Debt investment returns drying up? Check out these options with a 3-5-year horizon

Emerging mutual fund categories like target maturity funds, floating rate funds, as well as traditional investments now offer more options to investors

Mutual fund investors have gone through perception issues recently, with both Axis MF and Invesco MF facing serious allegations of wrongdoings. In the latter's case, the allegations pertain to irregularities in debt schemes. But, advisors say the confidence of investors has not seen a major drop due to these recent events. "While couple of AMCs have attracted negative news flow recently, the perception around mutual funds has not been heavily impacted because of that. There was a large impact after Franklin Templeton crisis, but as FT MF has returned the money to its debt scheme investors, it has improved investors' confidence in fact," points out Amol Joshi, founder of Plan Rupee Investment Services. As far as returns are concerned, experts say there are opportunities within debt mutual funds itself. "Current elevated yields should ensure that debt investors will see better returns compared to what they are getting in last one year in debt funds, provided they remain invested despite current volatility,” says Joydeep Sen, corporate trainer (debt markets). Here, we explore what are the options investors have within debt mutual funds with interest rates rising, as well as the alternatives beyond the mutual funds.

2/10

Floating rate funds (FRFs) are debt mutual fund schemes investing at least 65 percent of their corpus in bonds offering interest at a floating rate. The interest rate offered on these bonds is linked to an external benchmark. These bonds tend to offer a reasonable hedge as their coupons tend to get reset higher periodically. In a rising rate regime, the reference rate, too, rises and this eventually results in the coupon rate of these bonds inching up. Investors should check the credit quality of the portfolios of these schemes before investing. Consider investing in these if you have a minimum three-year view, to take home tax efficient returns.

3/10

Short duration funds (SDFs) are debt mutual fund schemes investing in bonds with a Macaulay Duration of 1 to 3 years. (Macaulay Duration refers to the weighted average of the time to receive cash flows from a bond.) Fund managers invest in a mix of bonds of varying credit quality that mature in short timeframes. In the recent past, most fund managers lowered the average maturity of bonds in their portfolio on the expectation of rising rates. Bonds with short maturity are relatively less sensitive to interest rate movements than those with long maturity. SDFs are the preferred choice in a rising rate environment as the proceeds of the short maturity papers can be redeployed in bonds with higher yields. This should improve the fund’s performance. Investors need to check the credit quality of the portfolio before investing.

