Budget 2021's indication on high government borrowing has already pushed up yields on debt securities up. Interest rates and bond prices move in opposite direction. Experts say that it’s only a matter of time before interest rates increase.

Liquid funds are typically marketed as a means to park sums for the short term to earn a bit more than savings bank accounts. However, currently, leaving money in saving bank accounts is more beneficial. If you invest regularly in liquid funds, or have money lying in there, then here is what you should do.

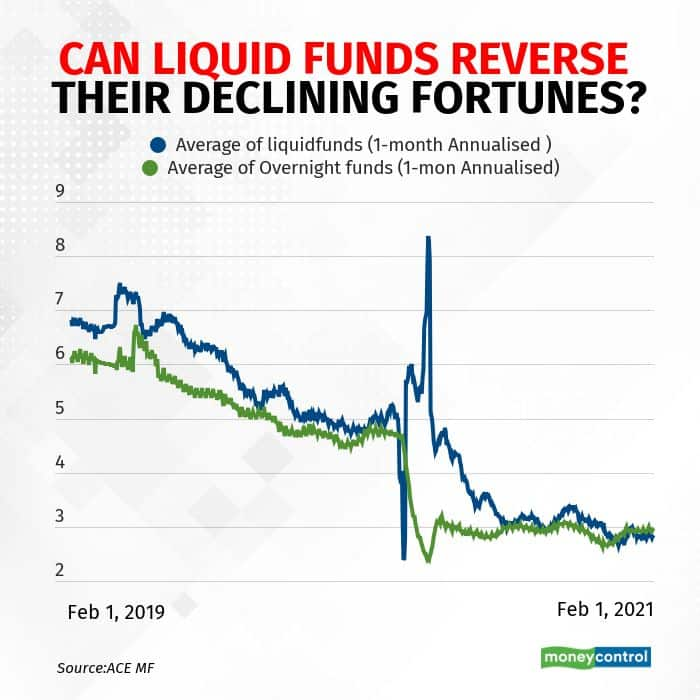

What has changed?

Liquid funds used to give more than the returns offered by saving bank accounts. For example, according to Value Research, liquid funds delivered 7.02, 6.55 and 4.16 percent in 2018, 2019 and 2020, respectively. Since liquid funds invest in short-term instruments such as treasury bills and commercial papers, the rate of return depends more on the liquidity situation. To fight the economic slowdown caused by the COVID-19 pandemic, the Reserve Bank of India (RBI), like other central bankers, cut interest rates. Increased liquidity ensured that the short term rates fell. This has led to lower returns from liquid funds, which are less than even savings accounts interest rates.

But the situation may change. Joydeep Sen, Corporate Trainer (Debt Market) expects the interest rates to move up gradually. But interest rates aren’t likely to go up in a hurry.

“Given the high fiscal deficit numbers, there is no scope to cut rates for the RBI. As inflation has softened in December compared to last year and the inflation projection for 2021 is lower than that of 2020, there is no pressure to increase the rates immediately, when the RBI is supporting large borrowing programme of the government,” he adds.

What are the alternatives?

Typically, ultra short duration and even short duration funds offer alternatives. Some investors have also begun parking their money in long-term bond and gilt funds. But this is a bad move.

In search of high yield, when you go for schemes with high duration, you end up taking interest rate risk. If interest rates increase quickly, then you are bound to lose. For example, corporate bond and banking & PSU bond funds lost on an average 29 basis points returns on February 1, 2021, as yields spiked in response to the budget announcements.

“When your investment time frame in a scheme is significantly less than the portfolio maturity of the scheme, you may lose money if the losses caused by upward yield movement exceed the coupon accrual for the period you are holding your investment,” says Sen.

If you are not keen to take these risks, then you can consider savings bank accounts offering high interest rates. For example, IDFC First Bank offers 6 percent rate of interest on the savings bank account for balances up to Rs 1 crore.

Despite low returns, liquid funds make sense, sometimes

There are a few situations where overnight and liquid funds still make sense. If you have a lump-sum amount to invest in an equity fund, then opting for a systematic transfer plan (STP), makes sense via such funds.

If you have large amounts of cash – because you sold some asset or got the maturity proceed of some old investment – then these funds can be used for temporarily parking the sum.

Should you look beyond liquid funds?

“Interest rates on debt instruments maturing in less than one year have fallen the most. As the cycle turns, these money market instruments may see the rate moving up in the near term,” says Dwijendra Srivastava, Chief Investment Officer-Debt, Sundaram Mutual Fund. He recommends liquid and ultra short duration funds as options to park your money for the short term – say a month or two.

Match your investment time frame with the duration of the scheme. Investing in longer duration than your timeframe for higher return can be risky. “If you have a horizon of a few weeks or 2-3 months, then you can consider ultra-short term funds. Choose low duration funds for 3-6 months horizon," says Amol Joshi, founder of Mumbai based Plan Rupee Investment Managers.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.