then you have to pay tax on your worldwide income in India.")

Is your company sending you overseas on a work assignment? If yes, it’s likely your employer will provide you a certain living allowance in addition to your salary in India. This could be to compensate you for your overseas living and travel expenses or simply put, for the higher cost of living.

Will this living allowance be counted as part of your salary and be taxed in India?

A recent order passed by the Delhi Bench of the Income Tax Appellate Tribunal ruled that an NRI working in Austria and receiving a salary / living allowance from his Indian employer for services rendered outside India is not liable to pay any tax in India on such income.

So, would the outcome have been different if the taxpayer had been an Indian resident?

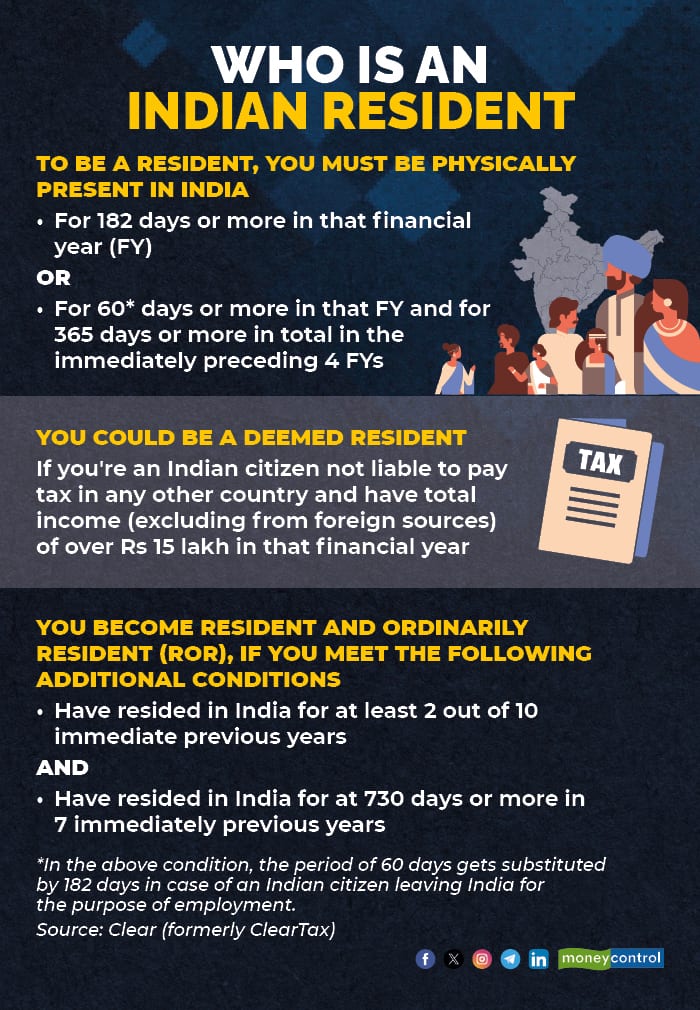

Resident or non-resident taxpayerChetan Chandak, Director of TaxBirbal, a tax consultancy firm, says that when it comes to income tax, the question of residency comes first (is the taxpayer a resident or a non-resident Indian). Next comes where the income is being generated (in India or overseas), and then comes taxation.

If you are a resident Indian, or more precisely, an ROR (Resident and Ordinarily Resident) then you have to pay tax on your worldwide income in India. If you have paid tax on any foreign income earned in any other country, you can claim tax credit for it in India.

According to Chandak, if you are an RNOR (Resident but Not Ordinarily Resident) or an NRI, then any foreign income earned outside India will not come under the Indian tax net and so will be exempt in India, irrespective of whether it is paid in an Indian bank account or a foreign one.

“Salary, including related allowances, is deemed to be earned at the place where the actual physical services are rendered. So, if these are earned by a non-resident Indian in a foreign country, they will be taxable in that country,” says Chandak. (see table for more details on who qualifies as a resident and non-resident Indian)

In the context of salary (income from employment), Neeraj Agarwala, Partner at Nangia Andersen India, a tax firm, highlights that for NRIs and RNORs, only income received by them for services rendered in India while being physically present in India will be taxed in India.

Also read: Want to stick with the old income-tax regime? Don’t forget to fill this form firstLiving allowances: Taxable or not?Coming specifically to allowances, Agarwala says that any allowance received as a fixed amount by an employee from a company in India is treated as part of his salary and taxed as such.

“But if a company structures the allowance smartly, whereby instead of a fixed amount, it provides reimbursement of up to a certain amount based on actuals (supported by bills) for expenses incurred in the course of one’s official work, this amount will not be included under taxable income,” says Agarwala.

Also read: Tax on ESOPs - How NRIs can navigate the rule bookReferring to Section 10 (14) of the Income Tax Act, which covers tax exemption of certain allowances, Chandak makes a slightly different point. In the context of a resident taxpayer, he says that any compensatory allowance given for expenses incurred for stay, travel etc. as part of one’s work is tax exempt under this section to the extent it is spent. “Going by a strict reading of this section, anything that is not spent becomes taxable in the hands of a resident taxpayer,” says Chandak.

For example, if an Indian resident working overseas spends USD 100 out of an allowance of USD 250, then USD 150 will be added to his taxable income. It would be the same for someone working in India.

However, Agarwala says that unless the allowance is structured appropriately (given as a reimbursement and not as a fixed sum), even if a taxpayer claims exemption only to the extent of actual expenses supported by bills, it could result in tax litigation.

Talking in the context of allowances that employees receive for work-related expenses, Alok Agrawal, Partner, Tax, Deloitte India says that if your company is giving you such an allowance, then it must be backed either by actual bills or a declaration from the employee (for small amounts) confirming that the allowance given was used for the intended purpose. “In the absence of both, if no tax is paid on this amount, the employee or employer may face a tax enquiry,” says Agrawal.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.