flat-to-moderate growth in passenger, commercial vehicle and tractor segments on year basis.

Domestic Economic Data

Further, the S&P Global Manufacturing and Services PMI data for December will be released next week on January 3 and January 5, which most experts expect slightly below the levels seen in November at 56 and 56.9 levels, respectively.

Further, foreign exchange reserves for week ended December 29 will also be announced on January 5.

Also read: January has mostly been cold to investors in past 10 years. Can we see a change in 2024?

FOMC Minutes

Globally, all eyes will be on the FOMC minutes of the Federal Reserve meeting held in December 2023. The market participants will look for cues related to rate cuts expected to take place in 2024.

In the December meeting, the US Federal Reserve kept the fed funds rate unchanged at 5.25-5.50 percent for three meetings in a row, while hinting three rate cuts (total 75 bps) in 2024, given the falling inflation. Economic growth is estimated to be higher at 2.6 percent in 2023 against earlier projection of 2.1 percent, but lower at 1.4 percent for 2024 against earlier estimates of 1.5 percent.

Global Economic Data

Apart from FOMC minutes, global investors will also focus on manufacturing & services PMI numbers by developed nations. In addition, US unemployment rate (which is expected to increase a bit for December, from 3.7 percent reported in previous month), non-farm payrolls, and JOLTs job openings & quits will also be watched.

Oil Prices

The market participants will also keep an eye on oil prices, which fell sharply in November and remained rangebound in December. The weekly charts indicated that the oil prices seem to have formed a bottom for the time being, during December as the prices rebounded from around $72 a barrel levels and remained tad below 200-week EMA (exponential moving average). Further, even in the past months during the year, the prices many a times tested $70-72 a barrel but did not break the same.

Having stabilised below $80 a barrel is a major positive for oil importing countries like India, and hence, acted as a strong supportive factor for the equity markets because it reduces the fiscal pressure.

Brent crude futures, the international oil benchmark, dropped 2.2 percent during the past week to settle at $77.04 a barrel. For the year, the prices plunged 10.3 percent after sharp rise in the past two years.

"We expect oil prices to slide as supplies from the non-OPEC nations have been on rise in the past few months and US production is running near an all-time high of 13.3 mbpd. Production cuts by OPEC+ have proved insufficient to prop up prices, with the benchmarks declining nearly 20 percent from their highest level this year," Mohammed Imran – Research Analyst, Sharekhan by BNP Paribas said.

Foreign institutional investors increased buying interest significantly in the month of December to nearly Rs 32,000 crore, the biggest monthly buying since February 2021, while the domestic institutional investors picked Rs 12,900 crore worth shares during the same month. They both helped the market report record high and post 8 percent gains during the month. The fall in US 10 year bond yields to 3.8 percent from 4.9 percent in last two months following increasing expectations for fed funds rate cut in 2024 caused the surge in FII inflow.

But for the year 2023, FIIs were net sellers to the tune of Rs 13,200 crore, hugely underperforming DIIs who bought Rs 1,68,988 crore worth shares in the cash segment. Now in the year 2024, most of experts expect flow from both the desk (FIIs and DIIs) to increase significantly.

"Since 2024 is expected to witness further declines in US interest rates, FPIs are likely to increase their purchases in 2024 too, particularly in the early months of 2024 in the run up to the General elections," Dr V K Vijayakumar, chief investment strategist at Geojit Financial Services said.

On the primary market front, the coming week is going to be a quiet period for the mainboard segment. In the SME segment, there will be no new IPO launch but seven companies will make their debut on the bourses.

Sameera Agro and Infra will list its equity shares on January 1, and AIK Pipes & Polymers on January 2, while Akanksha Power & Infrastructure, HRH Next Services, Manoj Ceramic, and Shri Balaji Valve Components will be listing on January 3.

Further, Kay Cee Energy & Infra will be closing its IPO on January 2 and its equity shares will be listed on January 5, while the Kaushalya Logistics IPO will be closing on January 3.

Technical View

The Nifty 50 turned healthy after a week of correction and registered a strong bullish candlestick pattern on the weekly scale. Further, the index hit a new milestone of 21,800 during the week, though saw some profit-taking on Friday. Higher highs and higher lows formation continued for five weeks in a row, and higher lows continued for the ninth consecutive week, while momentum indicators RSI (relative strength index) and MACD (moving average convergence divergence) maintained positive bias.

Technically, given the smart rally in the past week, the market may prefer to consolidate for some more days, but after the said consolidation, the index is expected to leap the 21,800-22,000 zone in the coming weeks, with crucial 21,600-21,300 area as a support, experts said.

"Immediate support is observed around 21,600, followed by 21,500, while strong support lies around the week's low around the 21,300 mark," Rajesh Bhosale, technical analyst at Angel One said.

He feels although prices are in uncharted territory with no prominent resistance visible, 21,850 followed by 22,000 presents an immediate hurdle, considering the overbought conditions. Traders should monitor these levels and adjust their strategies accordingly, he advised.

F&O Cues & India VIX

Given the strong optimism in the market, options data indicated that the Nifty 50 is expected to face resistance at 21,800-22,000 levels in the near term and further may also aim for the 22,500-23,000 zone in the short-to-medium term, with a support zone of 21,700-21,500 in the near term and then 21,000 as crucial support.

As per the first weekly options data of the January series, 22,000 strikes enjoyed the maximum Call open interest, followed by 22,500, 21,800 and 23,000 strikes, with meaningful Call writing at 23,000 strikes, then 22,000, 22,500 & 21,800 strikes.

On the Put side, the maximum open interest was owned by the 21,500 strike, followed by the 21,000 strike and 21,700 strikes. The writing was observed at the 21,500 strike, then 21,700 strike and 21,200 strike.

Since the market started moving upwards in November, the volatility has been gradually increasing week after week, except for one week. This suggests that market participants are overly bullish on the Nifty 50. Therefore, some caution is warranted at these levels and some profit booking can't be ruled out in the near to short term, as per experts.

It is worth noting that the fear index, India VIX, climbed 5.8 percent during the last week to 14.50 levels. Since November, it has jumped 33 percent.

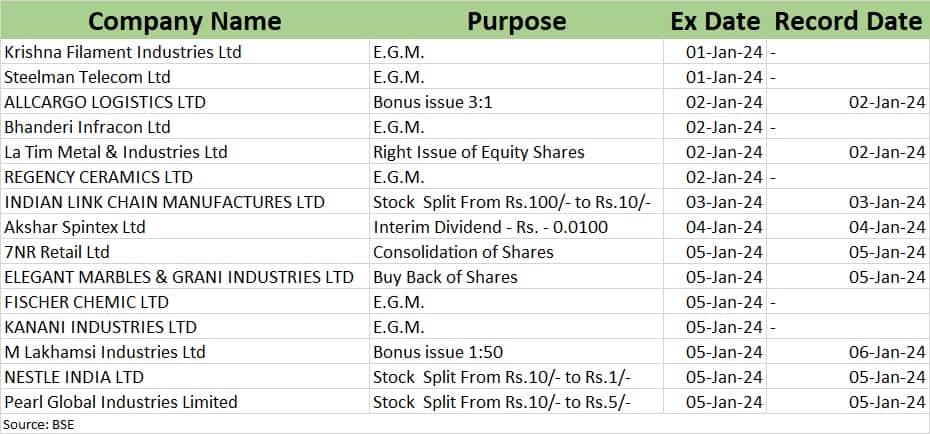

Corporate Action

Here are key corporate actions taking place in the coming week:

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.