during the week to 24,363, and the BSE Sensex fell 742 points (0.92 percent) to 79,858, while the Nifty Midcap and Smallcap 100 indices were down 1.1 percent and 1.4 percent, respectively.")

Bears staged a strong performance for the sixth consecutive week, the longest losing weekly streak since the Covid-led crisis in 2020, and pulled the benchmark indices down nearly 1 percent for the week ended August 8.

An additional 25 percent tariff on India imposed by Trump due to India buying and selling Russian oil, taking the total tariff to 50 percent (equal to Brazil) on the country, underwhelming quarterly earnings, and persistent FII selling weighed on the market sentiment. However, the RBI’s reaffirmation of macroeconomic stability with an optimistic stance on domestic growth capped the downside risks to some extent.

Overall, the ongoing bearish sentiment is expected to prevail in the coming holiday-shortened week, too, though there is a possibility of an initial rebound due to oversold conditions, according to experts. The focus will be on the India and US inflation numbers, further tariff-related developments, including the 90-day US-China trade truce deadline ending on August 12, the Trump-Putin meet, and the FII mood.

The Nifty 50 declined 202 points (0.82 percent) during the week to 24,363, and the BSE Sensex fell 742 points (0.92 percent) to 79,858, while the Nifty Midcap and Smallcap 100 indices were down 1.1 percent and 1.4 percent, respectively.

Looking ahead, "the market volatility is expected to persist. While risks from US trade tensions and sustained FII outflows remain, potential support from DIIs could offer some relief," Vinod Nair, Head of Research at Geojit Investments, said.

According to him, upcoming inflation data from both India and the US will be critical in shaping investor expectations. "Market participants are advised to closely track global trade developments and corporate earnings, with a strategic focus on domestic consumption-driven sectors that are better positioned to withstand short-term volatility," he said.

The market will remain shut on August 15 for Independence Day.

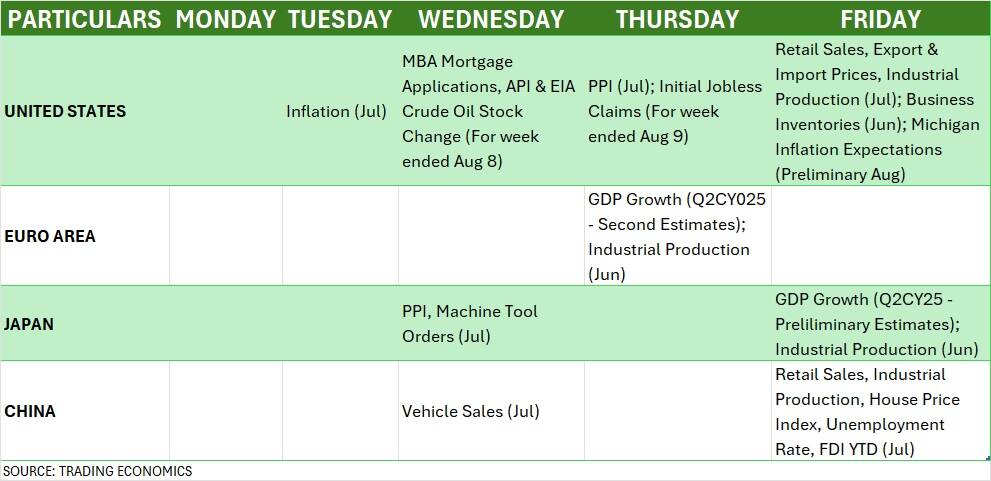

Here are 10 key factors to watch for this week:

Tariff-related developments and the Trump-Putin meeting

Market participants will be closely watching further tariff-related developments after the Trump administration imposed a 50 percent tariff on India. An initial 25 percent tariff was already implemented, effective August 7, and the additional 25 percent will take effect 21 days later. Before that deadline, US officials are expected to visit India for bilateral trade agreement negotiations, possibly on August 25.

The deadline for a trade deal between the US and China is set to end on August 12. However, reports indicate that the deadline could be extended by another 90 days, as there has been progress in the ongoing trade talks. The US administration has held three meetings with Chinese officials over the past three months. According to the Financial Times, China wants the US to ease export controls on a critical component for artificial intelligence chips as part of the agreement, ahead of a possible summit between President Donald Trump and President Xi Jinping.

Additionally, attention will be on a potential meeting between US President Donald Trump and Russian President Vladimir Putin, likely to take place on August 15 in Alaska, aimed at ending the war in Ukraine.

US Inflation

Globally, apart from tariff-related developments, the market participants will also focus on the US inflation (on August 12), one of the key factors behind the interest rate decision by the US Federal Reserve, along with speeches by several Fed officials this week. Most economists expect inflation and core inflation to climb higher in July, compared to 2.7 percent and 2.9 percent, respectively, in the previous month, largely backed by tariffs.

