Highlights:-

- The kitchen sink quarter raises more questions on asset quality and governance

- Market apprehends significant undisclosed exposure to troubled accounts

- Promoter interference is also a cause for concern

- Earnings to remain weak in the near term

- Raising capital at this valuation may not be rewarding

- Do not sell at this price but wait for capital raising

Ever since the declaration of the quarterly result, the Yes Bank stock has been falling continuously and the decline is now close to 50 percent. Are all the concerns priced in or is there worse to come?

It was common knowledge since RBI had denied a fresh term to founder CEO Rana Kapoor that all was not well with the bank. The reported pristine asset quality (1.3 percent gross NPA at the end of FY18) amidst the challenge in the banking space was always suspect though the RBI clean chit after the audit of FY18 numbers provided some ray of hope.

The kitchen sink quarter (Q4 FY19) under the new CEO Ravneet Gill (whose name was approved by the regulator) raised more questions on the quality of the book and governance standards at the bank.

More skeletons in the closet?

Instead of drawing comfort from the clean-up exercise, investors started worrying about the hidden exposure to troubled sectors and groups. Going by the grapevine, the exposure to troubled assets could be as high as Rs 26,000 crore, much higher than the sub-investment grade book that is a little over Rs 17,000 crore declared by the bank so far. It is pertinent to note that the bank saw over Rs 11,000 crore addition in this category in a single quarter. According to the management, they have created ad-hoc contingency provision of Rs 2,100 crore on low-rated standard assets of close to Rs 10,000 crore in Q4.

The net worth of the bank is a little over Rs 26,904 crore and going by the grapevine’s number if there is little recovery, the entire net worth could get eroded. Gill, however, in his media interactions reiterated the credit cost guidance at 125 basis points in FY20 (209 basis points for FY19). Only the earnings of the coming quarters will show the size of the hole and how fast the clean-up is taking place. With the economy in the slow lane, one cannot rule out more skeletons coming out of the closet.

The backdoor entry of the promoter?

The shadow control of the promoter has also remained an overhang. Reports suggest the promoter is reportedly making a claim for a board seat while RBI has appointed R Gandhi to bolster the CEO’s authority in the clean-up exercise of the bank.

Gill has made it unequivocally clear that he wants to be on the right side of the regulator by adopting superior risk management and the highest standards of corporate governance.

In terms of the near-term micro outcomes, a focus on retail both on assets as well as liabilities with more cross-selling, decentralisation of functions, making branches profitable are high on the agenda. Strengthening the bank’s digital leadership and sweating the database more effectively is also on the cards.

The earnings impact of the cleanup

While the growth may be cleaner, it will certainly be more moderate. The impact of the less risky book and reversal of interest income due to prompt NPA recognition will be felt on NII (net interest income or the difference between interest income and interest expenses). Fee income will be modest thanks to prudent accounting practices that the bank has started adopting from Q4 FY19.

While it is good to know that the bank is on a reform path, the new CEO has to walk the talk to convince investors. He has to have the support of his team and a free hand without any interference of the promoter shareholders.

As of now, there is no clarity on this front and it remains to be seen if Gill succeeds in getting capital on the basis of his intended clean-up story alone. With the share price falling to Rs 120 from Rs 404, raising capital at this valuation itself may not be a worthwhile proposition.

So earnings will remain weak and contradictory news flow will keep serious investors on the sidelines until Yes Bank succeeds in raising capital.

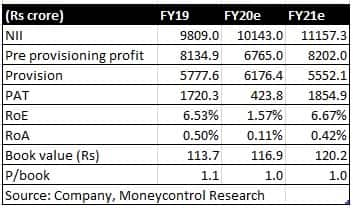

We attempted to look at the stress case valuation of Yes Bank, assuming elevated credit cost of 240 basis points and 220 basis points in FY20 and FY21, respectively, along with lower interest margin and non-interest earnings.

The only redeeming point amid the dark clouds is that the promoters still have a reasonably high stake in the bank at 19.8 percent and further erosion in market cap due to promoter’s interference may not be in their best interest. Finally, with a balance sheet size of over Rs 380,000 crore, the bank assumes importance and may not be allowed to go down by the regulator in the best interest of the system. So while the downside may not be significant from here on (hence existing shareholders should not be selling at this price), the upside is not immediate either. The journey to recovery may be long drawn with intermittent hiccups. Unless institutional investors repose faith in Yes Bank’s reform story by giving it capital at a decent valuation, catching this falling knife should be avoided.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!