4/10

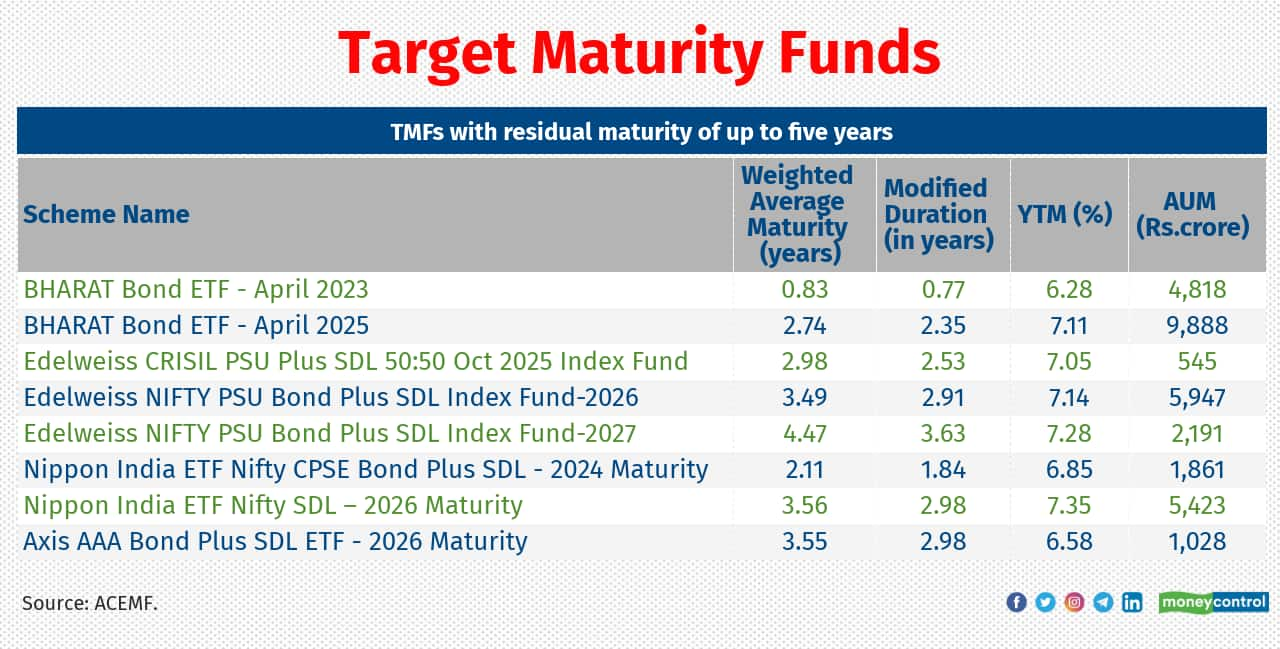

Investors keen on visibility of the returns expected from debt funds may find target maturity funds (TMFs) attractive. TMFs are passively managed debt mutual funds tracking fixed-income indices. TMFs have a predetermined maturity date and hold debt securities that are constituents of the underlying index. These indices typically comprise government securities and high-quality bonds issued by public sector enterprises. Dhawal Dalal, CIO-Fixed Income, Edelweiss AMC says, “ TMFs score on simple investment strategy, high quality portfolio, relative low expense ratio and predictability of returns. Given the recent change in RBI’s monetary policy stance, short-term yields have adjusted upward by 120-130 bp since early May 2022. This has increased the allure of short-maturity bond ETF / Index Fund as well. Now, TMFs of 3+ years maturities are yielding 7% and above. This provides attractive investment opportunity for investors with at least three years of investment horizon.”

Conservative investors have been investing in fixed deposits issued by banks and companies. The FD market now gives a lot more options as there are now small finance banks and new-age banks with their own FD products. The assured returns appeal makes many opt for FDs. After the hike in policy interest rates by the RBI, a few banks and non-banking finance companies have announced an increase in interest rates on offer. Vikram Dalal, Founder and Managing Director, Synergee Capital Services, says, “Investors keen on investing in fixed deposits may consider investing in deposits issued by good quality corporates, maturing in 24 months. As interest rates are going to rise, they will get an opportunity to deploy their funds at higher rates upon maturity.” Do not invest in FDs with very high interest rates as this is also an indication of high credit risk.