The US Federal Reserve chair Jerome Powell also stated that inflation is still elevated, and the growth also saw moderation in the first half of 2025, hence the central bank maintained the status quo on rates in the last meetings. However, Futures markets are signalling a 95 percent chance for a 25 bps cut in the Fed funds rate in the September meeting, especially following substantial downward revisions in non-farm payrolls.

Further, PPI, retail sales, and industrial production for July and weekly jobs data will also be watched.

Global Economic Data

Europe will release its second estimates for GDP growth for the second quarter of 2025, followed by preliminary estimates for Japan's GDP growth, China's retail sales, vehicle sales, and unemployment rate for July, this week.

CPI Inflation

Back home, monthly inflation is the key data to watch out for this week. Most economists expect the retail inflation is drop below the 2 percent mark in July compared to 2.1 percent seen in the previous month, largely backed by subdued food inflation. If that comes true, then that would be the ninth consecutive month of easing. Overall, for the current quarter (Q2FY26), the RBI estimated CPI inflation at 2.1 percent.

Further, the WPI inflation for July, which will be released on August 14, is likely to continue to be negative against dipped to a 20-month low of 0.13 percent in June.

Bank loan & deposit growth for the fortnight ended August 1, foreign exchange reserves for the week ended August 8, and balance of trade data for July will also be announced this week on August 15.

The focus will also be on the June quarter earnings season, which is set to end this week. Hence, the flow of numbers will be large as little more than 2,000 companies will be releasing their quarterly results scorecard, including Nifty 50 names like Oil and Natural Gas Corporation, Hindalco Industries, and Apollo Hospitals Enterprises

Further, key companies like National Securities Depository (NSDL), FSN E-Commerce Ventures (Nykaa), Honasa Consumer, Zydus Lifesciences, Bharat Petroleum Corporation, Brainbees Solutions (Firstcry), Indian Oil Corporation, Ipca Laboratories, Ashoka Buildcon, Awfis Space Solutions, Bajaj Consumer Care, Bata India, Brigade Hotel Ventures, Krsnaa Diagnostics, Travel Food Services, Bharat Dynamics, Alkem Laboratories, Jindal Steel & Power, Abbott India, Hindustan Aeronautics, Nazara Technologies, Oil India, CSB Bank, United Spirits, Hindustan Copper, IRCTC, Jubilant FoodWorks, Samvardhana Motherson International, Muthoot Finance, Vishal Mega Mart, Amara Raja Energy & Mobility, Ashok Leyland, Glenmark Pharmaceuticals, Vodafone Idea, and Zaggle Prepaid Ocean Services will also announce their June quarter numbers.

The activity at the FIIs (Foreign Institutional Investors) and DIIs (Domestic Institutional Investors) desks will also be watched in the this holiday-shortened week. FIIs remained net sellers in the last week, too, given the tariff-led concerns, offloading Rs 10,652 crore worth shares, taking the total current month's outflow to Rs 14,019 crore, though there was Rs 1,933 crore worth buying last Friday. This caused the market to maintain a lower highs-lower lows structure, and according to experts, unless the tariff concerns are resolved, the pressure from FIIs may continue.

On the other side, DIIs continued to be strong supporters in the market; in fact, they also remained net buyers on every dip and compensated the FII outflow by a significant margin. They net bought Rs 33,609 crore worth of shares during the week and Rs 36,796 crore in the current month.

Meanwhile, the Indian rupee hit an all-time low of 87.98 during the low on tariff woes, but the buying interest and softening oil prices reduced the pressure, and the currency ended the week at 87.44 against the US dollar, weakening by 0.26 percent. The Brent crude oil futures corrected by 4.42 percent during the week to $66.59 a barrel, trading below all key moving averages.

The US dollar index traded within the previous week's range as well as sustained below the 100 mark, closing the recent week down by 0.43 percent to 98.26. It is expected to remain volatile this week.

The flow of IPOs reduced a bit this week compared to the previous couple of weeks, as four public issues - 2 each in the mainboard and SME segments - will hit Dalal Street.

In the mainboard segment, BlueStone Jewellery & Lifestyle will open its Rs 1,541-crore IPO on August 11, followed by Regaal Resources' Rs 306-crore offer opening on August 12, while JSW Cement and All Time Plastics will close their public issues on August 11.

In the SME segment, Icodex Publishing Solutions will launch its Rs 42-crore initial share sale on August 11. This follows Mahendra Realtors & Infrastructure's Rs 49.5-crore IPO opening on August 12. Further, Sawaliya Foods Products and Connplex Cinemas will close their maiden public issues on August 11, while the subscription for Star Imaging & Path Lab, Medistep Healthcare, and ANB Metal Cast IPOs will remain open till August 12.

On the listing front, Highway Infrastructure will make its debut on the bourses effective August 12, followed by JSW Cement and All Time Plastics on August 14. In the SME segment, Sawaliya Foods Products and Connplex Cinemas will be available for trading on the NSE Emerge effective August 14.

