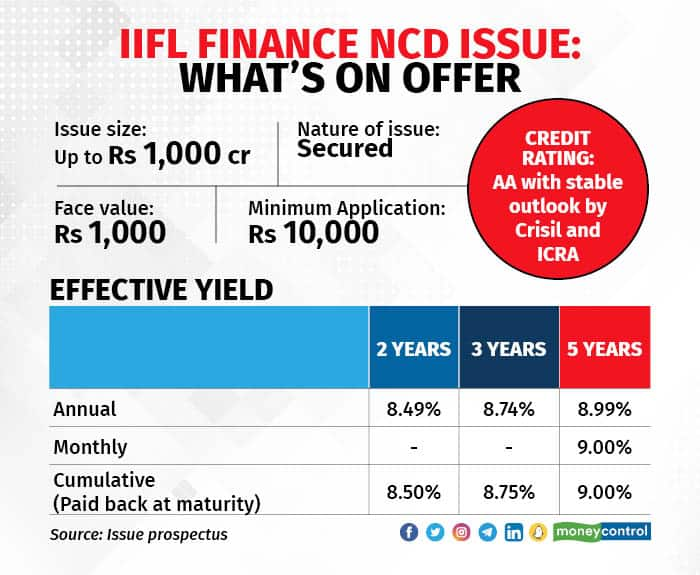

Non-banking financial company (NBFC) IIFL Finance Ltd on 6 December launched its public issue of secured non-convertible debentures (NCDs) to raise up to Rs 1,000 crore.

IIFL Finance’s offerings include home loans, gold loans, business loans, including loans against property, and medium and small enterprise financing, microfinance, construction and real estate finance, and capital market finance, catering to both retail and corporate clients.

The Fairfax-backed NBFC will issue secured NCDs worth Rs 100 crore, with a green-shoe option to retain oversubscription of up to Rs 900 crore, aggregating to a total of Rs 1,000 crore. The allotment will be made on first-come, first-served basis.

The NCDs offer the highest effective yield of 9 percent per annum for a tenor of 60 months. The NCDs are available in tenors of 24, 36 and 60 months. The frequency of interest payment is monthly, annually, and on maturity (60 months), while for other tenors it is annually and on maturity.

The company is raising funds for the purpose of onward lending, financing, refinancing its existing debts and general corporate purposes.

Past issues

The IIFL Finance group had raised Rs 3,000 crore via public issue of bonds during financial years 2011-14, and the same was repaid, along with interest, on time to all the investors.

Further, the group has raised about Rs 4,000 crore via public issue of bonds since FY19, of which Rs 1,325 crore has been repaid.

Also read | Edelweiss Financial Services NCD offers attractive rates

The company had raised funds via public issue in the past various years with different tenures and coupons, the last round being in October 2021. The company had offered returns of up to 8.75 percent per annum for tenure of up to 60 months, and had mobilised Rs 843 crore from the issue.

What’s hot

The NCD issue has been rated AA with stable outlook by both Crisil Ltd and ICRA Ltd. This rating indicates that the instruments are considered to have a high degree of safety for timely servicing of financial obligations and carry lower credit risk.

IIFL Finance claims that it has consistently maintained low level of non-performing assets (NPAs) and continues to focus on good quality of assets with gross NPA of 2.42 percent and net NPA of 1.22 percent. Additionally, as on September 30, 2022, 85.03 percent of the company’s consolidated loan book was secured with adequate collaterals, helping mitigate the risks further.

Also read | InCred Financial looking to raise up to Rs 350 crore via NCDs

The NCDs are also secured against 100 percent of the loan assets and other receivables of the company. The company's core loan products include gold loans.

What’s not

However, it is worth remembering that IIFL Finance’s NCD issue isn’t rated AAA, which indicates the highest degree of safety.

In its ratings rationale, Crisil noted, "While Crisil Ratings-adjusted return on managed assets improved to 1.4 percent for fiscal 2022 from 1.3 percent in fiscal 2021 (0.9 percent in 2020), it remains modest.”

Meanwhile, ICRA noted that the ratings are constrained by the impact of the COVID-19 pandemic on the group's profitability and asset quality.

“The asset quality has moderated on account of pandemic-related issues and slippages in the real estate book. With high slippages and write-offs, credit costs remained high in FY2022 and FY2021, thereby impacting the profitability,” it said.

What should investors do?

Experts say that beyond the ratings one needs to look at whether the company possesses the wherewithal to service the payouts.

“You may have a scenario where the company is stable, but the particular paper (security), keeping in mind whatever the collections are going towards, may not be as secure. So, not just the issuer needs to be looked at, but also for what purpose that money is being garnered, that needs to be looked at,” said Deepali Sen, Founder Partner, Srujan Financial Services LLP.

Kirtan Shah, Founder and CEO of Credence Wealth Advisors LLP, believes that repo rates in India will go up by another 25 basis points (bps) in the next policy, which will top out the rate-hike cycle in India, and probably two quarters later, rates may even start falling, but yields will start falling before that.

“If you want to park some money in private issues such as IIFL, try to avoid long durations like five, six or 10 years. Always look at 24 months, because the credit risk in 24 months is lower. Don’t lock yourself for long duration because such companies are always in need of capital, and so they will always come with offerings,” Shah said.

That is also perhaps why the company has offered a monthly interest option ― considered the most attractive by those seeking a regular and fixed income ― for just the five-year option, the longest in this offering.

Further, Amol Joshi, Founder of Plan Rupee Investment Services, suggests that any kind of capital, especially in debt allocation, is best deployed in multiple instruments.

IIFL Finance’s NCD issue opens on January 6, 2023, and will close on January 18. It comes with an option of early closure.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.