6/10

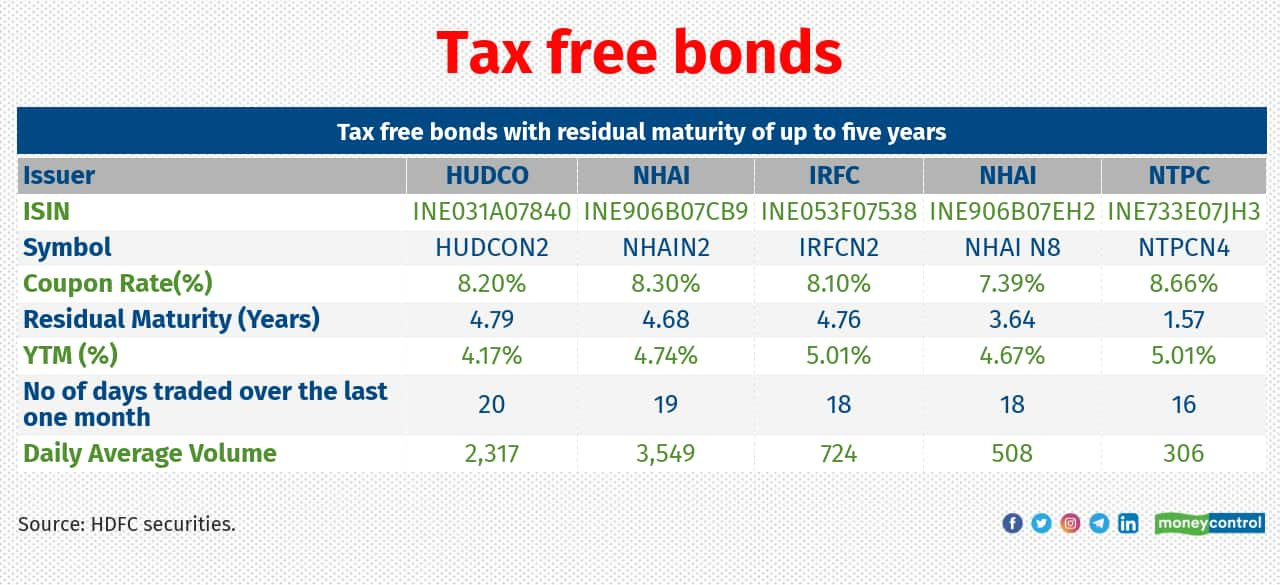

Tax-free bonds were issued by state-run infrastructure finance companies in the period between FY12 and FY16. These bonds were listed on the bourses and are now traded in the cash segment of the BSE and NSE. Investors can buy these bonds — through their demat accounts — from the secondary market. These bonds pay interest annually, which is tax-free. They are largely safe as the issuers are backed by the government of India. “Investors in the highest tax brackets can look at locking in the currently elevated YTM on tax-free bonds,” says Deepak Jasani, Head, Retail research, HDFC securities. With 4.4-4.6 percent YTM, tax-free bonds are still an attractive buy for investors in higher income-tax slabs. For those in the 43 percent tax slab, that results in a pre-tax yield of 7.8-8 percent. Select bonds with higher liquidity and higher YTM in the secondary market that match your time horizon.

7/10

Non-convertible Debentures (NCDs) are fixed income instruments issued by corporates to raise long-term funds through public issues. They are issued for a specific tenure of, say, one to seven years and pay interest periodically or at the end of maturity. Many NCDs that were issued to retail investors (whose face value is mostly Rs 1,000) are listed on the exchanges and traded like equity shares. A few of them are traded with reasonable liquidity and near fair value. Investors with a medium risk profile, looking for options other than bank and corporate FDs, may consider buying these NCDs. However, these NCDs are prone to credit and interest-rate risks. So, one should consider NCDs with a higher rating, better Yield-to-maturity (YTM) and ample liquidity on the exchanges.

8/10

National Savings Certificates (NSC) have a tenure of five years and offer an assured rate of return of 6.8 percent, payable at maturity. Contributions up to Rs 1.5 lakh per year, along with other investments, can fetch you a tax deduction under section 80C of the Income Tax Act. Interest is paid at maturity and taxable in the hands of investors. Since money is locked in for five years, it suits investors who can hold the certificates till maturity. Loans are allowed against NSCs.

Voluntary Provident Fund (VPF): For salaried, conservative investors who are three to five years away from retirement, a voluntary provident fund (VPF) can be an extremely tax efficient and safe investment option. Such individuals can contribute up to 100 percent of their basic salary towards VPF. The money so invested fetches tax free returns and also can be used to claim a deduction under section 80C, up to Rs 1.5 lakh, along with other investments. If the contribution exceeds Rs 2.5 lakh in a financial year, then the interest on the excess contribution becomes taxable, per the slab rate. While opting for VPF, this aspect needs to be kept in mind.

10/10

Government securities (g-secs) are debt instruments issued by the RBI on behalf of the Central Government. State governments also raise money by issuing such instruments, which are called State Development Loans. Treasury bills (T-Bills) are short-term instruments with a maturity of 3, 6 and 12 months, while dated g-secs have a maturity period of 6 months to 40 years. Since the Government of India backs these bonds, they are virtually credit-risk-free investments. However, these bonds are exposed to interest rate risks, which can be avoided if held till maturity. Retail investors can buy these bonds either offline or online. Recently, the RBI launched a Retail Direct platform for retail investors. Under the scheme, investors can buy g-secs at primary issuance, that is, when a bond is first issued by the government. Or, they can participate in the secondary market, which is called the NDS OM (Negotiated Dealing System Order Matching). The other ways to invest directly in g-secs is through a trading and Demat account, which can be opened at any bank or NBFC in India. Retail investors can buy government bonds from stockbrokers and place bids online on the goBID web portal or the NSE goBID mobile application. “Investors in government securities should be prepared to hold on to investments till maturity. Secondary market liquidity can be a challenge. Five-year government securities look better compared to longer tenure securities given their attractive yields compared to 10-year bonds,” says Parul Maheshwari, a Mumbai-based Certified Financial Planner. Investors can also consider gilt mutual fund schemes, which are a more convenient and tax efficient way to invest in g-secs.

