Life Insurance Corporation of India’s (LIC) latest product – Jeevan Utsav – a non-market-linked, non-participating (that is, guaranteed returns) whole life policy, has attracted the attention of prospective policyholders and financial advisors. This investment-cum-insurance traditional policy is meant to provide not only life cover, but also regular income over the long term, after the premiums are paid.

This limited premium payment policy offers cover even beyond 100 years, and promises 10 percent of the basic sum assured as annual income post the premium-paying period through two options – regular income and flexi-income benefits. Since the payouts are made periodically under this whole life plan, there is no lump-sum maturity benefit that will be paid. The details are here.

Also read: Will the rising market tide lift LIC?

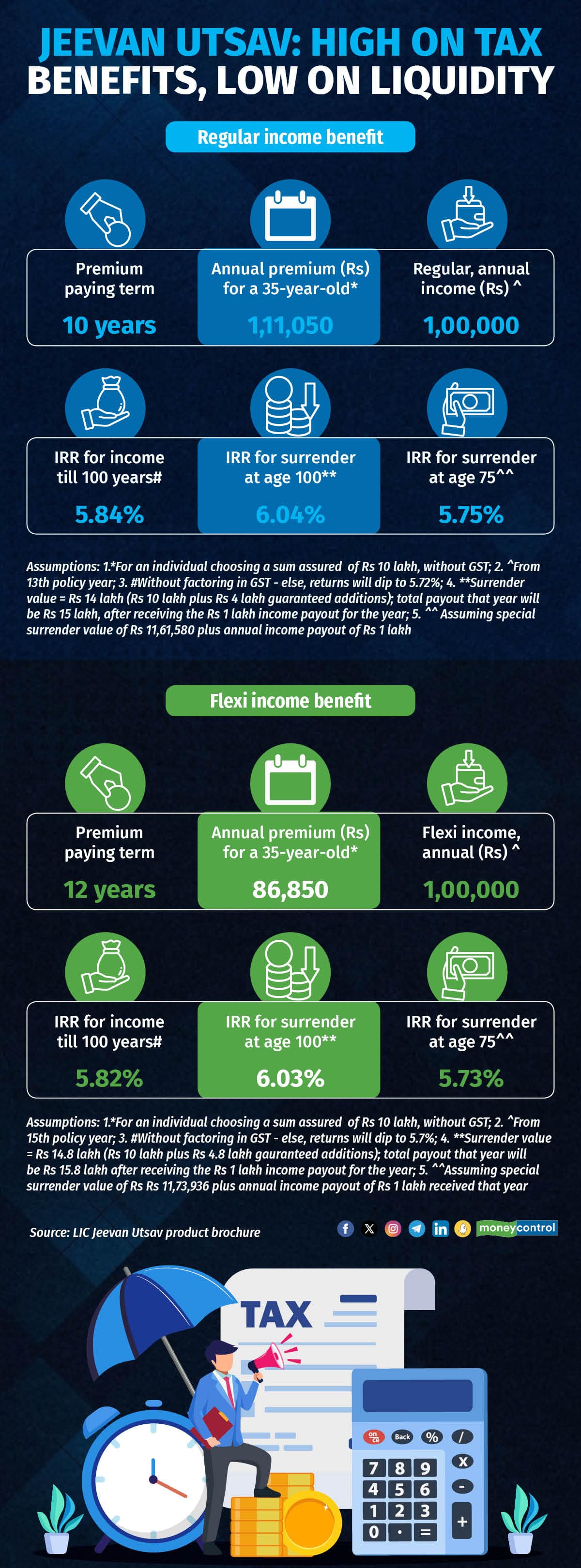

Guaranteed, long-term incomeFor a 35-year-old choosing a premium-paying term of 10 years and sum assured of Rs 10 lakh, the annual premium will be Rs 1,11,050, as per the product’s benefit illustration. Under the regular income option, this means an annual payout of Rs 1 lakh from the 13th policy year until year 65 (policyholder’s age then = 100 years). As per Moneycontrol’s calculations, the internal rate of return (IRR) works out to 5.84 percent without factoring in GST (5.72 percent with GST). However, as per LIC, the IRR will be much higher at surrender.

“Assuming he surrenders the policy after taking the income benefit, the total payout in the 100th year after adding Rs 14 lakh (basic sum assured plus guaranteed additions) would be Rs 15 lakh. Accordingly, if, at age 100, the Rs 1 lakh is replaced with Rs 15 lakh, the IRR would be superior,” LIC said in emailed responses to Moneycontrol’s questions around IRR. The IRR, in this case, will go up to 6.04 percent.

Surrendering earlier – which seems more reasonable – however, will mean lower IRR .

