Krishna KarwaMoneycontrol Research

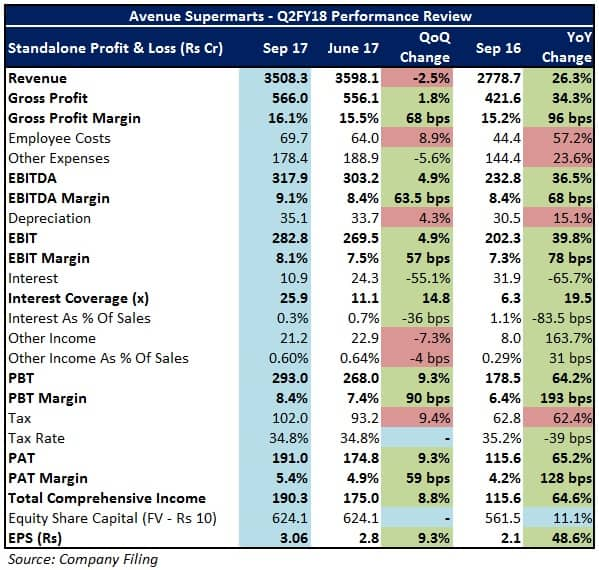

Avenue Supermarts (ASL), India’s most valued retailer by market capitalisation, reported strong numbers for the September quarter. After an impressive rally since its listing in March this year, the stock, which was already a tad too expensive to begin with, has left little on the table for investors. Nonetheless, here’s a look at how things panned out in the quarter gone by:-

As GST-induced disruptions led to merchandise pricing pressures, ASL maintained top-line growth through higher volumes and addition of five stores in the first half of the fiscal.

EBITDA margin growth was helped by economies of scale (in terms of product procurement), good inventory management practices, and cost-efficient operations (through the adoption of a cluster-based distribution model).

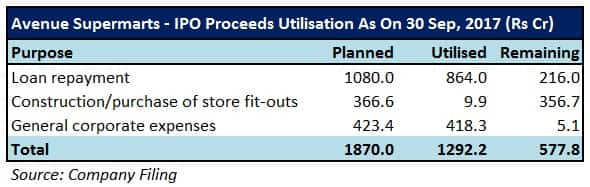

Interest costs fell as IPO proceeds were used to prepay some of the debt. This, in turn, helped protect margins despite a spike in capex.

Omnichannels, store additions, and GST to drive sales growth

ASL aims to expand its omnichannel network (through neighbourhood pick-up points and chargeable home delivery services), especially in and around Mumbai, from 41 at present to over 400 by the end of FY20.

The company is expected to add 20-25 new stores every year, primarily in its core markets in western India. The possibility of exploring new markets in Punjab, Rajasthan, Uttar Pradesh, and Tamil Nadu is under consideration as well. Savings in lease rentals, coupled with a high fixed asset turnover, augur well for ASL’s profit margins in the long run as the company owns almost all the stores operated by it.

Furthermore, GST is likely to benefit the organised retail industry across multiple models such as supermarkets, convenience stores, hypermarkets, and online retail.

Private labels to aid margins

For every 5 percent increase in D-Mart Premia's (ASL's private label brand in grocery items) contribution to the total turnover, on an average, its operating margins could rise by roughly 20 bps.

Dry grocery to remain the key focus area

ASL has a limited degree of exposure to fresh food, where localised sourcing is important and margins are low, as compared to items requiring centralised sourcing (such as dry grocery and home/personal care). This helps the company to negotiate payment terms with consumer product companies and expand operating leverage through effective working capital management practices.

Competitive pricing policy to cushion e-commerce threat

Though the boom in e-commerce may affect ASL’s store footfalls, we expect the impact of the same to be fairly minimal given the competitive pricing policy followed by the company at its brick and mortar outlets (by virtue of the ‘every day low pricing’ scheme, among others) from time to time.

Valuation

While we take note of ASL’s stellar show, expansion plans and steady fundamental parameters, at 73x FY19 projected earnings, the stock’s valuations, undoubtedly, seem stretched at the moment.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!