. Here, we explore what are the options investors have within debt mutual funds with interest rates rising, as well as the alternatives beyond the mutual funds.")

are debt mutual fund schemes investing at least 65 percent of their corpus in bonds offering interest at a floating rate. The interest rate offered on these bonds is linked to an external benchmark. These bonds tend to offer a reasonable hedge as their coupons tend to get reset higher periodically. In a rising rate regime, the reference rate, too, rises and this eventually results in the coupon rate of these bonds inching up. Investors should check the credit quality of the portfolios of these schemes before investing. Consider investing in these if you have a minimum three-year view, to take home tax efficient returns.")

are debt mutual fund schemes investing in bonds with a Macaulay Duration of 1 to 3 years. (Macaulay Duration refers to the weighted average of the time to receive cash flows from a bond.) Fund managers invest in a mix of bonds of varying credit quality that mature in short timeframes. In the recent past, most fund managers lowered the average maturity of bonds in their portfolio on the expectation of rising rates. Bonds with short maturity are relatively less sensitive to interest rate movements than those with long maturity. SDFs are the preferred choice in a rising rate environment as the proceeds of the short maturity papers can be redeployed in bonds with higher yields. This should improve the fund’s performance. Investors need to check the credit quality of the portfolio before investing.")

are fixed income instruments issued by corporates to raise long-term funds through public issues. They are issued for a specific tenure of, say, one to seven years and pay interest periodically or at the end of maturity. Many NCDs that were issued to retail investors (whose face value is mostly Rs 1,000) are listed on the exchanges and traded like equity shares. A few of them are traded with reasonable liquidity and near fair value. Investors with a medium risk profile, looking for options other than bank and corporate FDs, may consider buying these NCDs. However, these NCDs are prone to credit and interest-rate risks. So, one should consider NCDs with a higher rating, better Yield-to-maturity (YTM) and ample liquidity on the exchanges.")

have a tenure of five years and offer an assured rate of return of 6.8 percent, payable at maturity. Contributions up to Rs 1.5 lakh per year, along with other investments, can fetch you a tax deduction under section 80C of the Income Tax Act. Interest is paid at maturity and taxable in the hands of investors. Since money is locked in for five years, it suits investors who can hold the certificates till maturity. Loans are allowed against NSCs.")

are debt instruments issued by the RBI on behalf of the Central Government. State governments also raise money by issuing such instruments, which are called State Development Loans. Treasury bills (T-Bills) are short-term instruments with a maturity of 3, 6 and 12 months, while dated g-secs have a maturity period of 6 months to 40 years. Since the Government of India backs these bonds, they are virtually credit-risk-free investments. However, these bonds are exposed to interest rate risks, which can be avoided if held till maturity. Retail investors can buy these bonds either offline or online. Recently, the RBI launched a Retail Direct platform for retail investors. Under the scheme, investors can buy g-secs at primary issuance, that is, when a bond is first issued by the government. Or, they can participate in the secondary market, which is called the NDS OM (Negotiated Dealing System Order Matching). The other ways to invest directly in g-secs is through a trading and Demat account, which can be opened at any bank or NBFC in India. Retail investors can buy government bonds from stockbrokers and place bids online on the goBID web portal or the NSE goBID mobile application. “Investors in government securities should be prepared to hold on to investments till maturity. Secondary market liquidity can be a challenge. Five-year government securities look better compared to longer tenure securities given their attractive yields compared to 10-year bonds,” says Parul Maheshwari, a Mumbai-based Certified Financial Planner. Investors can also consider gilt mutual fund schemes, which are a more convenient and tax efficient way to invest in g-secs.")