“Also, the product has higher IRR in different scenarios. For example, for sum assured of Rs 50 lakh for a person aged 10 years, with a premium-paying term of nine years, the IRR would be 6.04 percent at age 100 without adding the SA (sum assured) of Rs 50 lakh and guaranteed additions of Rs 18 lakh available to the policyholder on surrendering the policy. Also, when Rs 50 lakh plus Rs 18 lakh is added to the income benefit of Rs 5 lakh available under the regular payout at age 100, the IRR would be more than 6.04 percent,” LIC said.

Financial planners, however, recommend keeping insurance and investment needs separate. "There is greater flexibility and scope for earning higher returns by investing across equity and debt asset classes. In the case of policies like Jeevan Utsav, you have to fulfil the regular commitment of paying the premiums so that your policy remains in force. Exit is not easy due to high surrender charges,” said Pankaj Mathpal, founder of Optima Money Managers.

What worksSince the maturity proceeds of fresh traditional life insurance policies with total annual premiums of up to Rs 5 lakh are tax-free, the ‘income’ payouts under this policy will not attract any tax. Fixed deposit interest attracts tax and also comes with reinvestment risk.

“Those who are not financially savvy and prefer an assured, fixed stream of income can consider this product. While even fixed deposits are suited for such people, this instrument comes with the reinvestment risk (there is no certainty that rates will remain higher when your fixed deposit matures and you need to reinvest the amount). However, LIC's plan will continue to offer the promised 'income',” said Nirav Karkera, head of research at Fisdom.

There are some categories of individuals who might find this product appealing. “Since this is a whole life policy, it might be suitable for some individuals – for example, those who are looking for assured, regular income over the long term, post their retirement. In the case of individuals whose collective premiums for policies bought after April 1, 2023, are less than Rs 5 lakh, 5.7-5.72 percent is a reasonable return,” said Mathpal.

According to him, it is better than the post-tax returns of some fixed deposits (assuming you are in the highest tax bracket) and even annuity from insurance or the National Pension System, which is taxable at slab rates. The State Bank of India (SBI) currently offers an interest rate (annualised yield) of 6.5 percent (7.5 percent for senior citizens) on fixed deposits with tenures of up to 10 years. The post-tax return, thus, works out to 4.47 percent for those in the 30 percent tax bracket.

What doesn’t workThe bane of all investment-cum-insurance policies is the requirement of long-term premium-paying commitment and the steep exit barriers in the form of high surrender charges.

“For savvy investors, there are several better alternatives such as debt funds, National Pension System (NPS) and even fixed deposits,” said Karkera. He said these products offer better flexibility in terms of investing as well as exit and also there is scope for higher returns.

“On the other hand, Jeevan Utsav necessitates regular premium payments and complex surrender rules to exit the product if you realise it does not suit your needs,” he added.

If the objective is to create a long-term retirement corpus, the National Pension System (NPS), which offers 60 percent lump-sum and pension for life from the 40 percent annuitised corpus, is a far better instrument, he feels. “NPS comes closest to Jeevan Utsav. Annuities, too, offer income for life. Though annuities are taxed at slab rates, you need to take into account the fact that the entire maturity corpus is not taxable – up to 60 percent can be withdrawn as tax-free lump-sum. The combined returns of these two components are likely to be more remunerative, post-tax,” said Karkera.

The probability of earning higher returns in NPS is greater because it offers the choice of asset allocation – you can deploy funds in equity, corporate debt and government securities as also alternative assets. “The equity component in your portfolio can yield much higher returns over the long term (which is the horizon of Jeevan Utsav, too), volatility in the interim notwithstanding,” said Karkera.

Also read: National Pension System: Not just a great retirement tool, it offers tax benefits too

Moneycontrol’s takeIt is best to not mix insurance and investment needs. A simple term insurance policy to secure your loved ones’ future and investment in mutual funds across asset classes, keeping your goals, risk appetite and investment horizon in mind, is the ideal approach, particularly for savvy investors. If you can stay put for the long term and stomach market volatility, equity is the best asset class to create a retirement portfolio.

Even debt funds and the NPS are likely to yield higher returns. As of November 24, 2023, the NPS’ scheme G (government securities) funds reported annualised 10-year returns of 9-9.84 percent. LIC, as an NPS annuity service provider, offers an annuity rate of 6.53 percent if you choose the ‘lifetime annuity with return of purchase price’ option.

A long commitment to paying the premium is another worry. According to data for 2021-22 from the Insurance Regulatory and Development Authority of India (IRDA), on an average, close to 56 percent of life insurance policyholders (across companies) surrendered their policy after the fifth policy year.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.