Technical View

Technically, the market is looking weak as the Nifty 50 maintained a lower highs-lower lows formation with the MACD giving a negative crossover with a histogram weakening last week. The RSI dropped below 50 at 49.50, showing a bearish crossover. Hence, experts see the possibility of Nifty correcting up to 24,200 (200-day EMA) and 24,000 (50-week EMA) is high considering the bearish momentum and advised sell on rally strategy until the index gives a strong close above all key moving averages. In case of rebound, the 24,500 is expected to be an immediate hurdle, followed by 24,700 being the next resistance.

F&O Cues

The weekly options data suggested that the 24,500-24,600 is expected to immediate resistance zone for the Nifty 50, with 24,300 being the support, followed by crucial support at 24,000.

On the Call side, the 25,000 strike holds the maximum open interest, followed by the 24,500 and 24,600 strikes, with the maximum Call writing at the similar strikes. On the Put side, the maximum open interest was observed at the 24,000 strike, followed by the 24,500 and 24,300 strikes, with the maximum writing at the 24,300 strike, and then the 24,000 and 23,700 strikes.

The FII long-short ratio for index futures declined to just 8.28 percent — one of the lowest levels seen recently. This indicates a strong tilt towards short positions, reinforcing the bearish outlook on Indian equities, though the short-covering-led bounce can't be ruled out after such an oversold situation, according to Sudeep Shah of SBI Securities.

Meanwhile, the fear index, India VIX, extended its upward journey for another week, rising 0.48 percent to the 12.03 zone, but remained below short-term moving averages. Overall, the VIX sustained near the lower zone, hence experts feel the possibility of a sharp move can't be ruled out in the coming weeks.

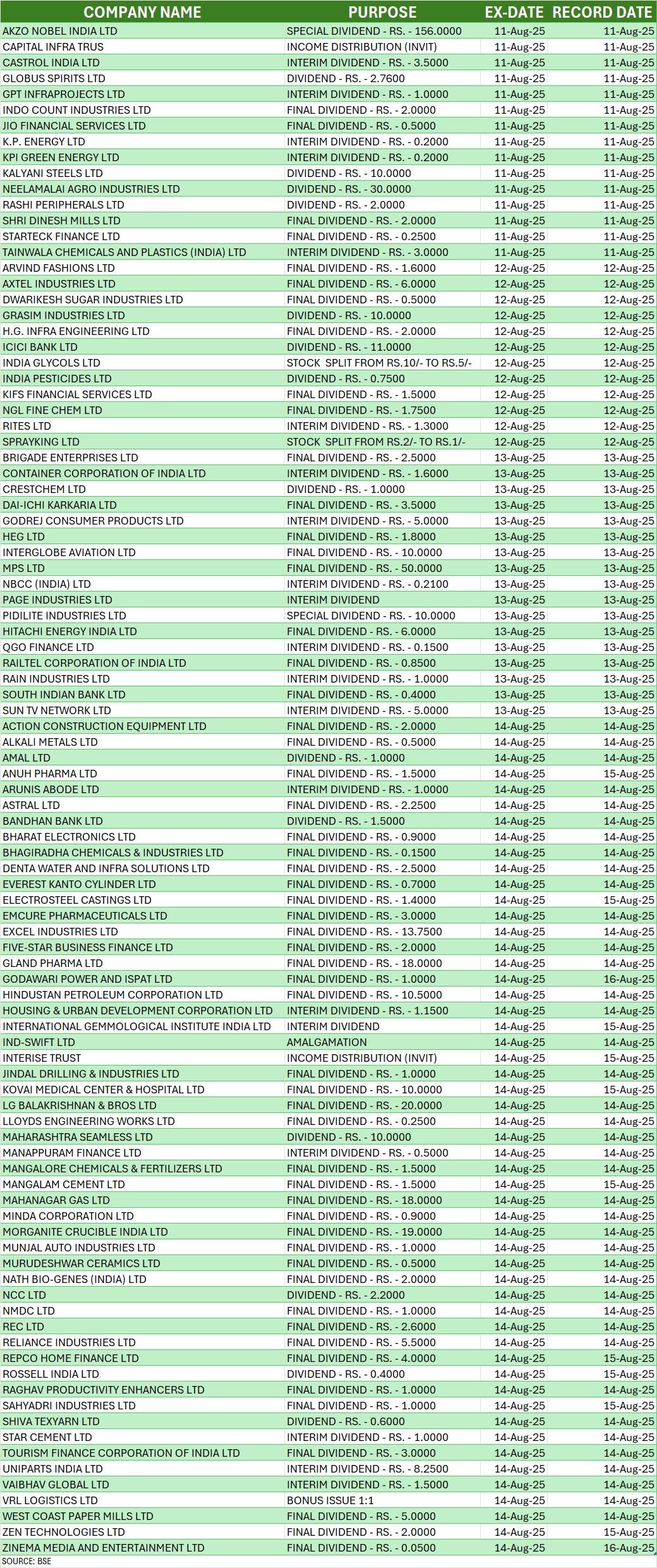

Corporate Action

Here are key corporate actions taking place this week:

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.